Formerly many things. 1st to rhyme Duce & Juche; describe US as Transfer Union. Says Poujadist often. Aging Macro Expat. Equal parts phlegm, spleen, dad humor.

It’s remarkable how many American progressives have embraced 3 deeply reactionary ideas re:CN —that poor people deserve crap capital stock; that increasing it cannot reduce poverty; and that something called “social capital” is an immutable constraint on its productive use.

It’s remarkable how many American progressives have embraced 3 deeply reactionary ideas re:CN —that poor people deserve crap capital stock; that increasing it cannot reduce poverty; and that something called “social capital” is an immutable constraint on its productive use.

This tweet, and the numbers therein, should be considered not only an indication of what chafes, but also an indication of why it is extremely premature to conclude that those chafing are anywhere close to the Tinactin.

This tweet, and the numbers therein, should be considered not only an indication of what chafes, but also an indication of why it is extremely premature to conclude that those chafing are anywhere close to the Tinactin.

Just some interesting pointers here--1. EUR is clearly the only other currency that comes close but is still behind USD (I also suspect that a big chunk of cross-border claims in EUR are intra EU or intra EZ). 2. The US banking system is not as large a global USD intermediary

Just some interesting pointers here--1. EUR is clearly the only other currency that comes close but is still behind USD (I also suspect that a big chunk of cross-border claims in EUR are intra EU or intra EZ). 2. The US banking system is not as large a global USD intermediary

More pungently.

More pungently.

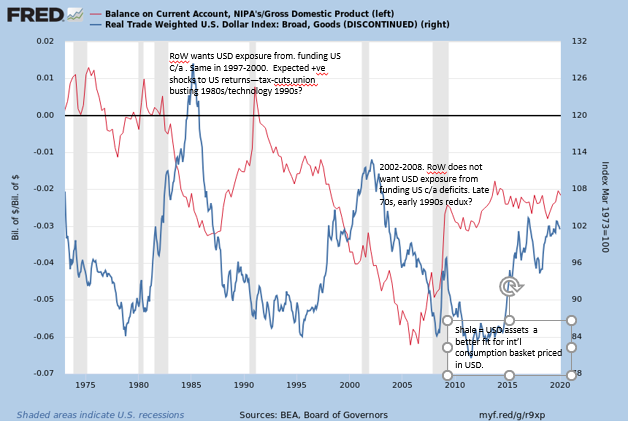

Couple of other thoughts. At times large scale reserve accumulation occurs precisely because the global private sector does not want to accumulate assets or is shedding net assets in a currency. Think of BoJ purchases of USDJPY in the early 2000 or SNB activity in €.

Couple of other thoughts. At times large scale reserve accumulation occurs precisely because the global private sector does not want to accumulate assets or is shedding net assets in a currency. Think of BoJ purchases of USDJPY in the early 2000 or SNB activity in €.

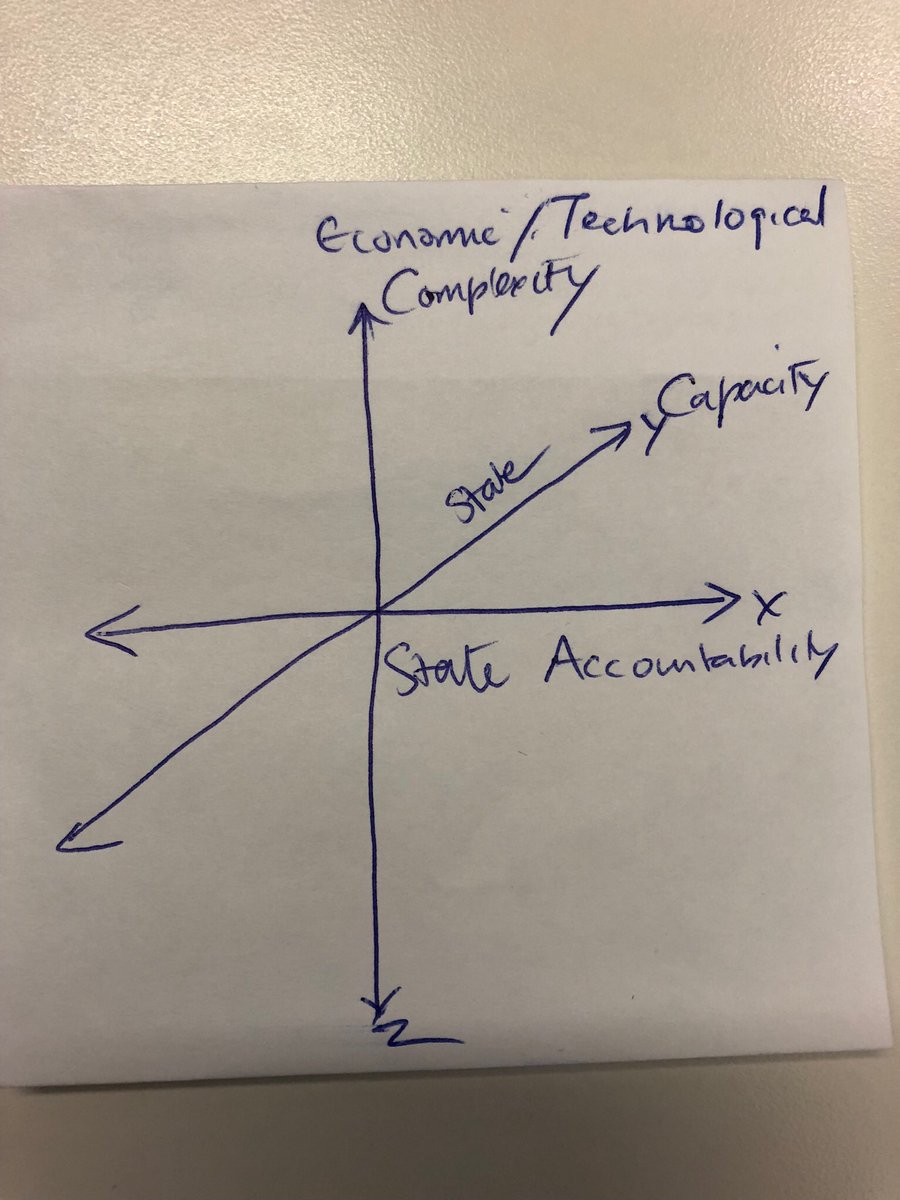

Cc:@DanielaGabor the diagram is up.

Cc:@DanielaGabor the diagram is up.