Mercenary at your local Multistrat hedge fund. HF recruiters wet dream...

In between gardening leaves.

Not selling any newsletter or something of that sort

3 subscribers

Sep 21, 2025 • 16 tweets • 3 min read

OK, this is gonna be a vol modeling 101. Nothing too fancy and quanty, just a simple intro of the concepts and idea behind

FWIW - i'm not trying to sell sht, just help junior and novice practitioners understand this world a bit better Let's dive in..

We start our journey into vol space at the ground floor: the Black–Scholes pricing model.

Haters gonna say it’s unrealistic with bad assumptions, but as a matter of fact it serves two key purposes:

1. mapping inputs into price 2. accounting standards

Aug 10, 2025 • 24 tweets • 5 min read

I'm a sucker for stories about how corporate hedging flows cause massive pain for dealers and affect the spot-vol dynamic and the vol surface.

Recently, we've seen a dynamic like this in no less than the most liquid FX market - the EURUSD, so I thought it worthwhile digging in

Our story begins with a little-known company - Safran.

Now, don't feel bad if you've never heard of them. They are in the aerospace business, yet they are HUGE. This multinational company is one of Europe's biggest exporters, so they have serious hedging needs.

Jul 27, 2025 • 17 tweets • 4 min read

Haven't written on anything in a while, so might be a little rusty, but let's give it a go...

Let's have a short thread about skew/smile delta and why the hell traders use it..

Back in the good ol' days of 1973 life was simpler, and delta (as B&S) modeled it was dP/dS

or in other words, the change in the value of the option wrt the change in the underlying asset. That was mostly true because one of the other key assumptions of the B&S model is that implied volatility is constant across all strikes and maturities

Mar 22, 2025 • 25 tweets • 5 min read

Ok... This post, which is going to be a long and fun one, is about how NOT to run a vol book (or thing I had to learn the hard way over the years)

Clearly, there are way too many ways to lose money, so feel free to pitch your own if I missed any.

Let's start..

Trying to capture Realized-Implied VRP

Despite sounding like a reasonable strategy, This rarely works for many reasons (gamma profile, inability to continuously delta hedge, actually modeling realized vol). Unless we have a var/vol swap-type product, it's a recipe for failure

Mar 16, 2025 • 24 tweets • 5 min read

Ok... So this topic is long overdue imho, and one that doesn't get nearly as much attention as it should even in deriv research space.

Before we dig into the effect of exotic structures on the vol surface, will note that this discussion will be focused on single asset exo

Correlation-type products, which are interesting af and worth delving into, bring another level of complexity to an already complex topic, so we'll leave them out (for now...)

In this discussion, we'll touch on the what, who, why, and how of exotic options and vol surface

Mar 8, 2025 • 15 tweets • 3 min read

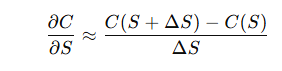

Ok... so let's talk about options greeks calculation and how most vol practitioners go about it...

Let's start with the obvious - black-Scholes greeks are contaminated with several flaws, among them two (or three) unrealistic assumptions.

Before we jump into the deep end, let's think about two real-life trading scenarios:

1. We start the day with a nice positive P&L, and throughout the day, we lose money to end the day about flat

2. We start the day with quite a negative P&L but hustle our way back to end flat

Feb 22, 2025 • 25 tweets • 5 min read

So it looks like systematic vol rv is the clear winner, so let's explore this relatively niche market segment..

Before we begin diving in, I would note that there are many shapes and forms of vol rv and systematic strategies, so I will focus on what I know to be a common one

The story of what we know as vol rv strategies starts around the late 90s/early 2000s when many head traders on the sell-side realized that they could get paid much better on the buy-side (namely hedge funds) doing what they do on the sell-side (minus the favorable friction)

Feb 15, 2025 • 23 tweets • 4 min read

Ok.. this is, by far, my all-time favorite structured product/derivatives blowup story ever...

This blowup left some decent scars at the large banks, caused quite a headache to exotic/hybrid desks, broke volatility models, and taught an important lesson about cross-gamma...

The story begins in Japan around the early 90s.

The BOJ cut rates to near zero after the asset bubble burst, and Japan went into a deflationary spiral.

Japanese, being Japanese, decided they would rather keep their money in savings for no interest than spend it

Feb 9, 2025 • 16 tweets • 3 min read

Since Benn wrote an excellent thread about GVV, I thought of giving my 2 cents about the application of this model in FX

Vol surface models like VV and SABR try to fit smiles using few liquid points and some stochastic params

Vanna Volga, which I believe originated in FX about 25-30yrs ago fits the vol smile using 3-5 liquidly traded instruments (ATM , RRs , BFs of different delta strikes).

The model was developed to address the high-order greek problem for options desk running 1st gen exo books

Jan 26, 2025 • 18 tweets • 4 min read

So I got quite a few questions/confused DMs about my OP regarding the "weekend effect" and the idea of virtual time. Given that this is somewhat of a "derivatives fetish" of mine, I thought it might be useful to delve a little deeper into the practical/technical applications

Let's level the ground w.r.t. market vol quotation - different markets may have different quoting conventions/standards, but market-makers/dealers will usually quote vol runs (or vol term structure) in the way of generic/liquid expires (i.e., 1w,2w,1m,3m, etc..)

Jan 18, 2025 • 20 tweets • 4 min read

One of the most sought-after ideas in financial markets is the idea of arbitrage because who doesn't like free money?

In most cases, this term is confused with convergence strategies like stat-arb, so I thought that it would be helpful to shed some light on the topic.

We can grossly differentiate between two types of arbitrages:

1. Pure Arbitrage - risk-free profit

2. Statistical Arbitrage - trading is highly correlated underlying assets, assuming that their price difference should converge towards the mean.

Jan 11, 2025 • 7 tweets • 2 min read

As a junior trader on a desk, I had a market-philosophical discussion with my PM on whether realized vol is an absolute truth and whether derivatives trading is a zero-sum game.

To test the hypothesis, we decided to experiment with both long and short the same option.

We picked an underlying option we liked (with the tiniest bid/ask spread)and simultaneously bought/sold it. The rule was that we could run the risk however we wanted as long as we held it to expiry.

Fast-forward to expiry - we both made positive pnl on the trade

Jan 4, 2025 • 18 tweets • 4 min read

A few days ago, I bitched about vol trading being hard but came short of giving a practical example as to why... Given it's the weekend (and I'm bored af) I thought of giving a small glimpse into the daily struggles of vol trading.

Vol strategies, generally speaking, try to extract value from vol surfaces (i.e., atm vol and/or high-order moments like skew/convexity). There are many ways to skin that cat (metaphorically, of course), but most buy-side vol desks run what we like to call "vol rv" strategies

Dec 29, 2024 • 6 tweets • 1 min read

Vol trading is hard (so don't let anyone on X/TikTok/YouTube tell you otherwise)....

Practitioners in the market (myself included) dedicate their days to model dynamics in vol surfaces, and you probably think - why?

Textbook derivatives literature will tell you that the vol smile embeds the information on how the market prices the change in volatility w.r.t. spot move, but this is merely the *Expected* change in the vol smile... sometimes it rolls over/sometimes it rolls under...

Jan 7, 2023 • 4 tweets • 1 min read

It's amazing how @EmanuelDerman static option replcation paper is as relevant today as it was 28yrs ago...

despite having to add few correction to the original method this paper proposed the simplest, yet most robust way to replicate exotic options

the amount of paper over the years that came up with extremely sophisticated processes and models to be as accurate as possible (like MC simulations with 1m x 1m grids...) most converge to a very close price...