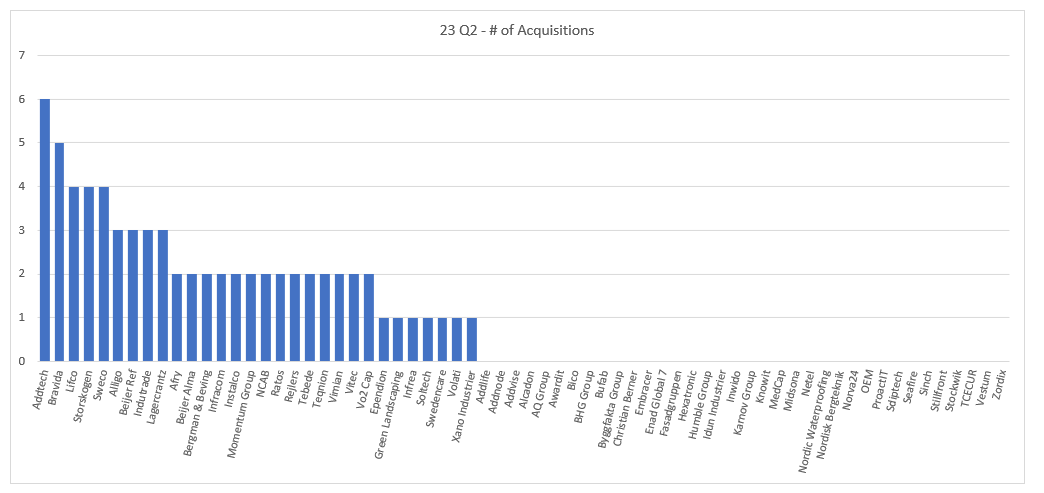

If we look at 2023 YTD the total # of acquisitions completed is 168.

If we look at 2023 YTD the total # of acquisitions completed is 168.

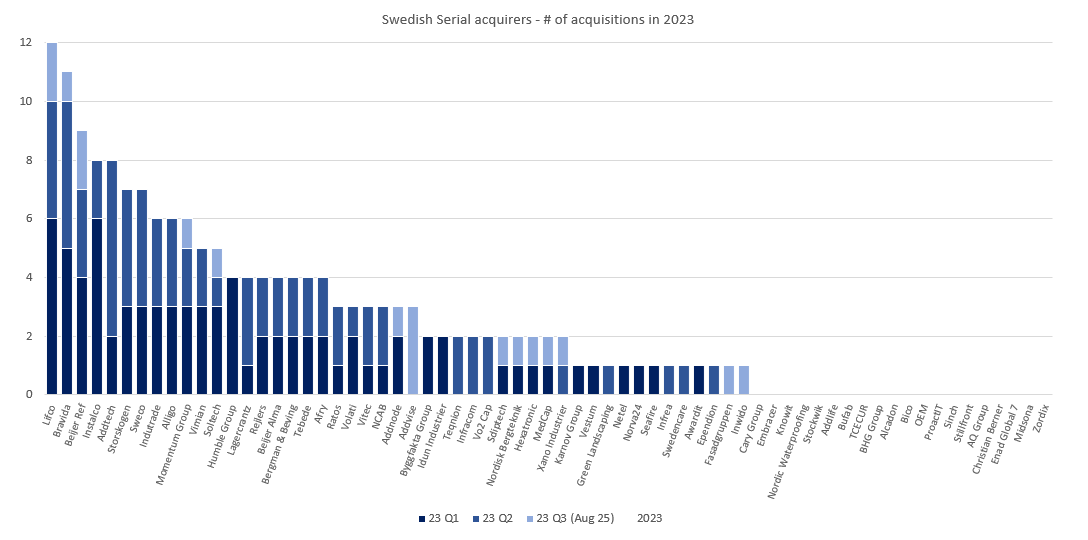

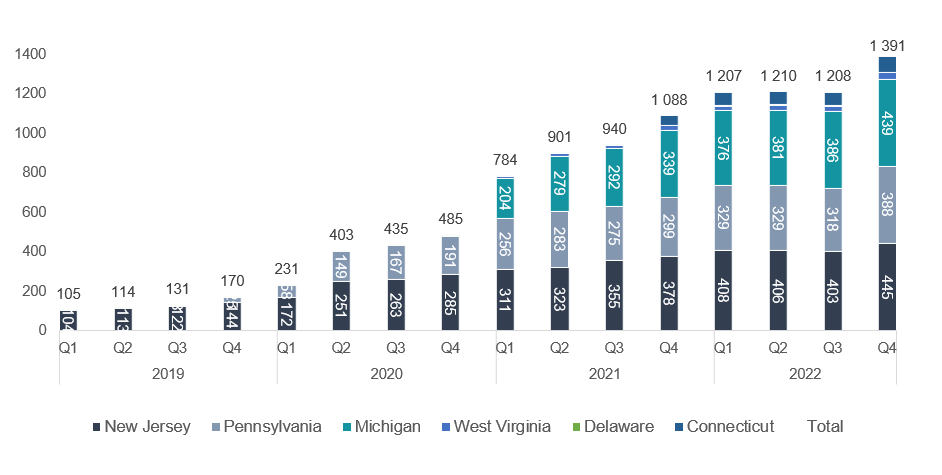

2022 started of really good in Q1 and then had a really flat development throughout the year - until Q4.

2022 started of really good in Q1 and then had a really flat development throughout the year - until Q4.

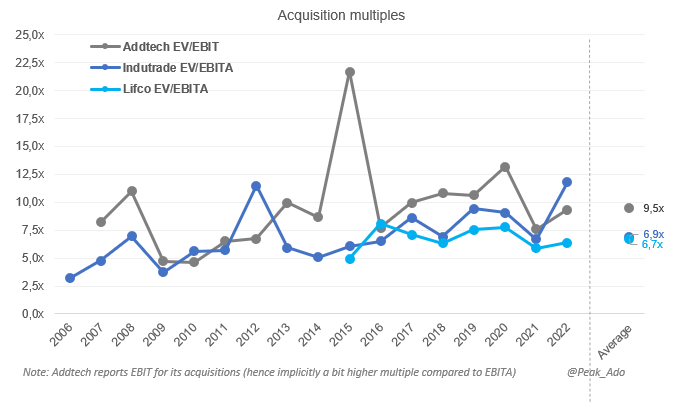

From a historical perspective it was pretty obvious that the margin during the pandemic was not sustainable (but Mr Market likes to extrapolate). EBITA-margin was pretty stable 2016-2019 around 9-10%.

From a historical perspective it was pretty obvious that the margin during the pandemic was not sustainable (but Mr Market likes to extrapolate). EBITA-margin was pretty stable 2016-2019 around 9-10%.

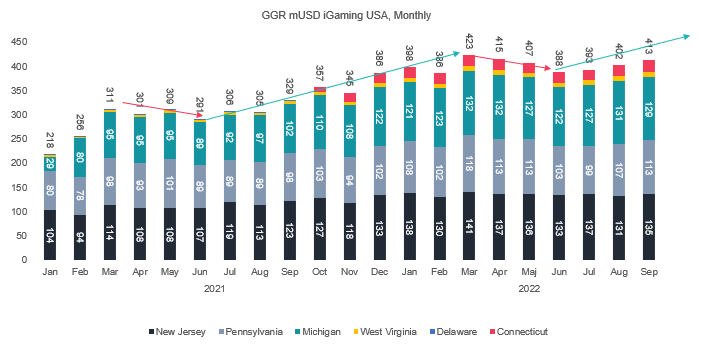

Generally, Q3 is a weaker period in gaming so nothing that worries me as I believe there is further room for growth in the US market.

Generally, Q3 is a weaker period in gaming so nothing that worries me as I believe there is further room for growth in the US market.

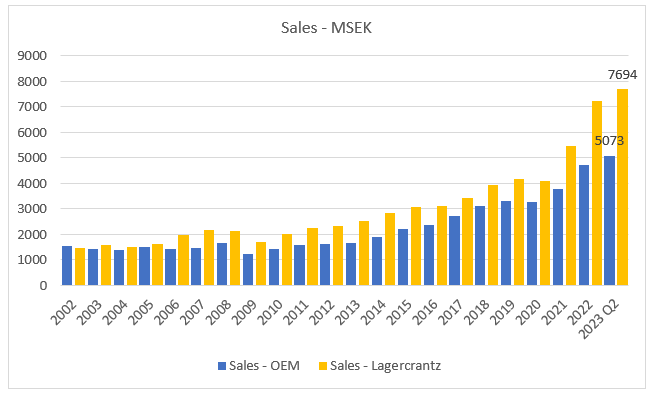

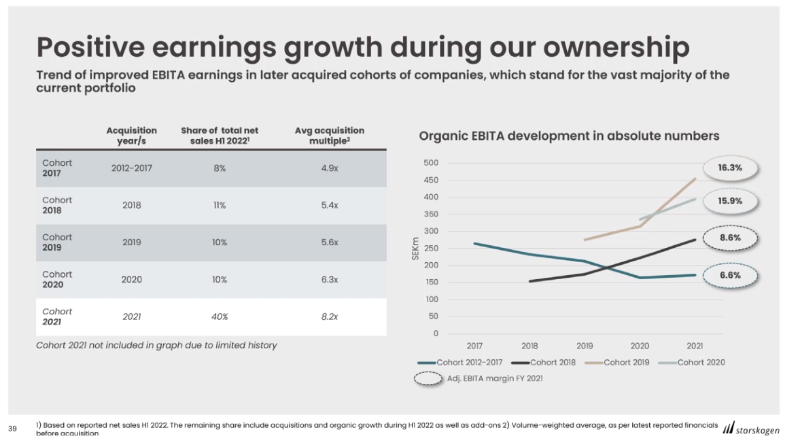

Lagercrantz has been viewed as a great company that manage to increase its margins over time by increasing the share of proprietary products with higher gross margins, improving the group EBITA-margin.

Lagercrantz has been viewed as a great company that manage to increase its margins over time by increasing the share of proprietary products with higher gross margins, improving the group EBITA-margin.  For me the hard job of value creation starts after earn-outs are paid out and sellers out of the game. For that reason the Cohorts prior to 2019 are more interesting than those after.

For me the hard job of value creation starts after earn-outs are paid out and sellers out of the game. For that reason the Cohorts prior to 2019 are more interesting than those after.

Har också studerat EBIT-marginalen för alla bolag i koncernen (som om de hade ägt de hela vägen) och det är en imponerande trend att de lyckas öka marginalerna.

Har också studerat EBIT-marginalen för alla bolag i koncernen (som om de hade ägt de hela vägen) och det är en imponerande trend att de lyckas öka marginalerna.