🧵 ULTY "Death Spiral" from July 21, 2025: NAV Decline, Dividends' Role, & When to Expect Reversal

ULTY's NAV has declined ~11.85% since July 21, 2025 (from $6.33 to $5.58 as of Sep 3 close), sparking "death spiral" fears amid high yields (~85% annualized). Are dividends making up the difference? When might it reverse? Let's analyze data to Sep 3, 2025, causes, total returns, & outlook—it's not a spiral, but structural erosion in a tough period.

1/7. The NAV Decline: Data from July 21 to Sep 3, 2025

NAV history (daily closes):

- Jul 21: $6.33

- Jul 31: $5.90 (-6.8%)

- Aug 7: $5.91 (+0.2%)

- Aug 14: $5.75 (-2.7%)

- Aug 21: $5.74 (-0.2%)

- Aug 28: $5.67 (-1.2%)

- Sep 3: $5.58 (-1.6%)

Total: -11.85% over ~6 weeks (~2% weekly avg.). Recent "blood bath" days like Aug 19 (-2.88%) amplified, but trend gradual.

This slide follows post-revamp pattern (~15-20% ann. erosion), but accelerated by market weakness.

Aug 23, 2025 • 8 tweets • 3 min read

🧵 Frustrations with ULTY NAV Declining: Why It's Not a Growth Income Fund & NAV is Designed to Go Down – Educational Post

ULTY (YieldMax Ultra Option Income Strategy ETF) promises sky-high yields (~85% annualized as of Aug 2025), but its NAV has slid from ~$6.33 on July 21 to ~$5.61 as of Aug 22 close—a 11.4% drop in a month. This frustrates many investors expecting "growth income." But ULTY isn't built for NAV growth—it's options-powered for current income, where erosion is part of the plan. Let's explore frustrations, why it happens, & mindset shift 👇

1/7. Common Frustrations: "Why Is My Investment Shrinking?"

Investors vent on forums: "ULTY NAV keeps declining—feels like a losing bet!" or "Expected growth with income, but price drops while divs come." This stems from misunderstanding: People see high yields and assume NAV stability like dividend stocks (e.g., SCHD up ~2% YTD).

Reality: ULTY is an income fund, not "growth income." Erosion is structural—high payouts reduce NAV to deliver cash now.

Aug 21, 2025 • 10 tweets • 3 min read

🧵 Re-Evaluating ULTY Performance Since the New Strategy: NAV Decline Since 7/21/25 (Post-New Strategy Peak) & 10-Year DRIP Projections

ULTY's March 2025 strategy revamp (direct holdings, protective puts, credit spreads) aimed to stabilize the fund amid high yields. But with NAV declining ~9.5% since July 21, 2025 (from ~$6.33 to $5.73 as of Aug 19), is it working? Let's re-evaluate performance, causes of the slide, and run updated 10-year projections for $100K with 100% DRIP starting July 25, 2025, in bull, stagnant, and bear markets. Hypotheticals based on data 👇

1/9. The Strategy Change: What Happened in March 2025?

Pre-March: ULTY used synthetic positions, leading to heavy NAV erosion (~70% drop from launch Feb 2024 at $20 to ~$7 by March).

Post-Change: Shifted to direct ownership of 15-30 high-vol U.S. stocks (e.g., NVDA, MSTR), added OTM puts for downside cushion (~5-10%), credit call spreads for moderate upside capture, and flexible call writing. Weekly distributions started.

Goal: Boost income (~85% yield) while reducing erosion risks.

Aug 19, 2025 • 8 tweets • 2 min read

🧵 Why ULTY Must Distribute All Cash Before End of October: Educational Explainer & Shareholder Impact

YieldMax ETFs like ULTY operate on a fiscal year ending October 31, requiring them to distribute all net income & gains by then to maintain RIC status & avoid fund-level taxes. But what does this mean for holders? Let's break it down 👇

1/7. Fiscal Year Basics for ETFs Like ULTY

ULTY (and other YieldMax funds) has a fiscal year from Nov 1-Oct 31. As a Regulated Investment Company (RIC), it must distribute at least 90% of taxable income (dividends, interest, cap gains) annually to pass through taxes to shareholders & avoid 21% corporate tax.

"Distribute all cash": Refers to excess net income/gains not yet paid out via regular distributions—ensures compliance by fiscal year-end (Oct 31).

Not unique to ULTY—standard for many ETFs/mutual funds with Oct fiscal ends.

Aug 17, 2025 • 9 tweets • 2 min read

🧵 Building a Portfolio with ULTY for Ultra High Income: Best Funds to Pair & Why

ULTY (YieldMax Ultra Option Income Strategy ETF) delivers massive yields (~85% annualized as of Aug 2025) via options on volatile stocks, but alone it's high-risk. Pairing with complementary funds diversifies while chasing ultra income (50%+ total yield). Let's educate on strategy, top pairs, & a sample build 👇

1/8. Why Build Around ULTY? Core Strengths & Needs

ULTY shines for income: Weekly distros from covered calls/spreads/puts on 15-30 high-vol names (e.g., NVDA, MSTR). YTD total return ~13%, but vol ~30% & NAV erosion risks.

Pair to: Mitigate risks, blend yields, add stability. Goal: Ultra high income (50-100% portfolio yield) via diversified options/dividends. Avoid over-exposure to vol.

Diversify across strategies: Covered calls, single-stock yields, broad dividends.

Aug 11, 2025 • 8 tweets • 2 min read

🧵 Sharpe Ratio of $ULTY Since Strategy Change: Educational Analysis & Calculation

The Sharpe ratio measures risk-adjusted returns—key for volatile ETFs like $ULTY. Post-March 2025 revamp (direct holdings, puts, spreads), has it improved? Let's explain, calculate since then (Mar 1-Aug 9, 2025), & compare. Data as of Aug 10, 2025 👇

1/7. What is Sharpe Ratio?

Sharpe = (Portfolio Return - Risk-Free Rate) / Volatility (std dev of returns). Higher >1 = good risk-reward.

For ULTY: High vol (~30% ann.) from stock picks, but strategy buffers.

Use monthly/daily for short periods like 5 months.

Aug 8, 2025 • 9 tweets • 2 min read

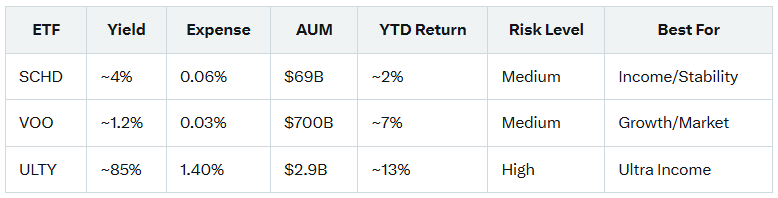

🧵 SCHD vs VOO vs ULTY: Battle of Dividend, Growth, & High-Yield ETFs – Which Fits Your Portfolio?

In a volatile 2025 market, these ETFs shine differently: SCHD for steady dividends, VOO for broad growth, ULTY for ultra income via options. Let's compare strategies, yields, risks, & performance to help you choose 👇

1/8. SCHD: The Dividend Stalwart

Schwab U.S. Dividend Equity ETF (SCHD) tracks Dow Jones U.S. Dividend 100 Index—100 high-quality, dividend-paying U.S. stocks (e.g., HD, MRK) screened for consistency & strength.

Focus: Income + stability. ~100 holdings, large-cap bias.

AUM: ~$69B. Expense: 0.06%. Yield: ~3.95%. YTD Return: ~1.59% (as of early Aug 2025).

Best for: Retirees/income seekers wanting low vol.

Aug 6, 2025 • 8 tweets • 2 min read

🧵 Likelihood of $ULTY Reverse Split: Addressing a Common Investor Fear

With $ULTY's NAV stabilizing around $6 post-March 2025 strategy tweaks, fears of a reverse split persist. But is it likely? Short answer: Low probability (~5-10%) in the near term. Let's break down the myth, mechanics, & data 👇

1/7. What is a Reverse Split & Why Fear It?

A reverse split (e.g., 1-for-10) combines shares to boost price (e.g., $2 to $20), reducing outstanding shares proportionally. No value change—your stake stays the same.

Fear: Signals weakness, triggers selling, or hurts liquidity. For ETFs, it's often to meet exchange rules ($5+ price) or attract institutions.

But: Not always bad—can stabilize perception. $ULTY hasn't split yet.

Aug 4, 2025 • 8 tweets • 2 min read

🧵 Busting the Myth: Can $ULTY Really Go to Zero? A Common Misconception Debunked

High-yield ETFs like $ULTY (YieldMax Ultra Option Income Strategy) boast 60-80%+ yields, but skeptics fear NAV erosion will drive it to zero. Spoiler: That's a huge misconception. The odds are near-zero. Let's educate on why 👇

1/7. The Misconception: "High Yields = Unsustainable Decay to Zero"

Many think $ULTY's distributions (often 100% Return of Capital or ROC) eat away at principal until nothing's left. This stems from confusing ROC with "destructive" payouts in failing funds.

Reality: ROC is just a tax label for option premiums—deferring taxes, not signaling failure. It's sustainable as long as volatility persists for premiums.

Pre-2025, NAV dipped from high distros, but post-strategy tweaks (direct holdings, puts), it's stabilized ~$6.

Jul 31, 2025 • 9 tweets • 2 min read

🧵 What is AUM & Why It's Crucial for $ULTY Investors

If you're eyeing high-yield ETFs like $ULTY, AUM (Assets Under Management) is a key metric. It signals health, liquidity, & more. Let's break it down simply & explain its role for $ULTY 👇

1/7. What Exactly is AUM?

AUM stands for Assets Under Management—the total market value of all assets in a fund or ETF at a given time. For ETFs, it's the sum of investor money flowing in, managed by the issuer (here, YieldMax).

Think of it as the fund's "size"—bigger often means stronger.

Jul 30, 2025 • 9 tweets • 3 min read

🧵 Comparing YieldMax's Diversified ETFs: YMAX, YMAG, & How $ULTY Stands Apart in Detail

YieldMax shines with single-stock income ETFs, but their diversified lineup—YMAX, YMAG, & ULTY—offers broader exposure. All chase high yields via options, but strategies differ. Let's compare, with a deep dive on ULTY's unique active edge 👇

1/8. First: The Diversified Trio Overview

YieldMax's non-single-stock ETFs as of mid-2025:

- $YMAX: Universe Fund of Option Income ETFs

– AUM ~$991M, expense 1.28%.

- $YMAG: Magnificent 7 Fund of Option Income ETFs

– AUM ~$523M (est.), expense 1.28%.

- $ULTY: Ultra Option Income Strategy ETF

– AUM ~$2.4B, expense 1.30%.

All aim for monthly/weekly income, capped upside, full downside (mitigated). But ULTY isn't a fund-of-funds—it's actively managed on stocks directly.

Jul 29, 2025 • 10 tweets • 3 min read

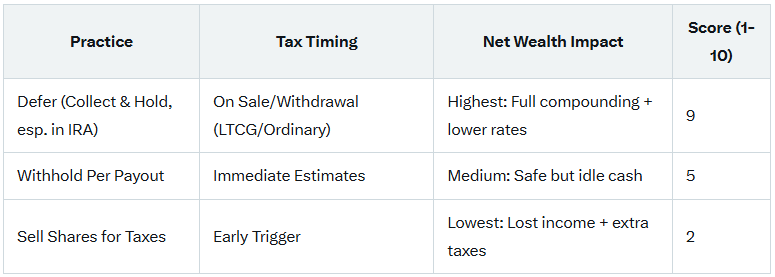

🧵 The Most Financially Beneficial Way to Handle Taxes on ROC Distributions (Like in $ULTY)

High-yield ETFs like $ULTY generate big payouts, often as Return of Capital (ROC)—but taxes? Deferral is king. Let's explore why holding & deferring beats immediate payment or selling, maximizing your after-tax wealth. Plus: Can you defer ETF income? Yes, via account types! 👇

1/9. ROC Basics: Not Your Typical Tax Hit

ROC distributions (common in YieldMax ETFs) aren't taxed now—they reduce your cost basis. For $ULTY, recent payouts (e.g., July 2025): 100% ROC from option premiums.

Tax event? Only when you sell: Gain = Sale price - Adjusted basis, potentially long-term capital gains (0-20% rates). If basis hits zero, future ROC = gains.

YieldMax's guide: ROC = tax-deferred cash, not income.

Jul 28, 2025 • 10 tweets • 3 min read

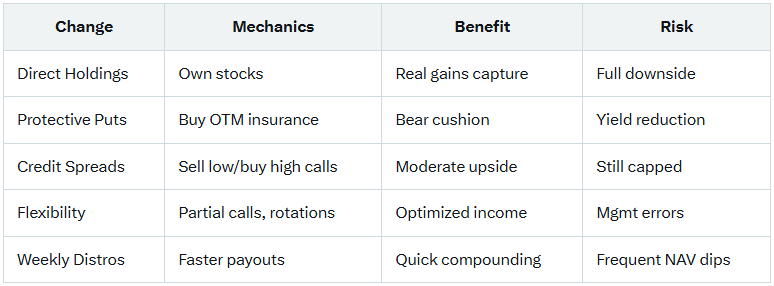

🧵 Deep Dive: $ULTY's March 2025 Strategy Overhaul – How It Transforms Income Generation

YieldMax's $ULTY ETF revamped its approach in March 2025, shifting from pure covered calls to a tactical, resilient model. This addresses past NAV erosion while boosting income potential. Let's unpack each change, mechanics, benefits, & risks 👇

1/9. Background: Why the Changes?

Pre-March: $ULTY used synthetic positions (swaps) for exposure to 15-30 high-vol stocks, selling calls for premiums. But volatility led to NAV decay & uneven payouts.

March 2025 tweaks: Direct holdings, protective options, spreads, flexibility, & weekly distros. Aims: Better alignment, downside buffers, upside capture. Since then, AUM ~$1.6B, YTD returns ~15.6%.

Jul 27, 2025 • 8 tweets • 2 min read

🧵 Yield vs. Yield on Cost: Decoding These Metrics for Better Investing Decisions

In high-yield plays like $ULTY, yields can dazzle—but mixing up "yield" and "yield on cost" (YOC) leads to confusion. One's for new buyers; the other's for holders. Let's break down how to interpret them wisely 👇

1/7. What is Yield (Dividend Yield)?

It's the current annual dividend (or distribution) divided by the current market price, expressed as a %. Formula: (Annual Dividend / Current Price) x 100.

This shows what income you'd get if buying today. For $ULTY, it's ~60-80% based on recent payouts—super high due to options.

Jul 25, 2025 • 8 tweets • 2 min read

🧵 Debunking $ULTY ROC Myths: It's a Tax Classification, NOT Economic Erosion!

High-yield ETFs like $ULTY often show distributions as Return of Capital (ROC), sparking fears of NAV decay. But YieldMax has clarified: It's just tax treatment, not "true" ROC eating your principal. Let's unpack the facts & why it's often a win 👇

1/7. What is ROC in ETFs?

ROC is a tax label for nondividend distributions—cash paid out that reduces your cost basis, deferring taxes. It's NOT an indicator of fund performance or economic loss. For option ETFs like $ULTY, premiums from calls often get classified this way.

Jul 23, 2025 • 8 tweets • 2 min read

🧵 $ULTY vs $YMAX: Battle of YieldMax's High-Income ETFs – Which Fits Your Portfolio?

YieldMax offers killer income strategies, but $ULTY and $YMAX take different paths. One's a diversified stock picker with options flair; the other's a fund-of-funds powerhouse.

Confused which to pick? Let's compare strategies, yields, risks, and more 👇

1/7. First, what is $ULTY?

YieldMax Ultra Option Income Strategy ETF ($ULTY) is an actively managed fund targeting high monthly (now weekly) income via covered calls on 15-30 volatile U.S. stocks like NVDA or MSTR.

It holds the stocks directly for real exposure, sells calls for premiums, and uses tweaks like protective puts to manage downside. AUM: ~$1.61B. Expense: 1.30%. Volatility: ~4.59%.