Invest intelligently in high-quality stocks! 15,000 subs on YT. I wrote three books. Learn more ⬇️

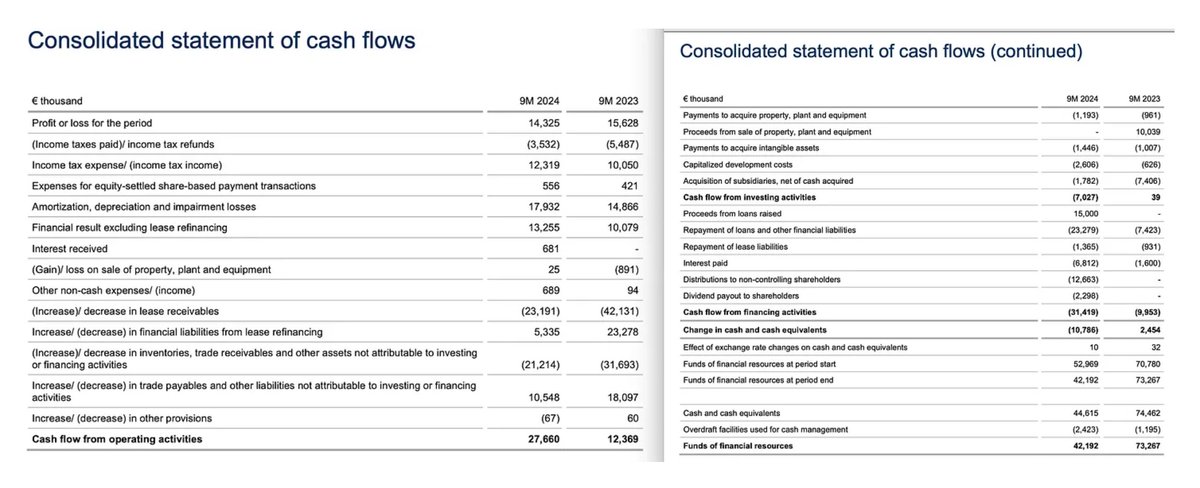

Evolution Gaming (EVO) released its Q1 results.

Evolution Gaming (EVO) released its Q1 results.

1. It starts with expectations.

1. It starts with expectations. 1/ The U.S. Stock Market’s Historical Edge

1/ The U.S. Stock Market’s Historical Edge 1/ Budget cuts & the myth of tariff-driven revenues

1/ Budget cuts & the myth of tariff-driven revenues 1/ The Market’s Hot Streak May Be Over

1/ The Market’s Hot Streak May Be Over

Lesson 1: Embrace the Macro as It Is

Lesson 1: Embrace the Macro as It Is

#1 The Italian Sea Group 3.47% $TISG 3.5%

#1 The Italian Sea Group 3.47% $TISG 3.5%

Signal 1: Concentration in the Mag-7

Signal 1: Concentration in the Mag-7

But of course, the attractiveness of Celsius as an investment lies not only in its current FCF yield but also in its potential for growth; growth in FCF on a per share basis.

But of course, the attractiveness of Celsius as an investment lies not only in its current FCF yield but also in its potential for growth; growth in FCF on a per share basis. Chapter 1: Stock Performance

Chapter 1: Stock Performance

1. Worldly Wisdom and Multiple Mental Models:

1. Worldly Wisdom and Multiple Mental Models:

1) Ulta’s Business Model

1) Ulta’s Business Model

Are the "Magnificent 7" is turning into the "Magnificent 1"?

Are the "Magnificent 7" is turning into the "Magnificent 1"?

I think being able to identify the key value drivers for each investment and being able to capture your investment thesis in a VERY concise way is a superpower in the world of investing.

I think being able to identify the key value drivers for each investment and being able to capture your investment thesis in a VERY concise way is a superpower in the world of investing.

MYTH #1 – The PE Should Be Your Go-ToValuation Metric

MYTH #1 – The PE Should Be Your Go-ToValuation Metric

Category 1 – Moat:

Category 1 – Moat: #1 – Talks at Google (2014)

#1 – Talks at Google (2014)

So why even consider investing in Endor?

So why even consider investing in Endor?

#1: Russel 2000 vs. S&P 500 total return performance at the lowest level since 2000!

#1: Russel 2000 vs. S&P 500 total return performance at the lowest level since 2000!