Discussing great businesses with wonderful people! Tweets are NOT financial advice. DYODD. 🇨🇦 🇫🇷 🇬🇧

1985 letter - Prem’s first annual letter.

1985 letter - Prem’s first annual letter.

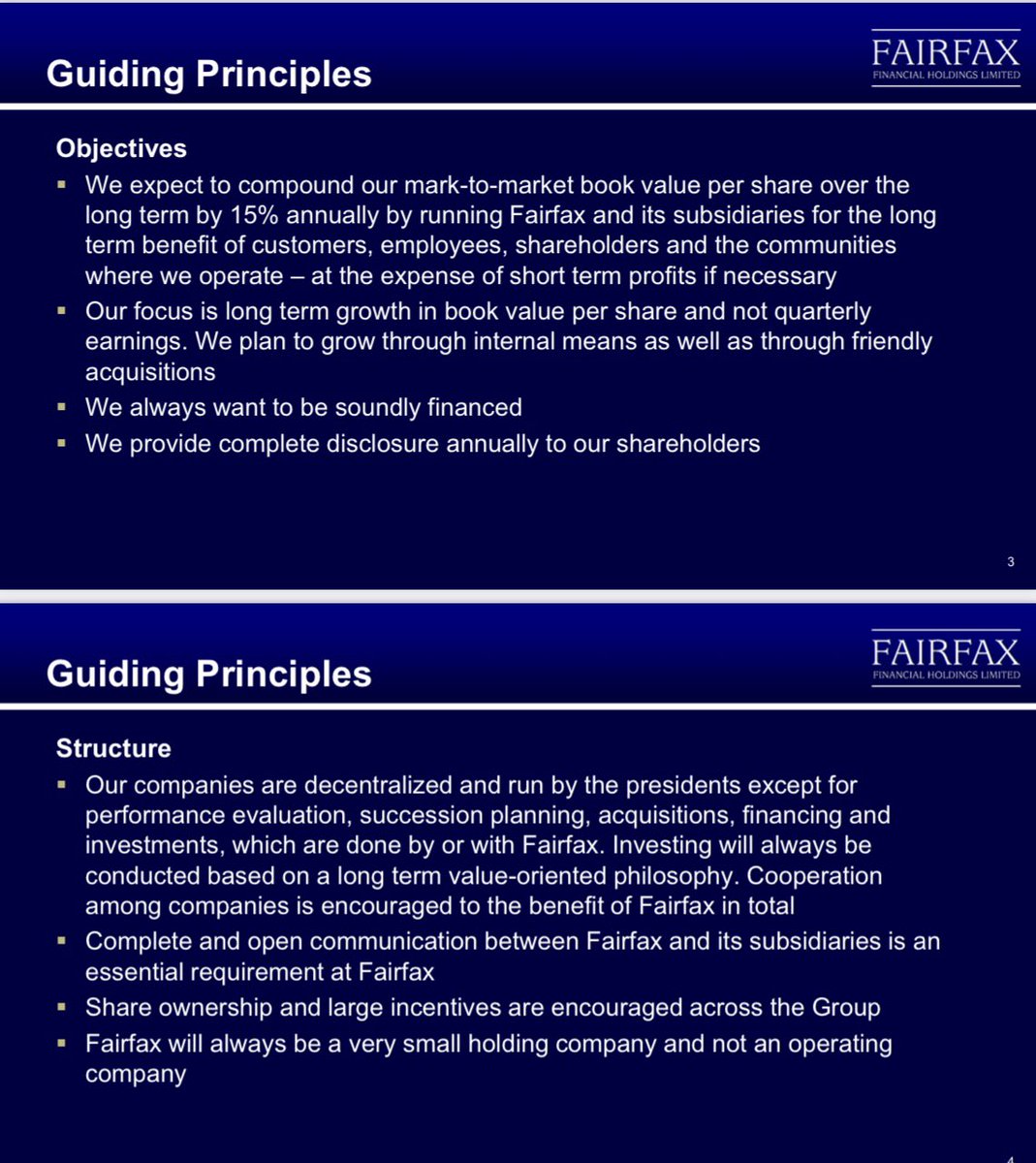

Fairfax’ Guiding Principles.

Fairfax’ Guiding Principles.

This was the clip:

This was the clip: WHAT IS KITS?

WHAT IS KITS?

Before analyzing earnings, we need to understand what IS Brookfield exactly?

Before analyzing earnings, we need to understand what IS Brookfield exactly? HISTORY

HISTORY

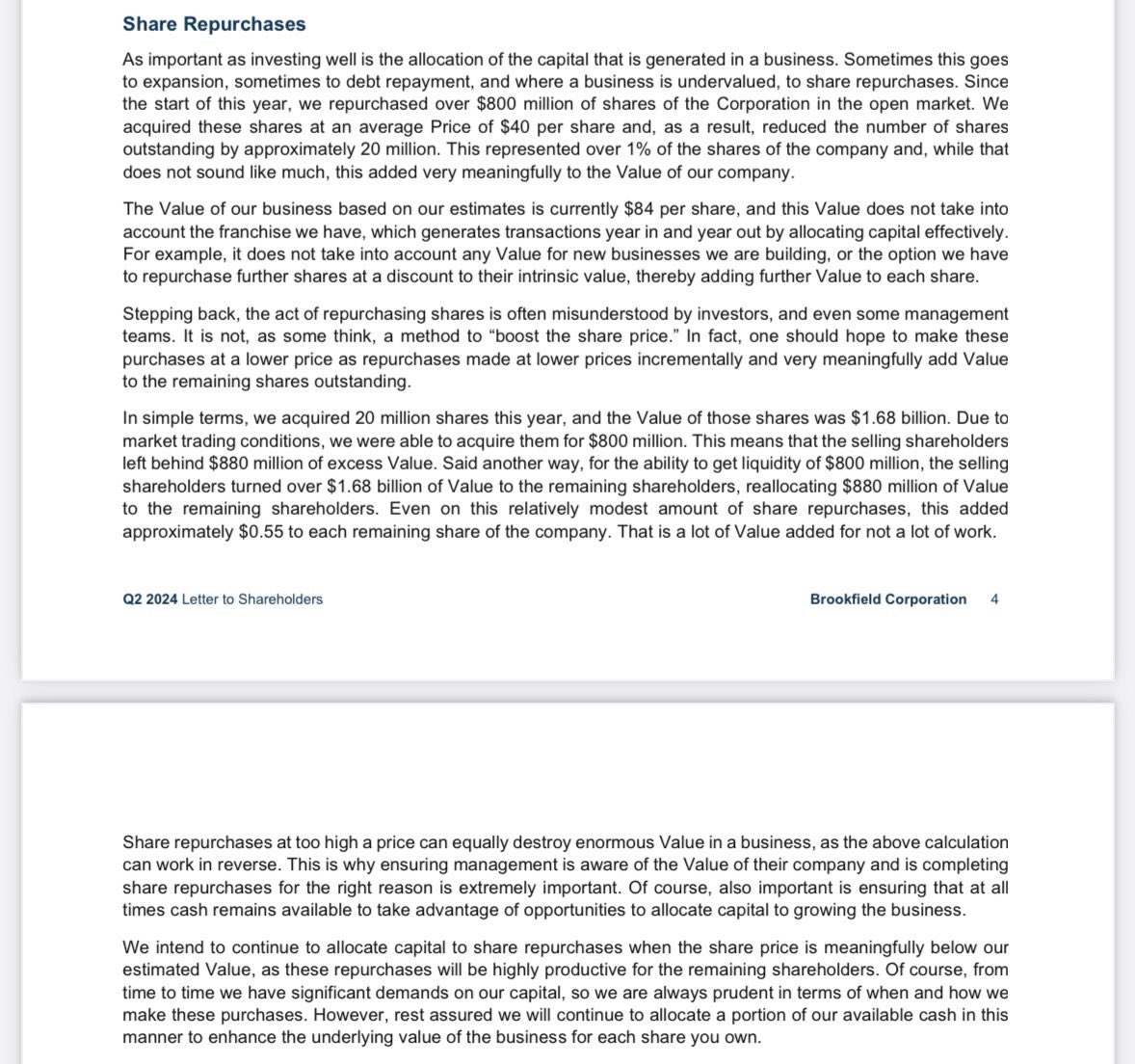

On share buybacks. Q2 2024.

On share buybacks. Q2 2024.

𝐓𝐇𝐄 𝐁𝐀𝐒𝐈𝐂𝐒:

𝐓𝐇𝐄 𝐁𝐀𝐒𝐈𝐂𝐒:

X-ELIO: A Spanish-based, global developer of renewable energy infrastructure.

X-ELIO: A Spanish-based, global developer of renewable energy infrastructure.