Now: Pre-Seed Investor @DeVC_Global || Prev: Founder @VerakInsurance (acq. by ID) || Views are my own

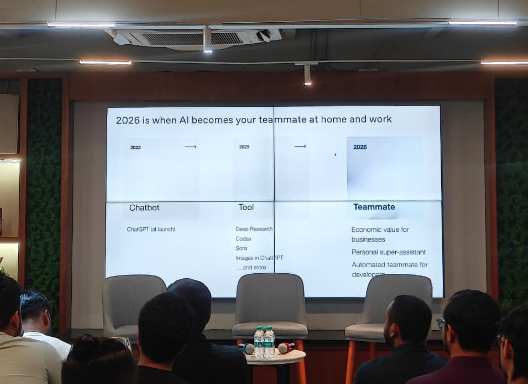

1️⃣The arc of AI thus far

1️⃣The arc of AI thus far

Isler is an ODM (Orignal Design Manufacturer) i.e. it works closely with each of its brand partners to ideate, design, spec & assemble products - it is MUCH more than simple component assembly which typically happens in the EMS space.

Isler is an ODM (Orignal Design Manufacturer) i.e. it works closely with each of its brand partners to ideate, design, spec & assemble products - it is MUCH more than simple component assembly which typically happens in the EMS space.

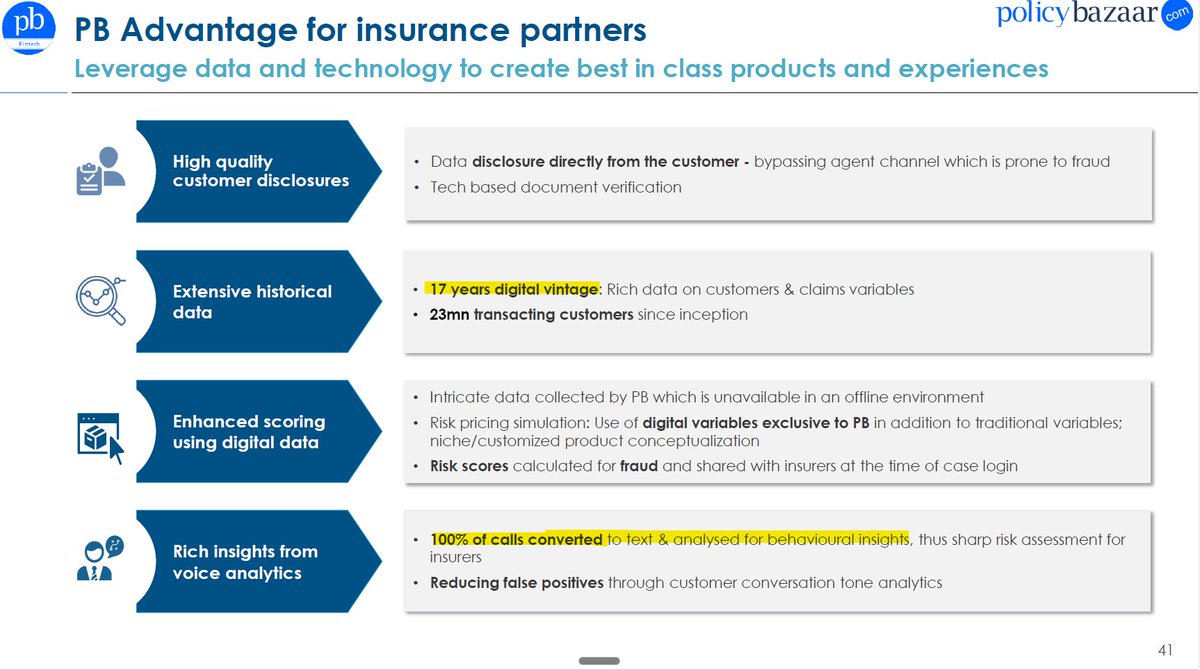

Founder Interviews:

Founder Interviews:

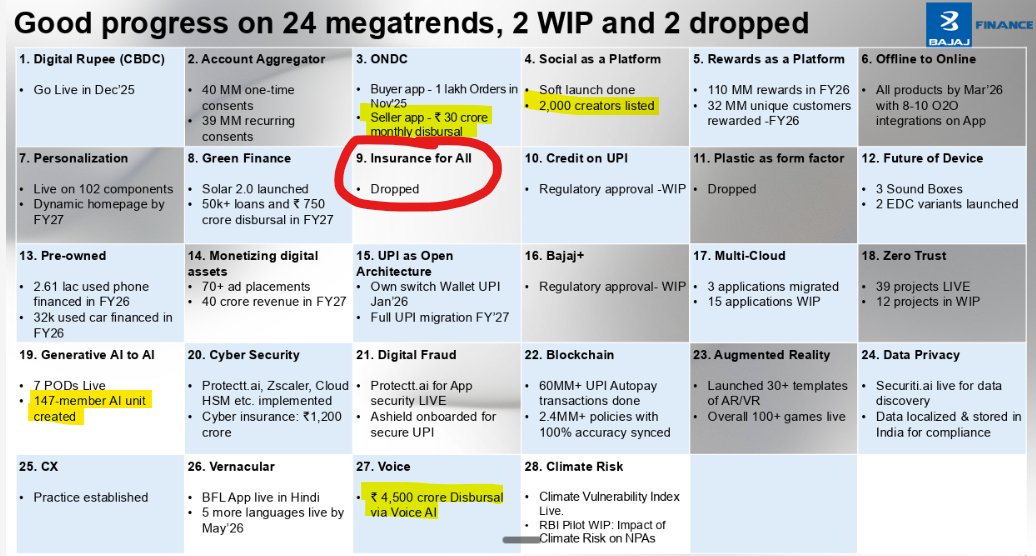

1️⃣Certain updates from BFL regarding megatrends caught my attention:

1️⃣Certain updates from BFL regarding megatrends caught my attention: