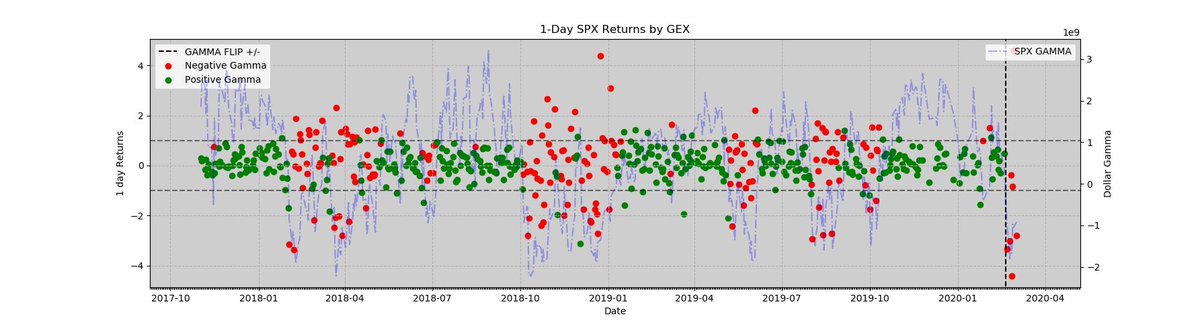

& Let the radio silence end. As you may have seen, we’ve spent the past couple of months researching, modeling, and building a new ‘ecosystem’ to track market gamma for individual stocks and SPX.

A quick explanation (and history):

Early models solved this problem by making assumptions about open interest.

The first / most popular OI assumption is just assuming all calls are sold and all puts are bought. Surprisingly, some people still use this assumption today to measure gamma.

This is frightening.

Mar 4, 2020 • 8 tweets • 5 min read

@_sbr1@SqueezeMetrics 1/ You *still* seem to have this entire thing perplexingly misunderstood.

1. ‘computation itself assumes…dealers hedge (GEX) by exclusively trading the underlying.’

No it doesn’t. The paper asserts that SPX options dealers hedge their *deltas* – by trading in the underlying.

@_sbr1@SqueezeMetrics 2/ The rationale is that rather than cannibalizing the liquidity they exist to provide by purchasing the requisite options to maintain a gamma-neutral book, dealers tend to hedge their deltas directly by adjusting their position in the underlying.