3rd gen Oklahoman. Board member $FGNX / $GFP.TO. Co-founder @childrensnoco w/ my amazing wife. All views are mine. Always do your own work.

3 subscribers

Nov 8, 2023 • 5 tweets • 1 min read

Hard to overstate how big of a deal this is for $BKTI

accesswire.com/800977/bk-tech…

The word 'transformational' almost doesn't cut it. The transaction allows BK to focus on what they do best, engineering, and transfers the capital / labor intensive functions to an expert who is now a significant shareholder

Dec 21, 2022 • 4 tweets • 1 min read

This transaction transforms GFP

- Exclusively in Ontario, most valuable fiber basket

- Lowers overall cost to produce

- Focuses our capex on our low cost mills

- We have significantly more capital than we need go forward

businesswire.com/news/home/2022…

Would note the price we sold these mills for is essentially the same as we paid for all six mills in 2021, and these are our highest cost mills (by a lot)

Private market values are well above current public market prices

May 29, 2022 • 63 tweets • 11 min read

The Story of Zales

This is my account of the story at Zale Corporation from the fall of 2007 to the spring of 2011. This is my memory of the events that at least in part define the investor I am today. This is a complete discussion, at least from a financial perspective.

This was a very difficult time in my life, which I will get into. This was also a very difficult time in others lives that were involved. That I will not get into.

This is my personal journal. I’m sharing it for two reasons.

Mar 16, 2022 • 9 tweets • 2 min read

I don't have a lot of them, but here is my favorite Michael Price story

Summer of 2003 I'm an intern at MFP. I've been there maybe a month and Michael asks me to go to an IPO lunch for him

He calls me into his office and says "Mike, I want you to go to this IPO lunch at the 21 club. Its an IPO of this new REIT thats going to own commercial office space leased to banks"

Feb 8, 2022 • 8 tweets • 2 min read

If you were all knowing and could precisely predict a businesses cash flows from now until the end of time you wouldn't put any weight on the quality of that business

So why do people care? Because cash flows are not predictable and quality offers downside protection***

BUT, there are plenty of things that can erode that downside protection

@ElliotTurn has the thread of the day going (could end up begin thread of the year) on selling discipline

I'm no genius and if we're all being honest with ourselves I'm probably an average analyst / investor (ok maybe below average)

But I think about this topic a lot

And for me, there are two reasons to sell (neither are easy btw)

1) when your thesis changes 2) when the stock overshoots your (conservative / rational) estimate of fair value

The *key* imo is that these two things have to be mapped out BEFORE you buy

Jan 28, 2022 • 5 tweets • 1 min read

OK - totally out of $QRTEA as of this morning at roughly $6

What changed? I have two strong signals that my thesis is wrong

- The business deteriorated through December (materially), that isn't supposed to happen

- My strong guess is capital returns will be put on hold

Stock is certainly cheap here (as it was yesterday and the day before and the day before), but that wasn't the thesis

The thesis was that the business is stable and that we're going to get all of our capital back within 3 years (+/-)

Dec 1, 2021 • 17 tweets • 3 min read

How I got a job in research at an investment bank as an outsider from a less than non-target school with zero experience (1/n)

First, I identified someone in the industry who was in a position to give me a chance and I made it my job to get him to like me (Michael Price gave me a 3 month internship in the summer of 2003)

This was my foot in the door (2/n)

Aug 29, 2021 • 5 tweets • 1 min read

Debt levels, valuations, the health of the US consumer, growth vs value factors, and the direction of the market

I’ve spent a lot of time thinking about this and I’m finally ready to offer up a roadmap of where we’re going from here

A thread (1/n)

It’s possible there will be a rotation and the market will react favorably before pulling back. It’s impossible of course to rule out that current winners don’t sustain momentum pushing new highs until the eventual correction brings us lower (2/n)

Apr 16, 2021 • 4 tweets • 1 min read

There is an absolute legend on twitter

Someone I follow (incidentally doesn't follow me but who's counting) who never really posts

A few years back this person made a somewhat large bet on a micro cap

Shares were trading weak on some news this person figured wasn't that bad

He bought over a million shares for a little under a dollar (he is a hitter)

Today those shares are trading close to $60

It is my understand he hasn't sold a share

Apr 15, 2021 • 7 tweets • 2 min read

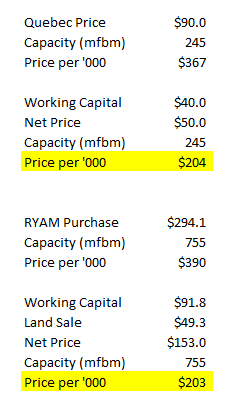

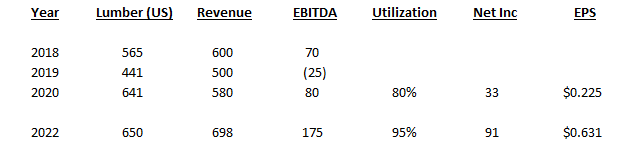

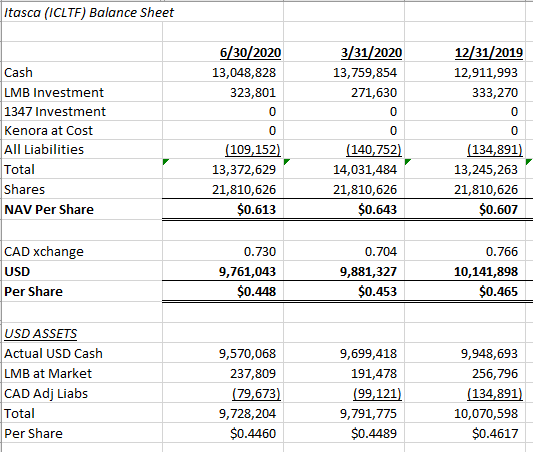

I've been asked more than a few times about the "normal" price of lumber and how to think about valuation. That really is the key question. Here's how I'm thinking about it

Thread could get long so I've linked to a PDF in case thats easier. I'll probably add to this thread over time.

Disclosure: I own a bunch

1/n

TL:DR

ICL was a pile of cash run by @kcerminara . They bought a lumber mill in Canada out of bankruptcy. Price paid looks really attractive. Two secular changes making CA lumber mills look like decent assets. Two very legit outsiders wrote a $5m check to get involved...

2/n