Renegade economist/investment strategist for large global Asset Mgr, Research Associate @ Levy Institute, GISP, Itinerant permaculturist

Aug 12, 2020 • 8 tweets • 2 min read

1/n Savings gluts narratives are used by many mainstream/New "Keynesian"/economists, zentral bankers, & policy makers. The marginal propensity to spend money on goods and services out of money income flows does matter, but savings glut narratives all lead back to loanable funds.

2/n Loanable funds theory makes no sense in a world where bank loans and bank investments create money, and where central banks create money out of thin air. Portfolio preferences do matter, no stock of savings, or flow of savings, or even stock of money.

Jun 18, 2020 • 14 tweets • 3 min read

1/n Even Jeremy Grantham doesn't get it. This is the Hot Ice Age-1 step beyond @albertedwards99 phenomenal Ice Age call. In the Hot Ice Age, asset prices hyperinflate, while consumer prices deflate...as much of a mindf*ck 4 investors as stagflation in '70s zerohedge.com/markets/invest…2/n The problem is stunted Milton Friedman. Milty stunted Irving Fishers MV=PT. T is for all transactions that use money as a means of final settlement. Milty turned T into Q, the quantity of final goods and services available for sale for money in any acct period.

May 27, 2020 • 19 tweets • 9 min read

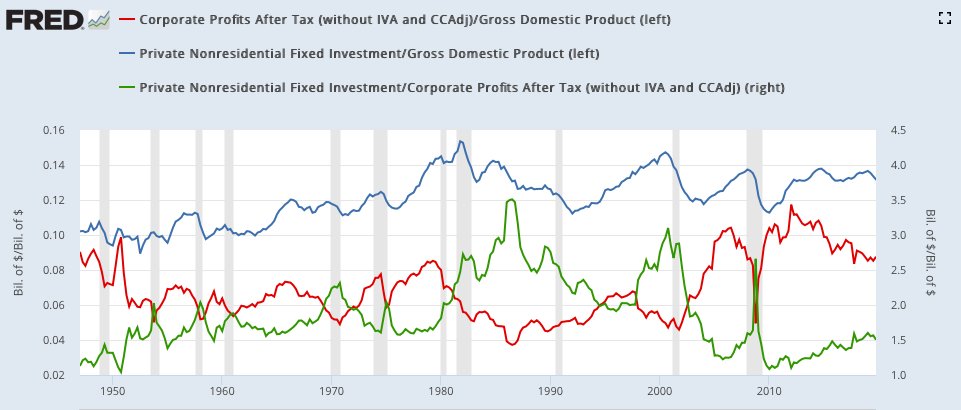

1/N We should applaud @LHSummers recognition of the work neoMarxian economists Bowles, Gintis, Weisskopf, and Schor did on worker power...4 decades ago. Am willing to bet they are not cited in this paper anywhere. See ideas.repec.org/a/tpr/restat/v… & amazon.com/Beyond-Wastela… for proof.

It's spring, 1941. Planning for the postwar period already underway. Alvin Hansen is running the Economics and Financial Group at CFR w/Jacob Viner. A statement on the aims of WWII is provided to the State Dept. with the following proposals front and center: 2/

May 3, 2019 • 15 tweets • 3 min read

1. Name the bomb throwing Harvard economist who wrote the following MMT consistent insights re WWII, after serving as an economic advisor to the State Department, the US Treasury, and the Federal Reserve Board (thread ahead): "The liquid assets of nonbank investors increased..."

2. "in 1940-1945 inclusive by 215 billion dollars...Of this vast expansion in liquid savings, totaling 215 billion dollars, 205 billion was due to the Federal budgetary deficit...Thus the increase in liquid savings sprang almost entirely from the Federal deficit-in other words...

Apr 5, 2019 • 11 tweets • 3 min read

So now the truth is really out. More than a few Wall Street practitioners like myself have helped many institutional investors - like Allianz Global Investors, who I have advised for over two decades - make successful investment decisions with many of the analytical tools of MMT.

That means The Big Lie that Headline Keynesians like @paulkrugman & @LHSummers and @delong and Ken Rogoff have been feeding u of late the MMT= Nonsense is simply sheer nonsense itself. We r practitioners. We get fired if we give bad advice. The oroof of concept is in our careers.

Mar 14, 2019 • 18 tweets • 5 min read

If you understand how many people have such a large stake in IPOs finding favorable equity market conditions in 2019...you can begin to understand Fed Chair Jay's Miraculous Policy Pirouette in Dec. 2018. And to be fair, S&P 500 op profit margin squeeze hit hard in Q4 '18.#FEDUp

The Fed says it just pursues the goals that Congress specifies. The Fed interprets those rules are: minimize unemployment subject to the constraint of maintaining stable inflation. The Fed defines stable inflation @ or near 2%, usually on core (ex food and energy) PCE deflator.

Mar 14, 2019 • 13 tweets • 4 min read

The models of New Keynesians r irrelevant 2 the economy we actually inhabit. They suffer from a Lump of Savings assumpt. Banks do not need 2 gather deposits 2 make loans - loans create deposits. BoE has vids but you will not find this in Krugman textbook.

#MMTNotMMM What we really have here is MMT calling out MMM: Mickey Mouse Macro. Some investment professionals & central bankers know this, because we have to deal with actual money and finance institutions, make decisions with real repercussions for clients. MMM is malpractice.

Mar 11, 2019 • 10 tweets • 2 min read

New Keynesians, or Old Fisherians? MMT & All That.

Dear Dr's Summers, Krugman, Rogoff, et al. Please give a quick glance at "How Much Does Finance Matter", from the book, Keynes on the Wireless.

With all due respect, your version of Keynes does not match his own words. Read them.

Here, let me make this a little bit easier. This is the opening passage from a BBC Radio address by JMKeynes, March 23, 1942. JMK is working on preparing apt economic policies to manage the transition from the wartime economy. My apologies in advance if I am violating copyrights.