Koyfin is a financial data and analytics platform for researching global stocks, ETFs, Mutual Funds, macro trends, and portfolios. Sign up for free.

1) The weight of the Magnificent Seven* more than 30% of the S&P 500, about level with prior peaks in mid-2024 and early-2025.

1) The weight of the Magnificent Seven* more than 30% of the S&P 500, about level with prior peaks in mid-2024 and early-2025.

1) $UBER Uber

1) $UBER Uber

2/ $PTON Peloton

2/ $PTON Peloton

2) $MSFT Microsoft

2) $MSFT Microsoft

1) Drawdowns are the norm, not the exception.

1) Drawdowns are the norm, not the exception.

1) Today's largest companies are built different.

1) Today's largest companies are built different.

1. The 80/20 rule:

1. The 80/20 rule:

1) These charts are sometimes called 'Fair Value' chart lines, where you plot a range of constant valuation multiples to visualise where the company trades in relation to those bands.

1) These charts are sometimes called 'Fair Value' chart lines, where you plot a range of constant valuation multiples to visualise where the company trades in relation to those bands.

2) $MSFT Microsoft

2) $MSFT Microsoft

2) $XYZ Block

2) $XYZ Block

1/ Most investors misprice extreme outcomes - markets often overpay for "lottery" stocks (low probability, high payoff) and underprice extreme downside risks.

1/ Most investors misprice extreme outcomes - markets often overpay for "lottery" stocks (low probability, high payoff) and underprice extreme downside risks.

2) The 10 largest companies in the S&P 500 accounted for nearly 40% of total market capitalization and nearly 60% of total index returns in 2024

2) The 10 largest companies in the S&P 500 accounted for nearly 40% of total market capitalization and nearly 60% of total index returns in 2024

2) $PEP PepsiCo

2) $PEP PepsiCo

2) $MSFT Microsoft

2) $MSFT Microsoft

Here is how you would set up the screen in Koyfin, which yields 122 results across the US, Canadian, and European markets (you can include other continents or countries).

Here is how you would set up the screen in Koyfin, which yields 122 results across the US, Canadian, and European markets (you can include other continents or countries).

2) $CRM Salesforce

2) $CRM Salesforce

1/ What is a compounder?

1/ What is a compounder? 1. Things that have never happened before occur with some regularity

1. Things that have never happened before occur with some regularity

2/ Value traps, and how to avoid them

2/ Value traps, and how to avoid them

2) $WMT Walmart

2) $WMT Walmart

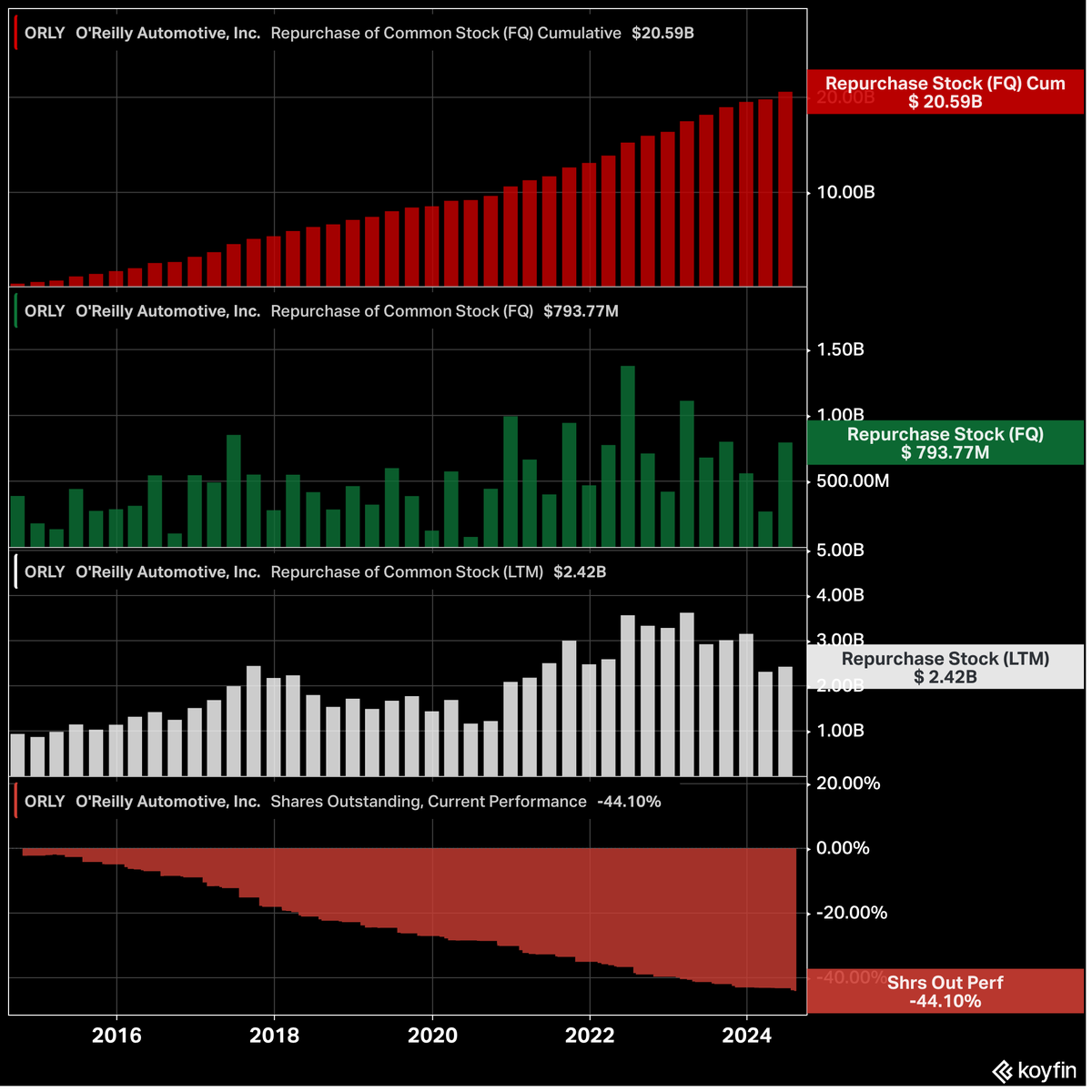

2) $ORLY O'Reilly Automotive

2) $ORLY O'Reilly Automotive