SOIC Intelligent Research LLP | SEBI Registered Research Analyst (Reg. No: INH000012582) | Views are personal & for education purposes | Not Investment Advice

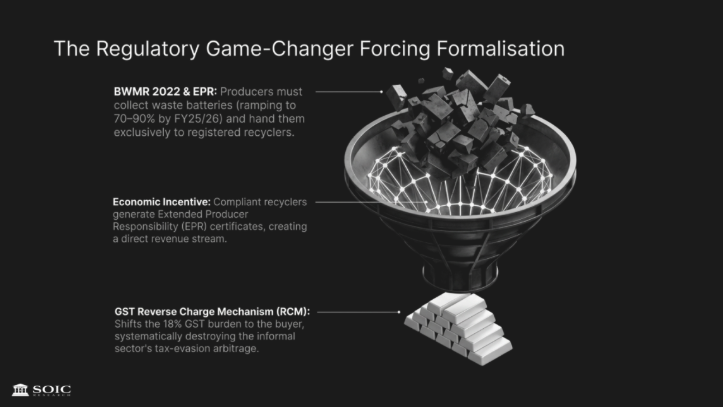

India's recycling rate is approximately 20%. In developed markets in the US, Germany, Japan it sits between 60% and 80%. That gap alone tells you there is a massive structural opportunity somewhere. But the more interesting number is this: roughly 60% of India's lead scrap still flows through the informal sector backyard smelters and kabadiwalas who operate with 50–70% recovery rates, zero environmental compliance, and a single competitive advantage: they don't pay the 18% GST.

India's recycling rate is approximately 20%. In developed markets in the US, Germany, Japan it sits between 60% and 80%. That gap alone tells you there is a massive structural opportunity somewhere. But the more interesting number is this: roughly 60% of India's lead scrap still flows through the informal sector backyard smelters and kabadiwalas who operate with 50–70% recovery rates, zero environmental compliance, and a single competitive advantage: they don't pay the 18% GST.

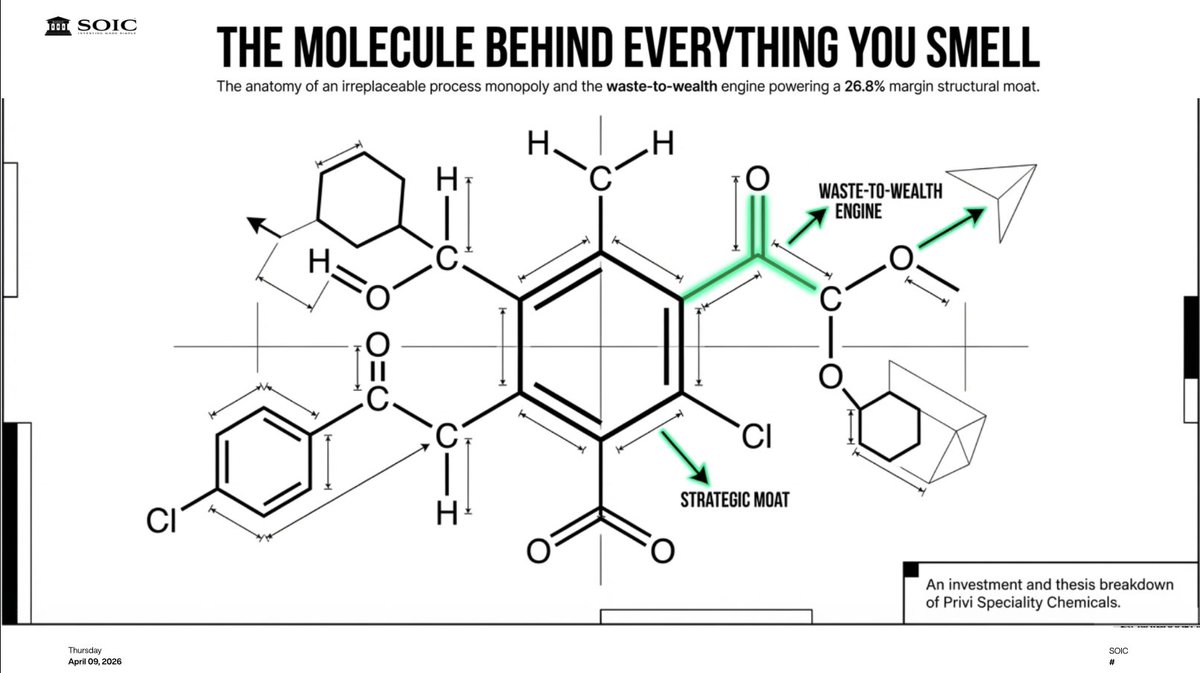

This company makes the molecule responsible for the freshness in 99% of the perfumes sold in the world today. It is one of just four companies on the planet that has mastered the chemistry of extracting sulphur from a foul-smelling hazardous paper mill by-product and turning it into the building block of a $3.8 billion global aroma chemicals market.

This company makes the molecule responsible for the freshness in 99% of the perfumes sold in the world today. It is one of just four companies on the planet that has mastered the chemistry of extracting sulphur from a foul-smelling hazardous paper mill by-product and turning it into the building block of a $3.8 billion global aroma chemicals market.

Let's first start from all the products that company is into and understand the key moat that the company has in each of the products the company is in

Let's first start from all the products that company is into and understand the key moat that the company has in each of the products the company is in