Associate Professor @NovaSBE, Ph.D. in Economics at University of Illinois (@EconAtIllinois)

The setting: Portugal’s municipalities set their own corporate surtax.

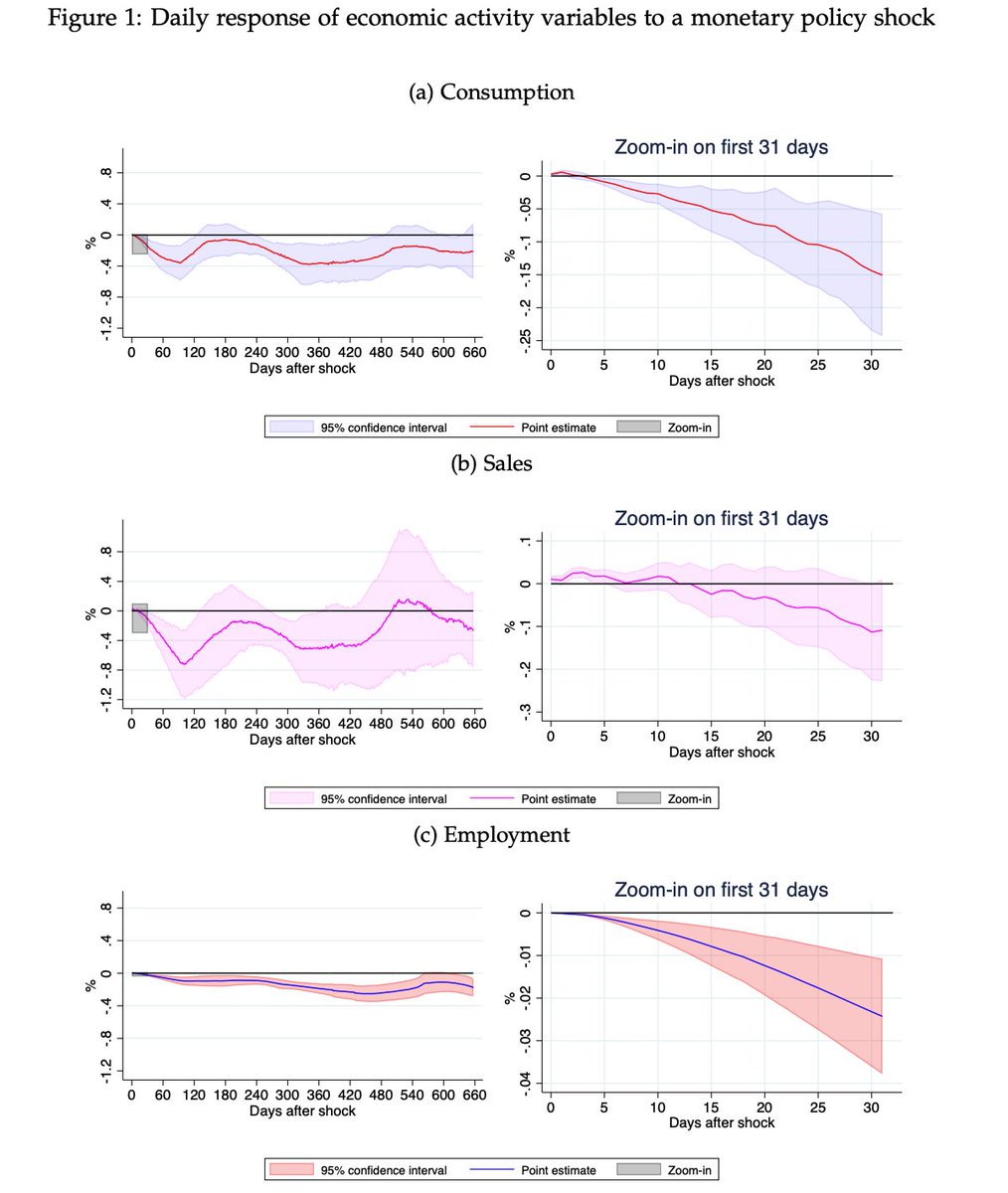

The setting: Portugal’s municipalities set their own corporate surtax. We use novel consumption (bank transactions), sales (VAT) and employment (social security) at very high-frequency (daily) in Spain, together with high-frequency monetary policy shock identification for the Euro Area, to revisit Friedman's dictum. 2/N

We use novel consumption (bank transactions), sales (VAT) and employment (social security) at very high-frequency (daily) in Spain, together with high-frequency monetary policy shock identification for the Euro Area, to revisit Friedman's dictum. 2/N