Neither noise nor guessworks - only insights.

Illuminating your investing journey with facts, data, charts, and more.

#MarketInsights

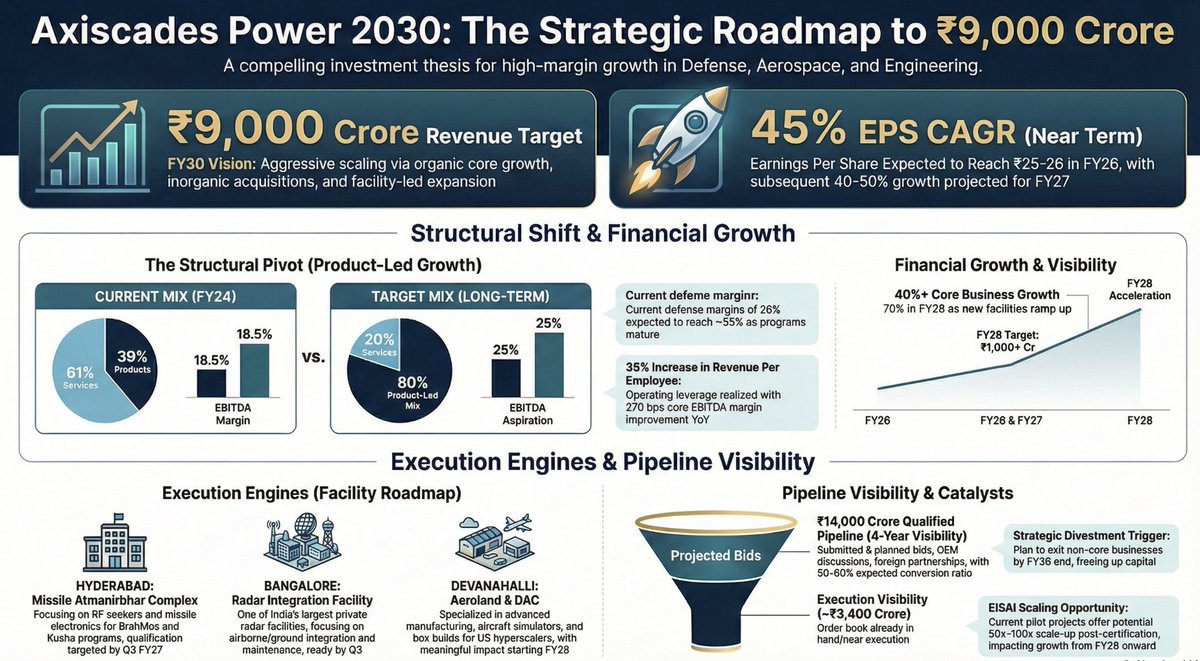

📈 Revenue Growth Guidance

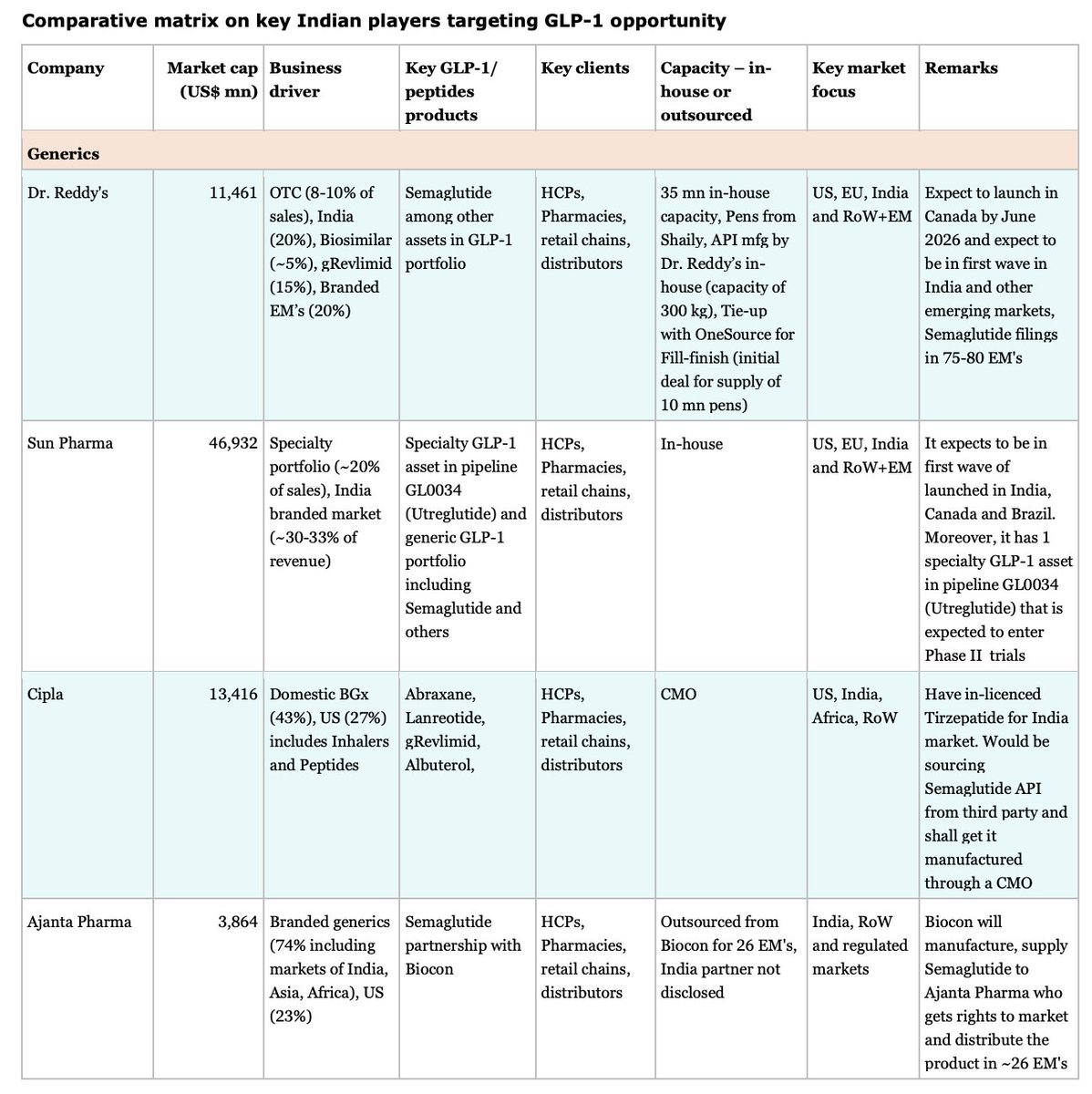

📈 Revenue Growth Guidance Generics

Generics

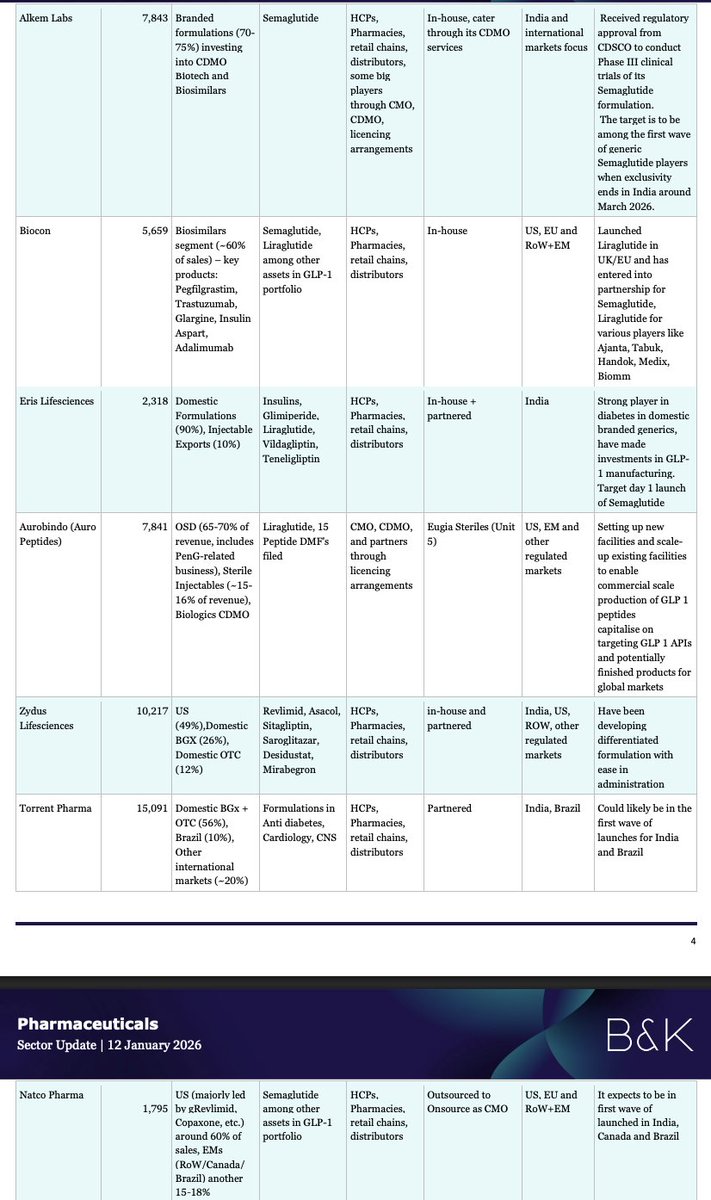

1️⃣ HBL ENGINEERING | What actually happened

1️⃣ HBL ENGINEERING | What actually happened This flywheel design explains Meesho’s structural cost advantage.

This flywheel design explains Meesho’s structural cost advantage.