First, even if we agree to go with a middle ground, then USDe should have been allowed to depeg for DeFi to .995 rather than be hard coded to 1. This is safer because there could be instances where the deepest pools of liquidity depeg more than that.

Second, I even if I agree with the framing that the goal is to separate out the case of temporary secondary price dislocation versus permanent impairment of collateral, this goal is not easily achievable in true tail scenarios. From the perspective of Binance, they can 1) use an oracle that looks at deeper liquidity pools that are not their own to determine if USDe should be liquidated as collat or 2) they can treat all of DeFi and other exchanges as invisible and exogenous to their own closed system. If they chose 2), then they are not able to determine what is a temporary dislocation versus a true impairment of collateral because it looks the same to them. So then how things played out is exactly the result. If they choose 1), then there are other tradeoffs. 1a) They are effectively loaning their own balance sheet out temporarily based on the trust they have toward the custodian, the oracle provider, and other exchanges. In extreme cases where let’s say USDe becomes hugely successful and much bigger, Binance would be betting the solvency of their exchange on trusted third parties. If they are wrong in their judgement, users hold the bag. At this point, you might as well just formalize a cross-industry clearinghouse thus reinventing the wheel from tradfi. That would at least be better than the current structure. 1b) In the time it takes MMs to cut over liquidity from USDe DeFi pools to CeFi, the liquidity on Curve/Uni/Fluid could deteriorate. In other words, local books guarantee higher solvency than expecting liquidity to be cut over from external books which is not as instant. Easy example is if two exchanges have local book dislocations and then wait to liquidate based on a DeFi oracle. MMs go to grab the same liquidity to service two exchanges. You can’t grab the same liquidity even though it initially looks like you can.

Third, at some point the tri-party custodian agreements will be tested. The custodian will have to decide whether an incoming margin call is real or fictitious. If they ignore a real margin call, Ethena is safe but the exchange and its users get rekt. If they fulfill a fictitious margin call, Ethena gets rekt and true impairment of collateral will happen.

Fourth, if Ethena has a special deal with exchanges for ADL protection, does that mean any firm with the same transparency, similar risk profile, and a tri-party custody agreement can get this privilege? If not, this would break exchange neutrality. If so, it puts undue burden on the exchanges to have case-by-case customized integrations to check up on any user who wants this. The issue here is that exchanges are taking on brokerage function. The exchange should be neutral while the brokerage doesn’t have to be. The brokerage risks their own balance sheet in isolation but the exchange, by risking their balance sheet, affects solvency for all users. This would also be a reinventing of the wheel from tradfi but long term would help avoid conflicts of interest.

For the short term, there’s many different things that can be done. Exchanges could use a DeFi oracle that looks at the deepest pools and integrate those pools into their liquidation engine. Alternatively, they could not do that and instead create a cap on USDe that can be used as collateral based on their local USDeUSDT book. Exchanges can also offer ADL protection based on a fee though the total ADL-protected capital must be significantly less than the exchange’s balance sheet. They can also provide a toggleable option to auto-close underwater positions when other profitable positions are ADL’d. They can also run stress tests on how much USDe can be redeemed into USDT without closing out Ethena’s perp positions and then what it would look like if those were closed under more severe situations. This could be run as a slower separate process periodically off the matching and standard risk check hot path.

In the long term, there should be separation of exchange and broker function and also the creation of a clearinghouse. Exchanges already share risk with each other, not just through Ethena, but in many other ways too. Might as well formalize the risk sharing agreement and create a robust clearing system. Lastly, each exchange should have a transparent and thorough rule book. Users should know exactly what deals are possible and how to get them. In this particular case, we might call it project-capture of an exchange but you also want to avoid MM-capture of exchanges.

Apr 3, 2025 • 18 tweets • 3 min read

The US is basically saying that it is not bluffing and entirely willing to face higher prices in order to export civil unrest and economic turmoil to the rest of the world if they don’t play ball.

The US is tired of other countries and their protectionist policies which create large trade imbalances for the US but also happens to distort these foreign labor markets (through artificially weak currencies) and intentionally suppresses their quality of life.

Mar 26, 2025 • 12 tweets • 2 min read

Every decision sets precedent for the future. Binance and Okx listing perps in Hyperliquid’s face does help their short-term incumbency status but it also sends the message to other cex and dex competitors of what to expect if they take on bad liquidations.

This has multiple negative effects. First, it means that challenger exchanges will be more robust in their risk management thus creating stronger competition for incumbents, like an immune response.

Mar 1, 2025 • 7 tweets • 1 min read

Since everyone is trying to rewrite history, I as Tacitus, keeper of the crypto a[n]nals, will tell you the an alternative history of USDC. Once upon a time Circle looked upon USDT and thought, “damn, those guys over there are making a shit ton of money”.

They figured that the market’s big enough for two players. Plus even though their OTC desk was dominant along with Cumberland, how are you supposed to get a good rev multiple for valuation based on a trading business.

Jan 7, 2025 • 7 tweets • 1 min read

Definitely some similarities. I would add that after the fall of the USSR, in the power struggle between the libertarian faction and the nationalist faction of the coalition, the nationalists won.

In my view, this is because the techno-capitalists are, by nature, more individualistic than the ethno-nationalists and thus have varying interests which pull them in many different directions.

Nov 26, 2024 • 12 tweets • 2 min read

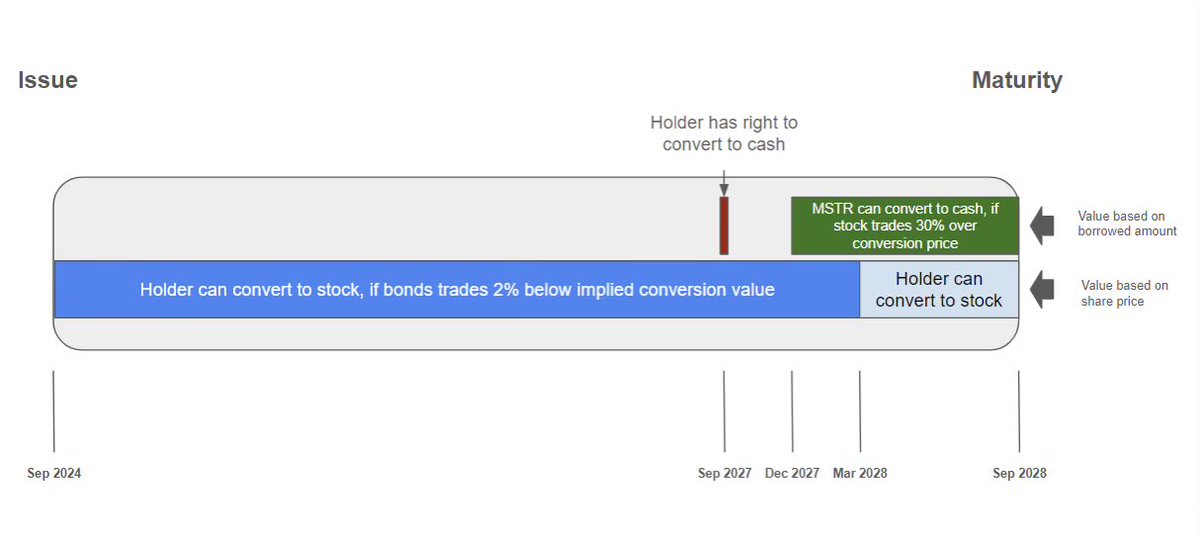

MSTR is like a BTC ETF but with greater flexibility in being able to do treasury/trading operations. So as long as they continue to make good decisions, it makes sense that MSTR trades at a premium to the underlying.

The only question is how much of a premium is fair. The market is pricing this by pulling from the future, into the present, expected profits and profit growth.

Sep 3, 2024 • 5 tweets • 1 min read

After an exhaustive and costly investigation of nearly two years, and without admitting or denying the findings detailed in the SEC’s order, we agreed to settle with the SEC and pay a $225,000 penalty which will go directly to our investors.

We’re glad to put this matter behind us. We used Fireblocks, a non-qualified custodian, as a best-in-class solution to secure our crypto assets.

Sep 3, 2024 • 14 tweets • 2 min read

It seems that since the default Twitter algo changed, narrative formation in crypto has been weak, h/t @AlokVasudev. My guess is that half of CT is still trapped on the For You feed which drives TikTok-like engagement.

This feed often shows more polarizing political topics given the election coming up. The other half are on the Following feed whose algo may or may not have also changed from the old one.

Jul 17, 2024 • 16 tweets • 3 min read

Tragedy of the Crypto Commons

Mostly agree with @AriDavidPaul and @ZeMariaMacedo assessments. Their suggestions on how to improve things will likely help. Still I don’t think there is an easy fix to the entire problem.

The core problem is that there are plenty of one-cycle oriented founders and VCs. This is because VCs have to make profits for their LPs and their LP capital largely comes from outside of the industry.

Jun 9, 2024 • 16 tweets • 3 min read

Apologia of the Trader

What purpose does the short term trader serve? He builds nothing for consumption nor does he advance the sciences. To most tribesmen, the trader seems to be at best a sellsword, at worst an annoying buzzard.

In fact, the trader serves an important role in short term capital allocation. Not belonging to any tribe, the trader represents the marginal capital which longs underpriced assets and shorts overpriced assets.

Jun 6, 2024 • 6 tweets • 1 min read

Degeneracy and the propensity to gamble cannot be solved by the social layer. In fact, it is so innate that it cannot even be solved with force.

There’s only one thing we can do. We can ask ourselves why degeneracy and gambling tendencies are on the rise. It’s the same reason for GME season 1 and season 2.

Jun 4, 2024 • 5 tweets • 1 min read

Interesting debate about whether staking issuance or the selling of it is a cost. Staking is a near 100% transfer from non-stakers to stakers and the government (tax on yield).

On the other hand, in a PoW system, mining is a significantly less than 100% transfer from non-mining holders to miners and the government (tax on mining profit).

May 31, 2024 • 4 tweets • 1 min read

A Future Eulogy for a Fallen Hero

When the mob finally sacrifices @blknoiz06, let it be said that he didn’t do anything particularly wrong. Was he a priest? No. But was he any worse than those who were crucified before him? Also no.

When the time comes, let us remember it as a Girardian comedy rather than a tragedy. Let us remember the joy he brought us wif his calls.

Apr 8, 2024 • 20 tweets • 3 min read

Have been thinking about the ETH issuance curve debate recently. I think both sides make some good points. However, there are many more considerations that should be in scope but have not been brought up.

If the goal is to target a lower equilibrium staking ratio/level than the eventual 100% staking level due to the current issuance curve, you should consider secondary and tertiary effects from Ethena.

Feb 20, 2024 • 12 tweets • 2 min read

I gaze into my crystal ball and I see two possible futures for the industry. In one future, LRTs are accepted as collateral in CeFi and DeFi and looping is eventually allowed.

As more people synthetically sell their ETH through this mechanism, the basis yield is compressed to low single digits or zero. This drives down borrow costs for ETH.

Dec 22, 2022 • 5 tweets • 1 min read

This difficulty is exactly why I think bridges should be built with tolerance for safety failures of the underlying chains. The risks should be made transparent to users and users can decide if they want to use the bridge.

Contrast this with the earlier approach of bridge projects sweeping these types of risks under the rug and trying to guarantee safety, something which is not generically possible for all underlying protocol pairs.

Sep 30, 2022 • 6 tweets • 1 min read

Pax Romana

I look around and what do I see. No more double digit billion market cap shorts to be had. I see the last grains of bitterness give way to sorrow and apathy.

Sep 14, 2022 • 5 tweets • 1 min read

"A man sees in the world what he carries in his heart." ~ Goethe, 'Faust'

"That which issues from the heart alone, will bend the hearts of others to your own." ~ Goethe, 'Faust'

Aug 13, 2022 • 16 tweets • 3 min read

Even though I still think the fork is mildly accretive, long merge plays have overextended in my opinion. Hence, with a heavy heart, I’ve decided to express a net short on ETH by shorting in small size ETH Sep futs and long BTC in that size multiplied by ETH beta to BTC.

As everyone I talk to is long into the merge, it causes significant asymmetries between further upside value vs downside risks due to exogenous shocks and fragility.

Aug 11, 2022 • 4 tweets • 1 min read

I agree that between Aristotelianism and Platonism, the mob is surely more Aristotelian. But when we divide things between Platonism and modern schools like Nietzsche and Foucault, the mob is surely more Platonic.

It’s essentially a gradient between the concrete/measured vs the abstract/analytical. The mob is lacking in abstraction ability but slowly gets better at it over centuries.

Aug 11, 2022 • 6 tweets • 1 min read

Crito is my favorite of Plato’s works though I disagree Socrates in this passage. It’s my favorite because it explains why Socrates did not escape and flee his fate even though he had the opportunity to do so. He was Zeratul.

A lone man against a mob. A man persecuted for his ideas. Contrast this to the current day where Platonism is the rule. You could say that the entirety of western civilization was built on Plato, indirectly Socrates.