Connect the Financial dots.

Analysis organized & presented in proprietary big-data & augmented web.

Patent US 11,327,775 B2

ex hedgie

👇 get a free account

2/17

2/17

2/6

2/6

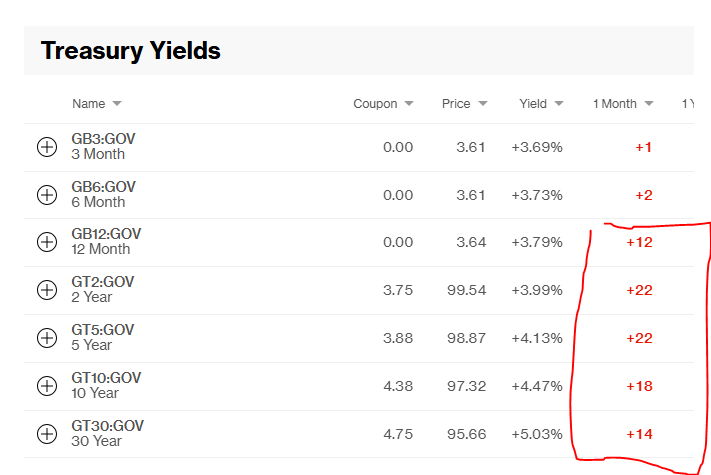

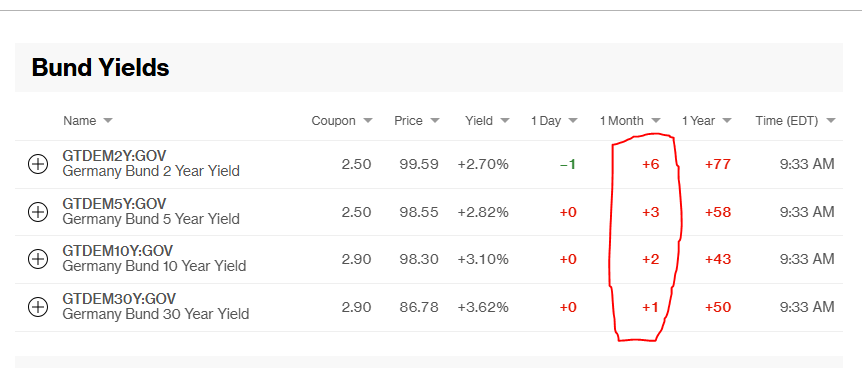

2/14 And NO, it's not happening primarily in Europe.

2/14 And NO, it's not happening primarily in Europe.

2/9 In the historical episode described, the UK government—burdened by excessive debt, largely as a result of fighting the Napoleonic Wars—chose to reduce the coupon on its obligations.

2/9 In the historical episode described, the UK government—burdened by excessive debt, largely as a result of fighting the Napoleonic Wars—chose to reduce the coupon on its obligations.

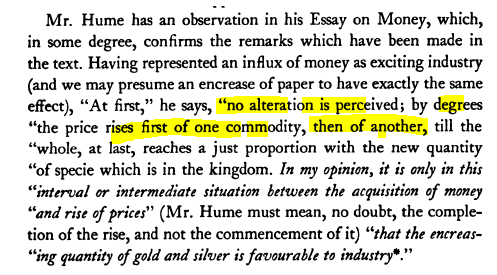

2/25 But that is the second phase in fact the first phase is “exciting industry” aka TINA .

2/25 But that is the second phase in fact the first phase is “exciting industry” aka TINA .

2/ Coupled with some dissavings

2/ Coupled with some dissavings

2/10

2/10

2/14

2/14

Why would any central bank be crazy enough to stimulate a bubble?

Why would any central bank be crazy enough to stimulate a bubble?

2/18

2/18