A system dynamicist specializing it's application for Macroeconomic Forecasting.

If depressions are mainly caused by government excess, that timeline doesn't work. The U.S. wasn't running huge deficits before the crash. It was tightening fiscally, and a depression followed.

If depressions are mainly caused by government excess, that timeline doesn't work. The U.S. wasn't running huge deficits before the crash. It was tightening fiscally, and a depression followed. They say: Equilibrium isn't stable, it can explode.

They say: Equilibrium isn't stable, it can explode. DSGE models boil the entire economy down to 3 equations:

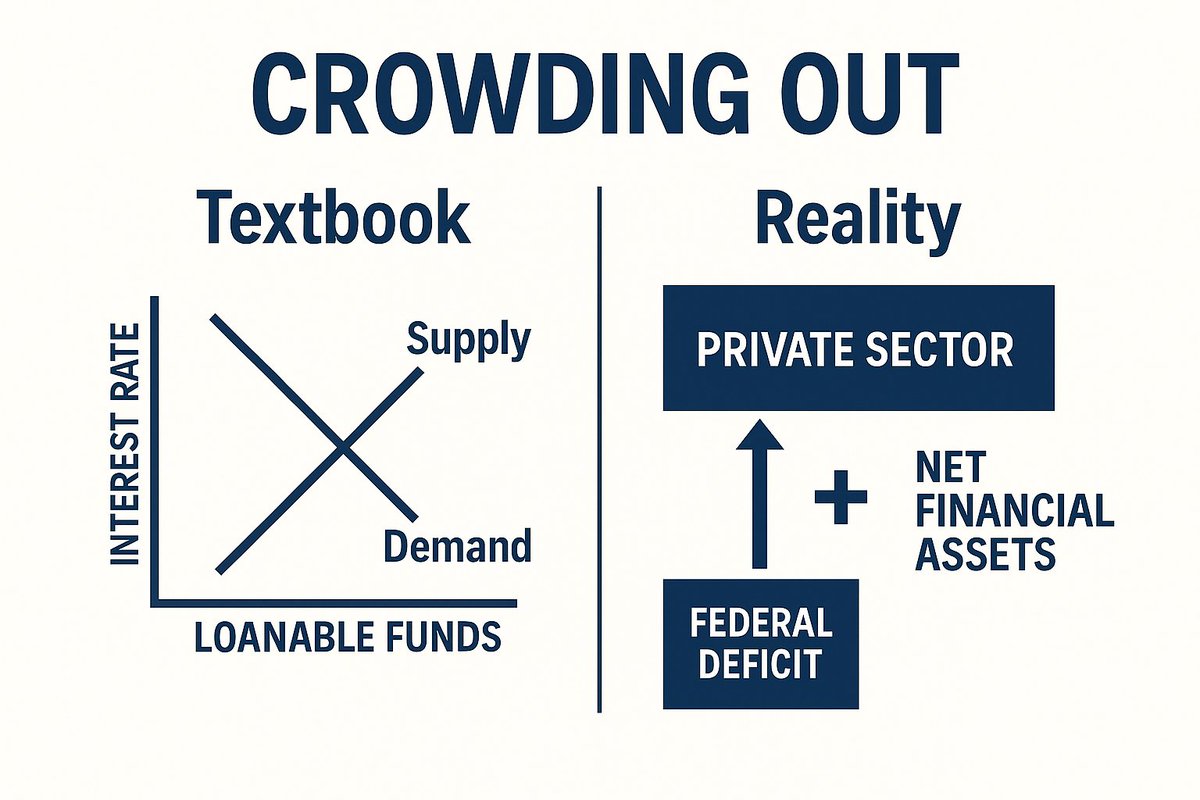

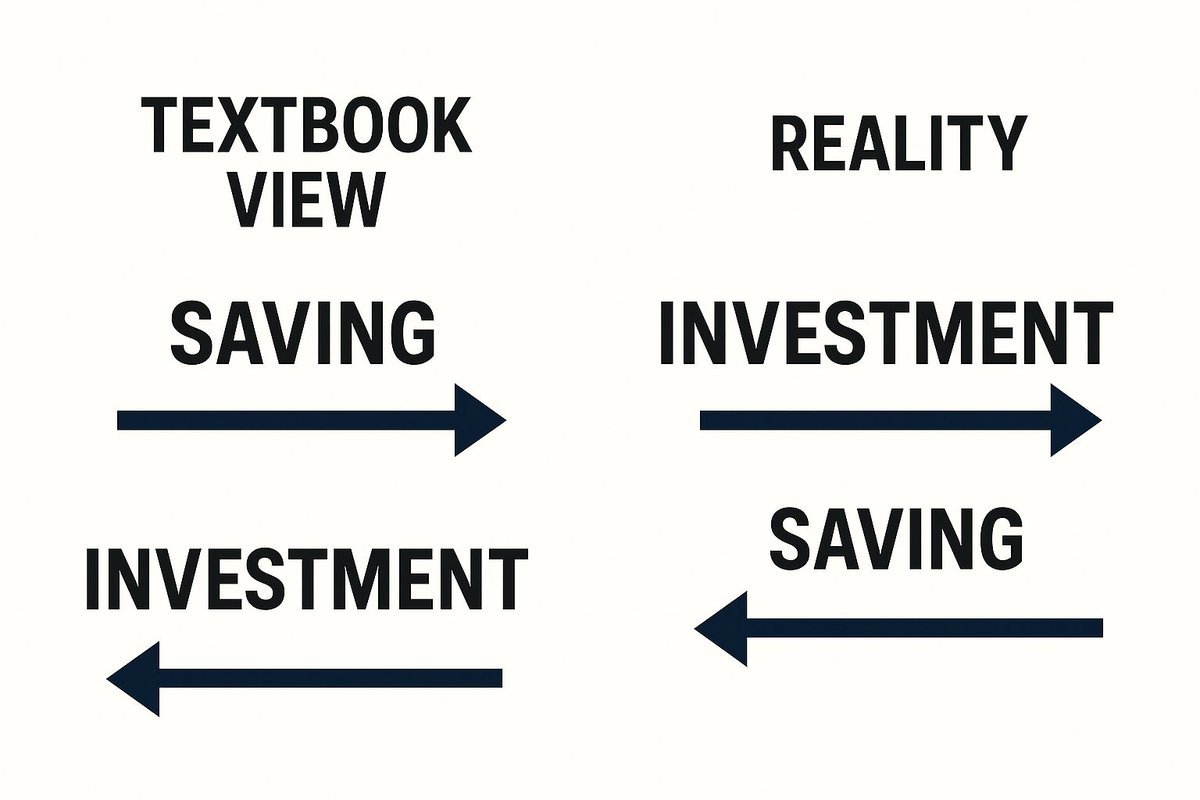

DSGE models boil the entire economy down to 3 equations: The textbook story starts with loanable funds: households save, banks lend those savings, and interest rates tidy everything up.

The textbook story starts with loanable funds: households save, banks lend those savings, and interest rates tidy everything up. Start with old-school neoclassical DSGE.

Start with old-school neoclassical DSGE. The fallacious story goes like this: banks take deposits, keep 10% as reserves, and lend out the rest. That fraction supposedly limits how much credit they can create.

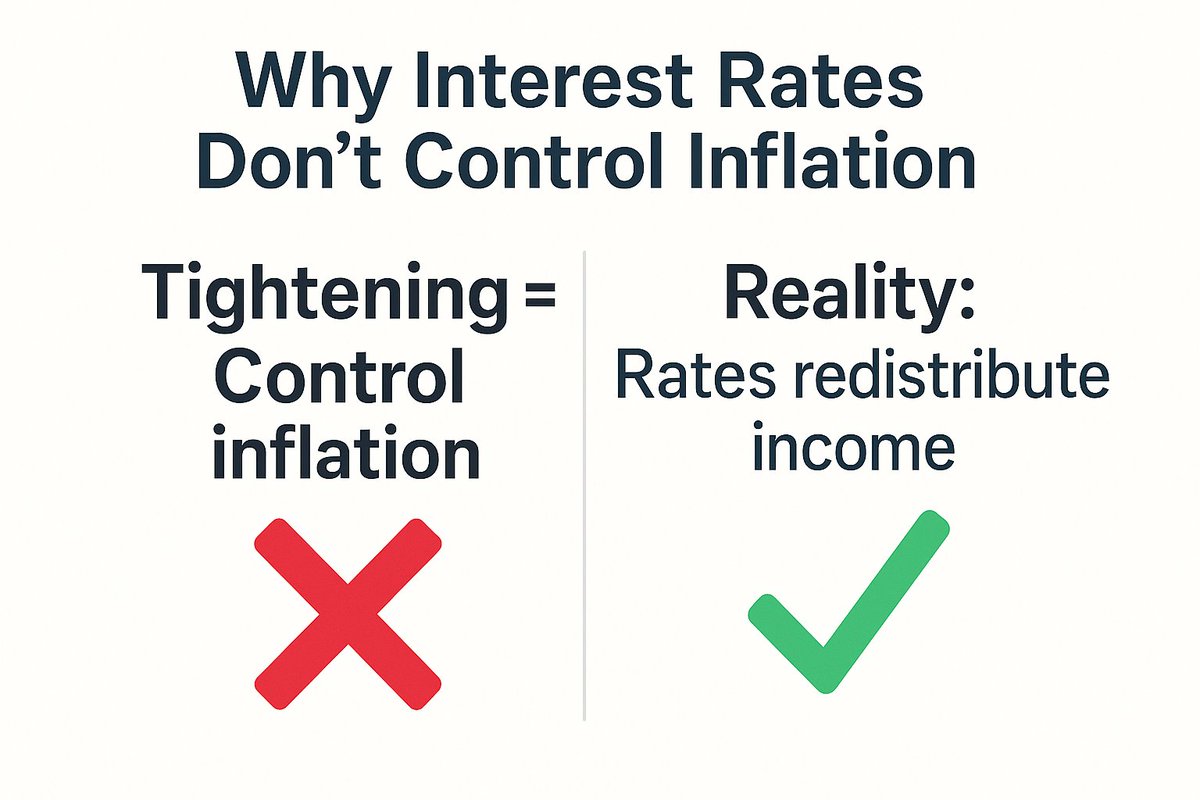

The fallacious story goes like this: banks take deposits, keep 10% as reserves, and lend out the rest. That fraction supposedly limits how much credit they can create. The textbook story: higher rates → less borrowing → lower demand → lower inflation.

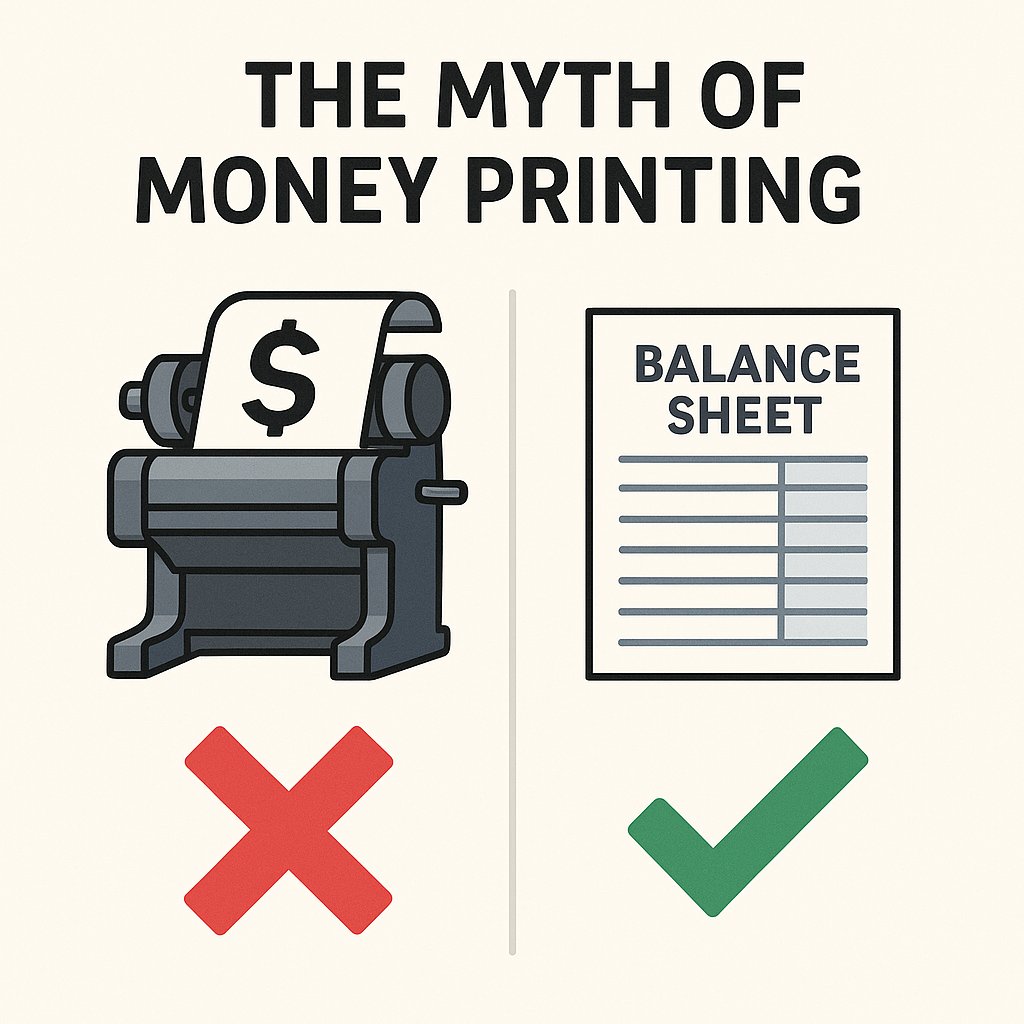

The textbook story: higher rates → less borrowing → lower demand → lower inflation. Story: gov't spends → prints money → inflation.

Story: gov't spends → prints money → inflation. The idea is simple: governments should not spend more than they tax.

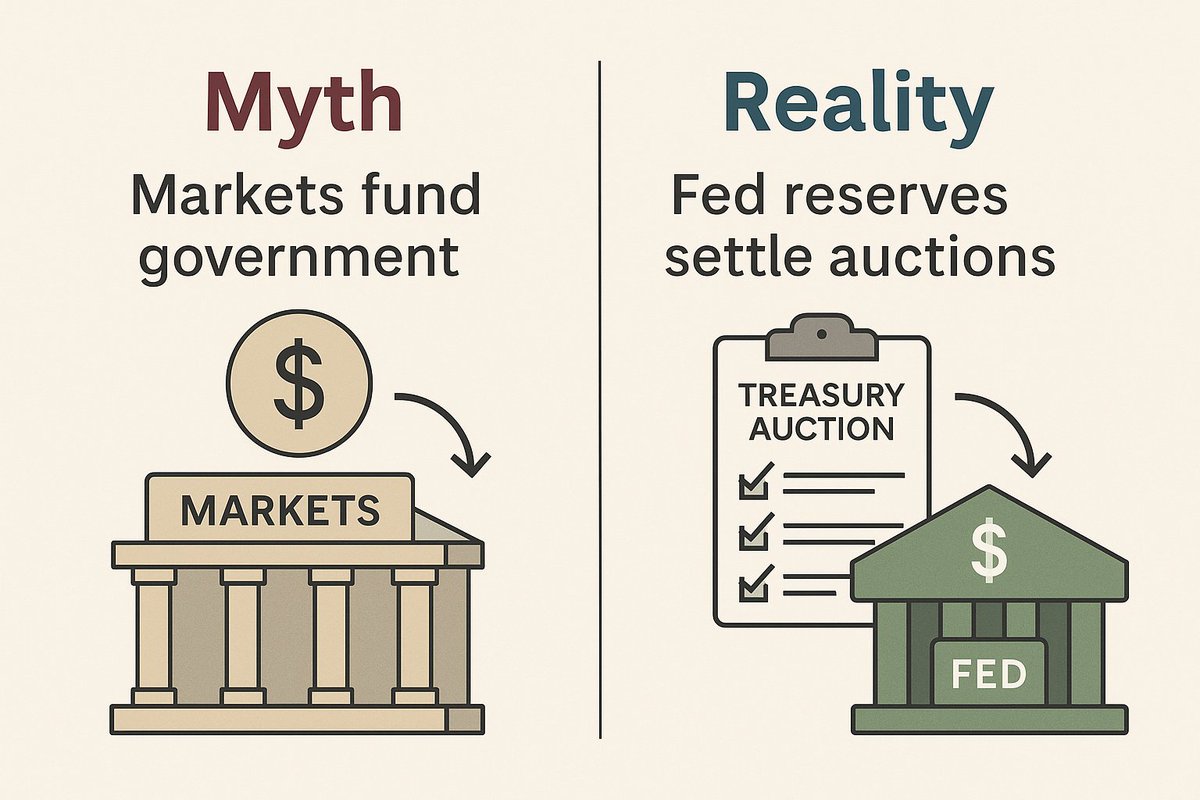

The idea is simple: governments should not spend more than they tax. Every week, the Treasury issues new securities at auction.

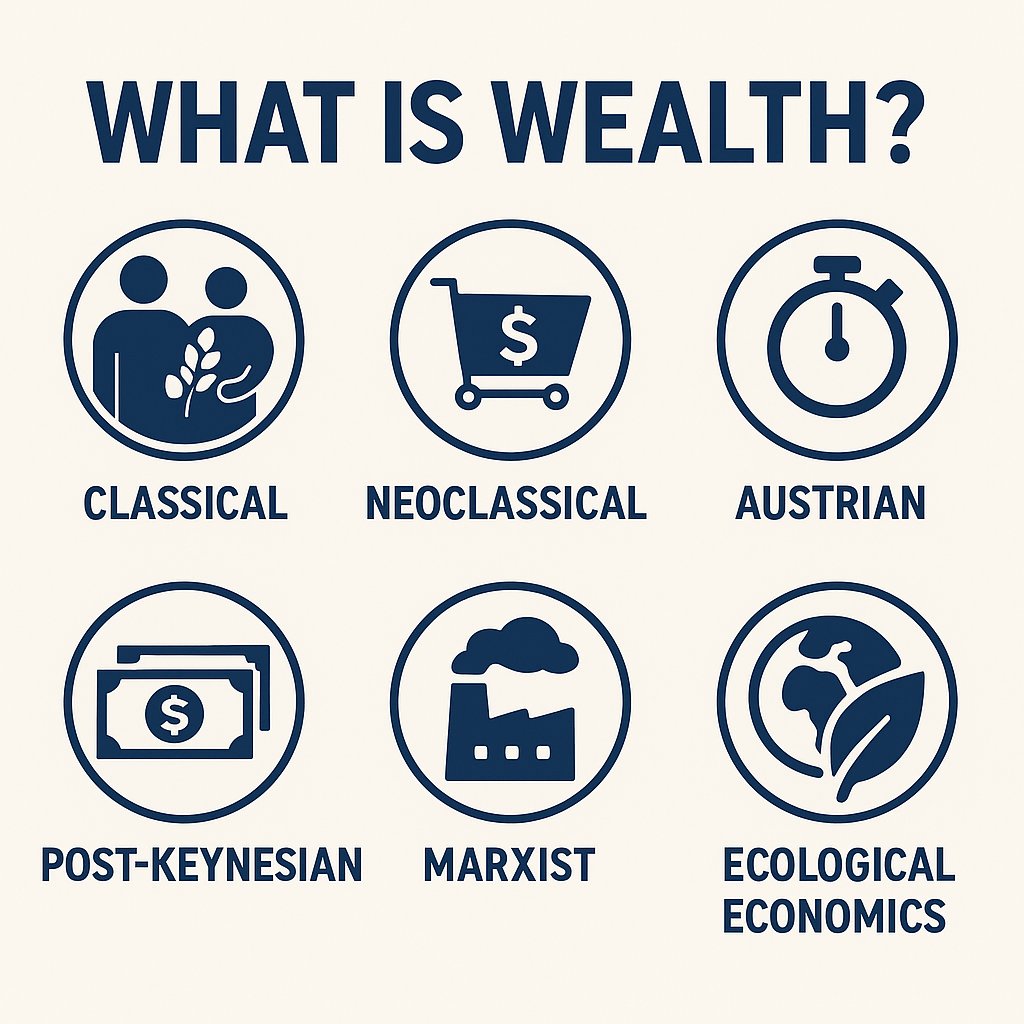

Every week, the Treasury issues new securities at auction. Classical economics (Smith, Ricardo):

Classical economics (Smith, Ricardo): The textbook story:

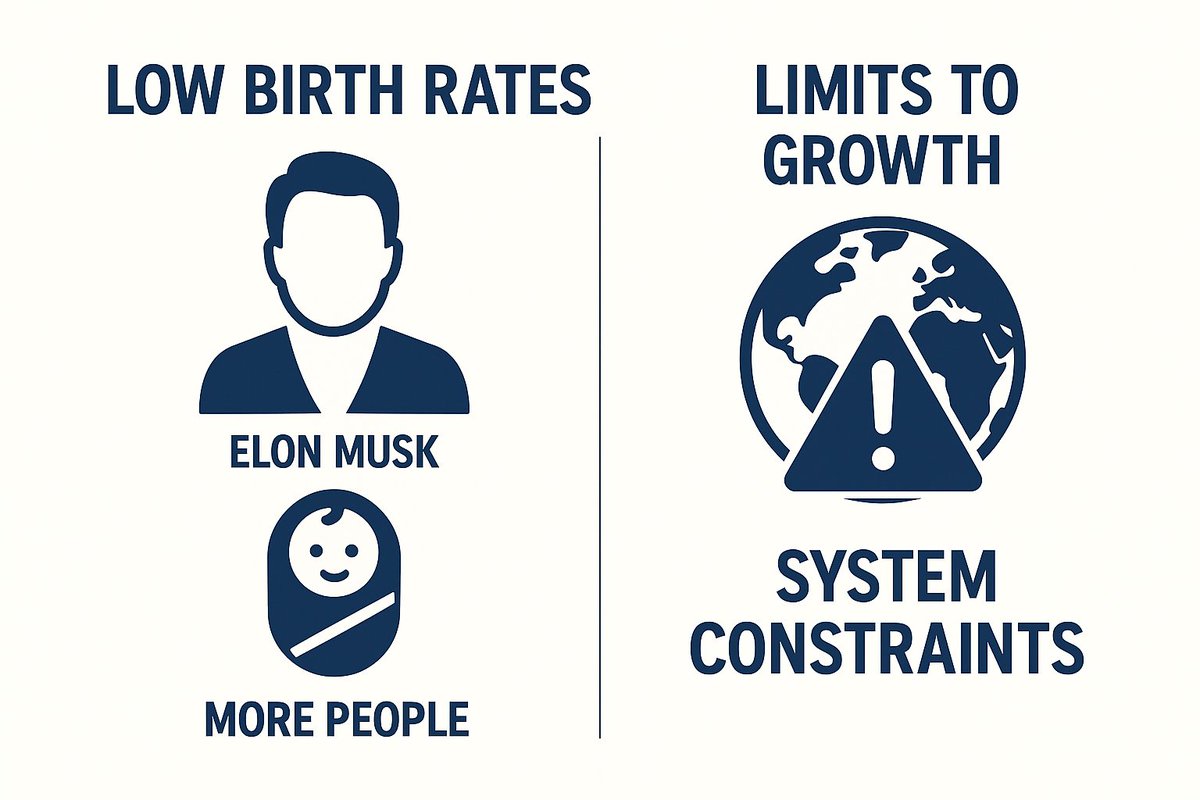

The textbook story: Musk’s story: if population falls, economies collapse.

Musk’s story: if population falls, economies collapse. Since 1978:

Since 1978:  No real-world industry looks like this.

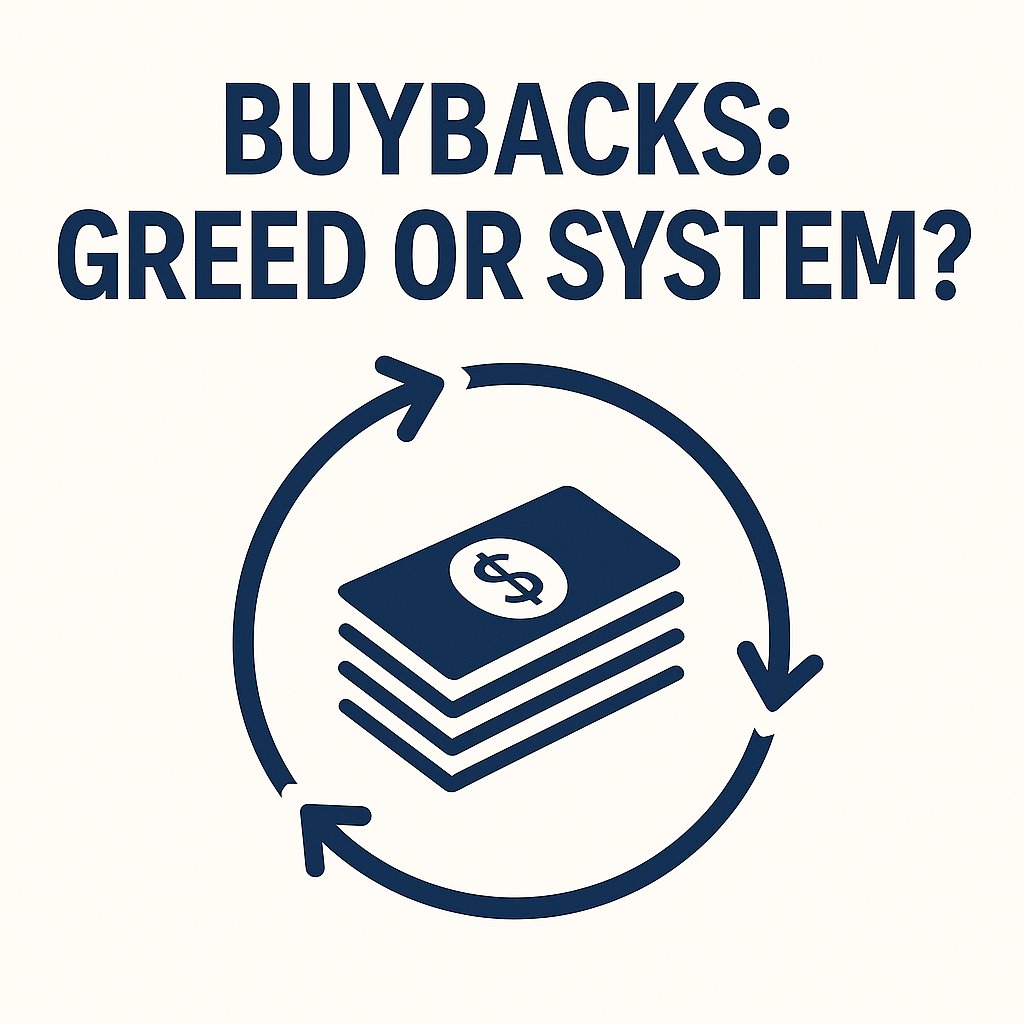

No real-world industry looks like this. Buybacks spark endless debate: are they corporate greed, or rational capital use?

Buybacks spark endless debate: are they corporate greed, or rational capital use? Wicksell’s idea: there exists some "natural" interest rate where saving = investment and inflation is stable.

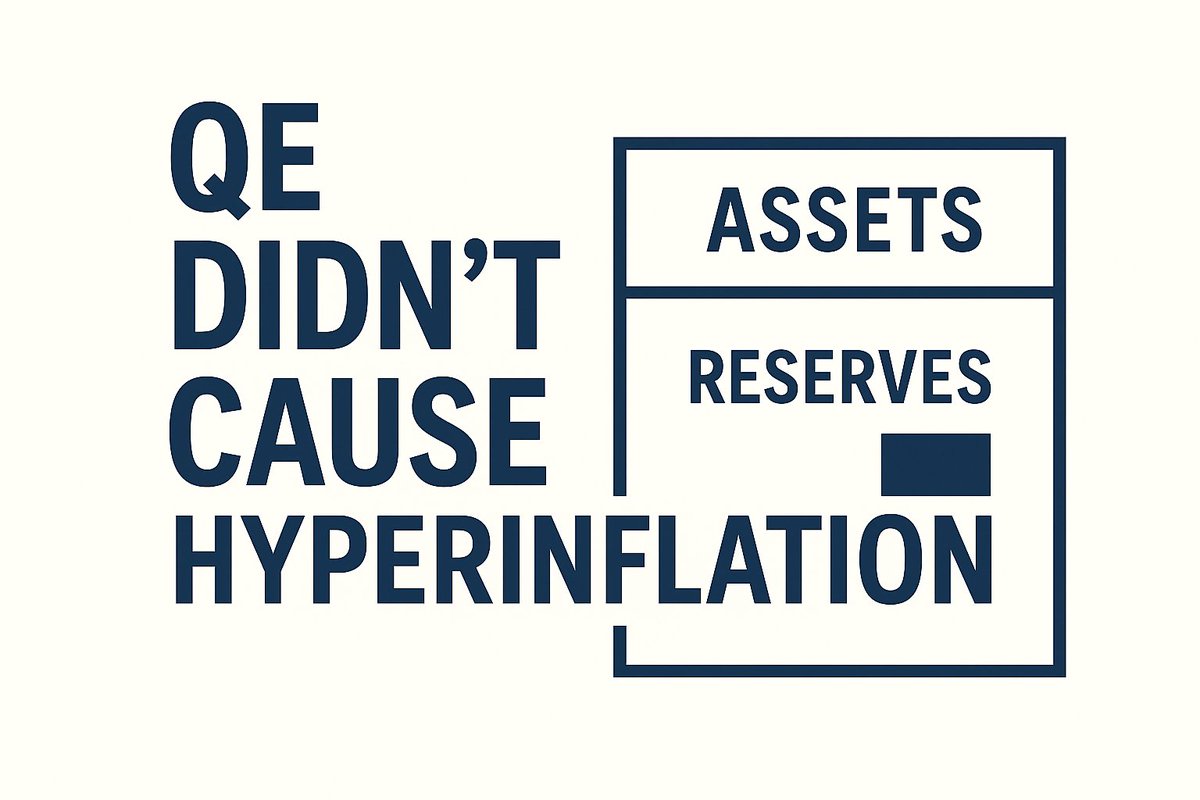

Wicksell’s idea: there exists some "natural" interest rate where saving = investment and inflation is stable. Because reserves don’t flow into the real economy.

Because reserves don’t flow into the real economy. The Goodwin growth cycle shows it:

The Goodwin growth cycle shows it: 1929, Japan’s 1990s bust, the 2008 GFC, all preceded by surging private debt-to-GDP.

1929, Japan’s 1990s bust, the 2008 GFC, all preceded by surging private debt-to-GDP. Traditionally, it meant banks held a fixed % of deposits in reserve (say 10%) and lent out the rest.

Traditionally, it meant banks held a fixed % of deposits in reserve (say 10%) and lent out the rest.