Economics prof @UWEBristol. @PKEconSoc chair. @FMM_macro fellow. @PEF_online council. Blogging intermittently at https://t.co/gjD32qdMbg

It’s a stellar line up for the first panel.

It’s a stellar line up for the first panel.

I shall plug these gaps, thus making my house more waterproof and better insulated!

I shall plug these gaps, thus making my house more waterproof and better insulated!

Note the use of the 'then' when discussing banks. A clear and incorrect statement of temporal ordering.

Note the use of the 'then' when discussing banks. A clear and incorrect statement of temporal ordering.

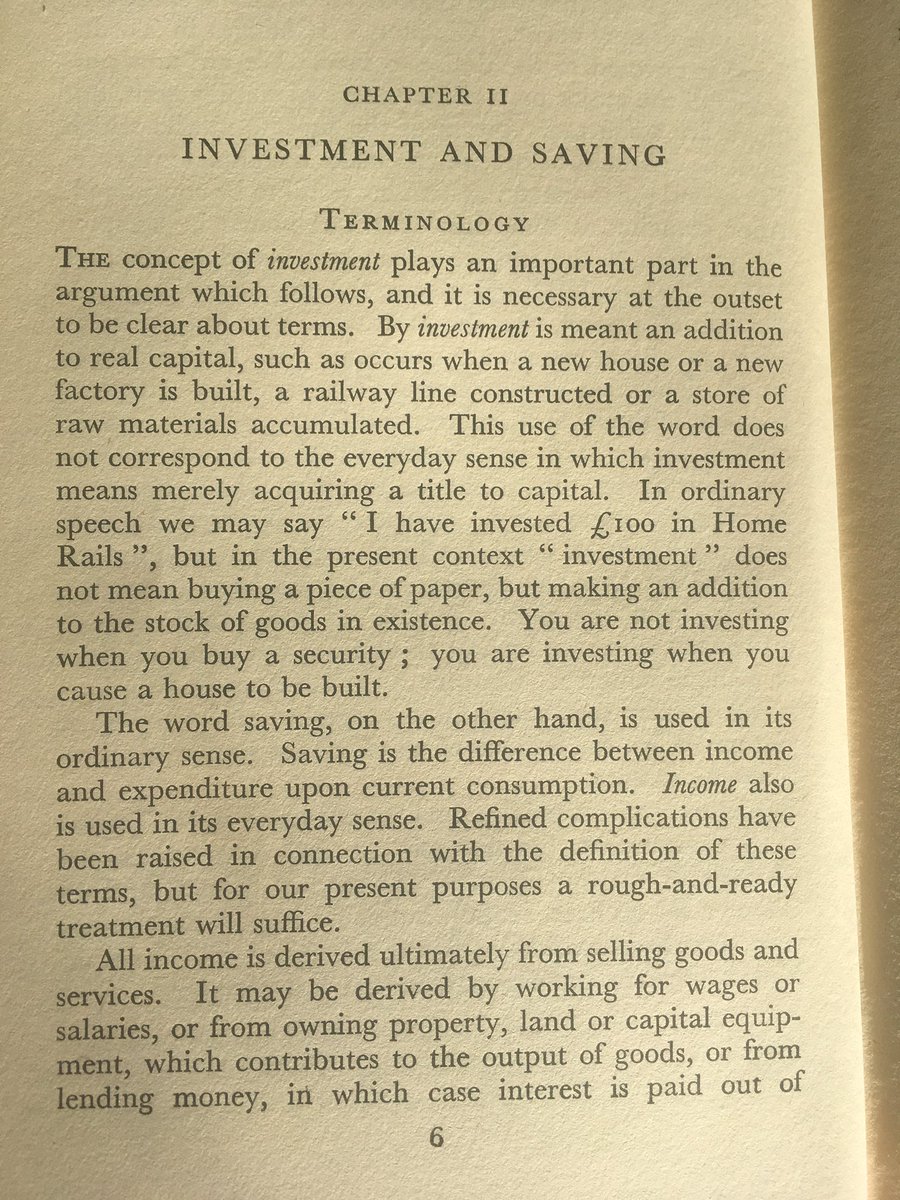

By investment is meant an addition to real capital ... This use of the word does not correspond to the everyday sense in which investment means merely acquiring a title to capital. ... Saving is the difference between income and expenditure on consumption. 2/

By investment is meant an addition to real capital ... This use of the word does not correspond to the everyday sense in which investment means merely acquiring a title to capital. ... Saving is the difference between income and expenditure on consumption. 2/

Gilt rates at 4.1%. Righto. I guess it's possible that gilt rate could also be a different number over a 50 year time horizon. But no confidence bands, yes, fine fine.

Gilt rates at 4.1%. Righto. I guess it's possible that gilt rate could also be a different number over a 50 year time horizon. But no confidence bands, yes, fine fine.