📈 | Automated Trading Systems @ https://t.co/GP053tHNIR

💻 | ProRealCode Market @ https://t.co/CXAyE7nAec

🔌 | Compatible with IG & Interactive Brokers

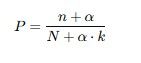

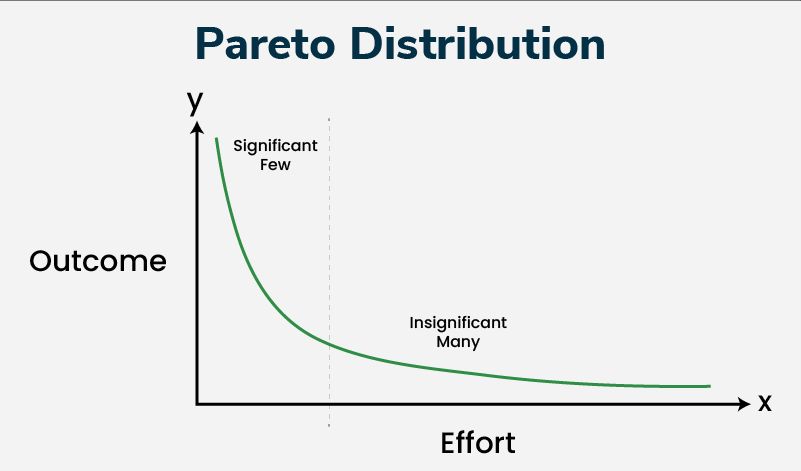

The Pareto distribution is a power-law probability distribution:

The Pareto distribution is a power-law probability distribution:

What is collinearity?

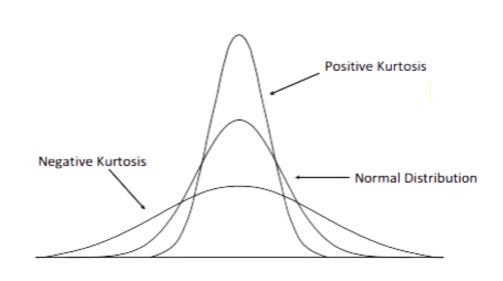

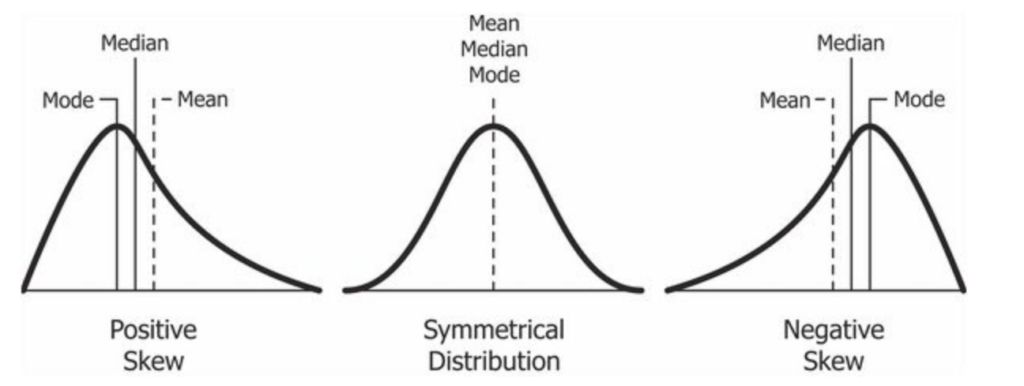

What is collinearity? Skewness measures the asymmetry of a return or drawdown distribution.

Skewness measures the asymmetry of a return or drawdown distribution.

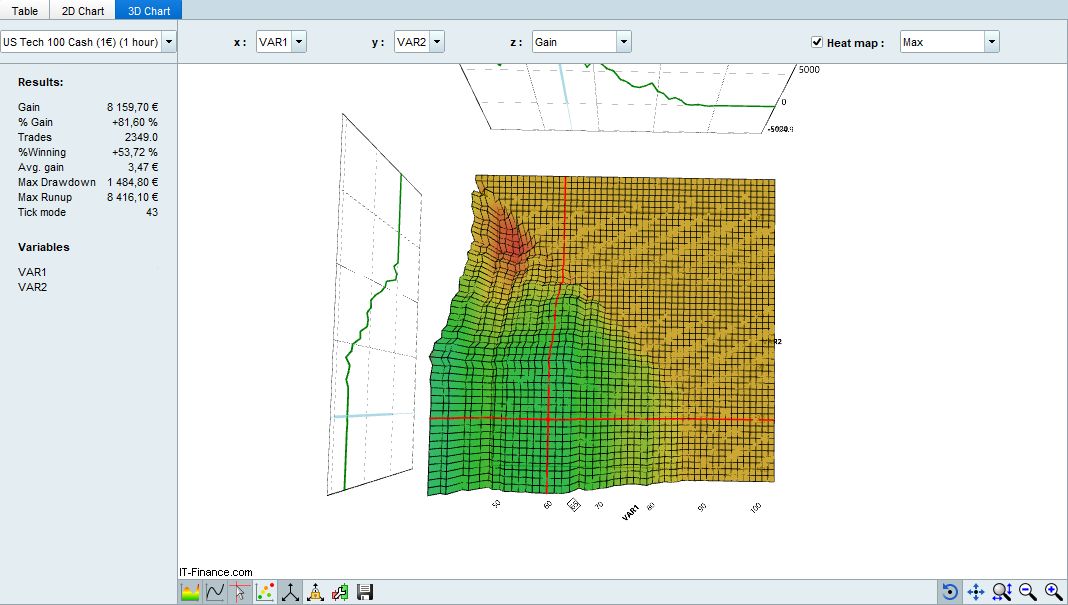

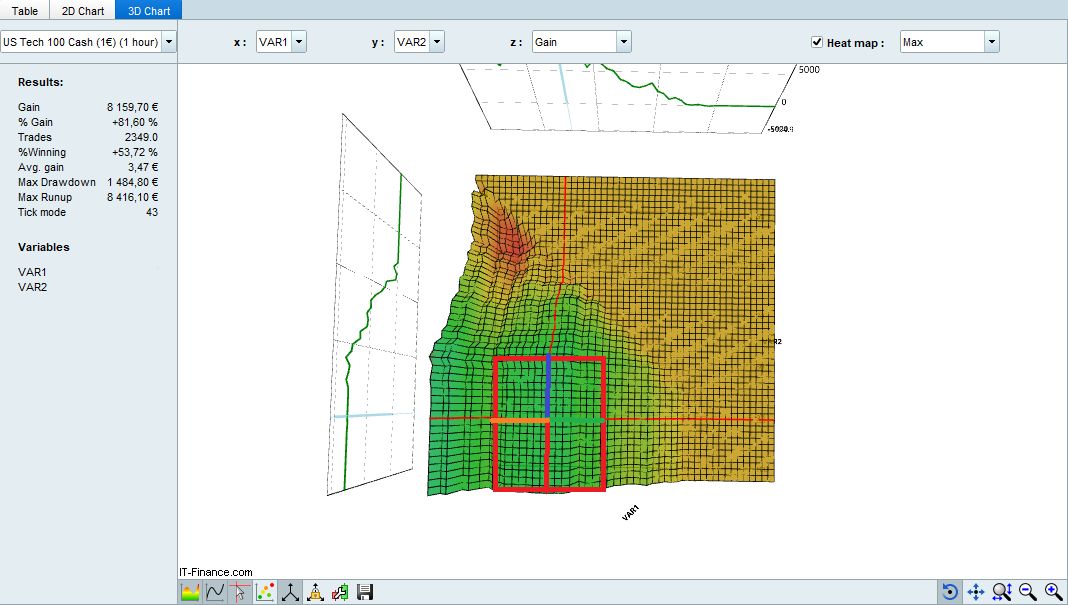

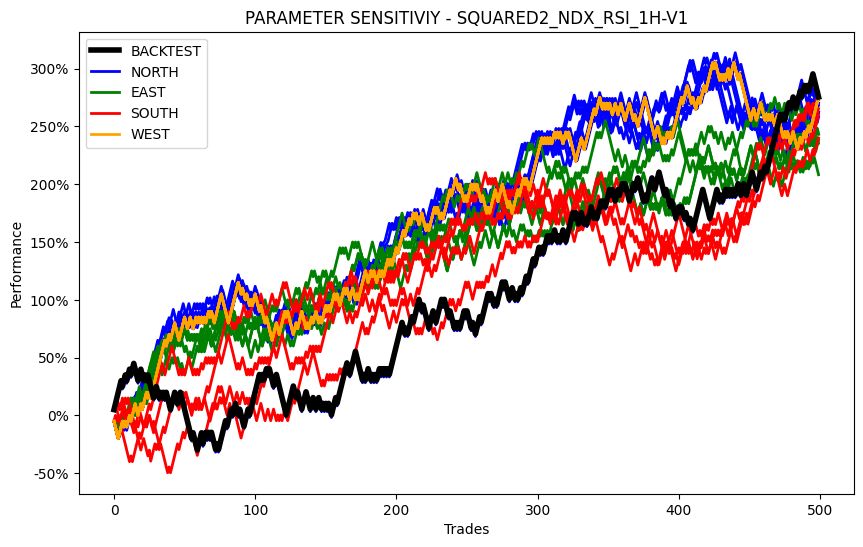

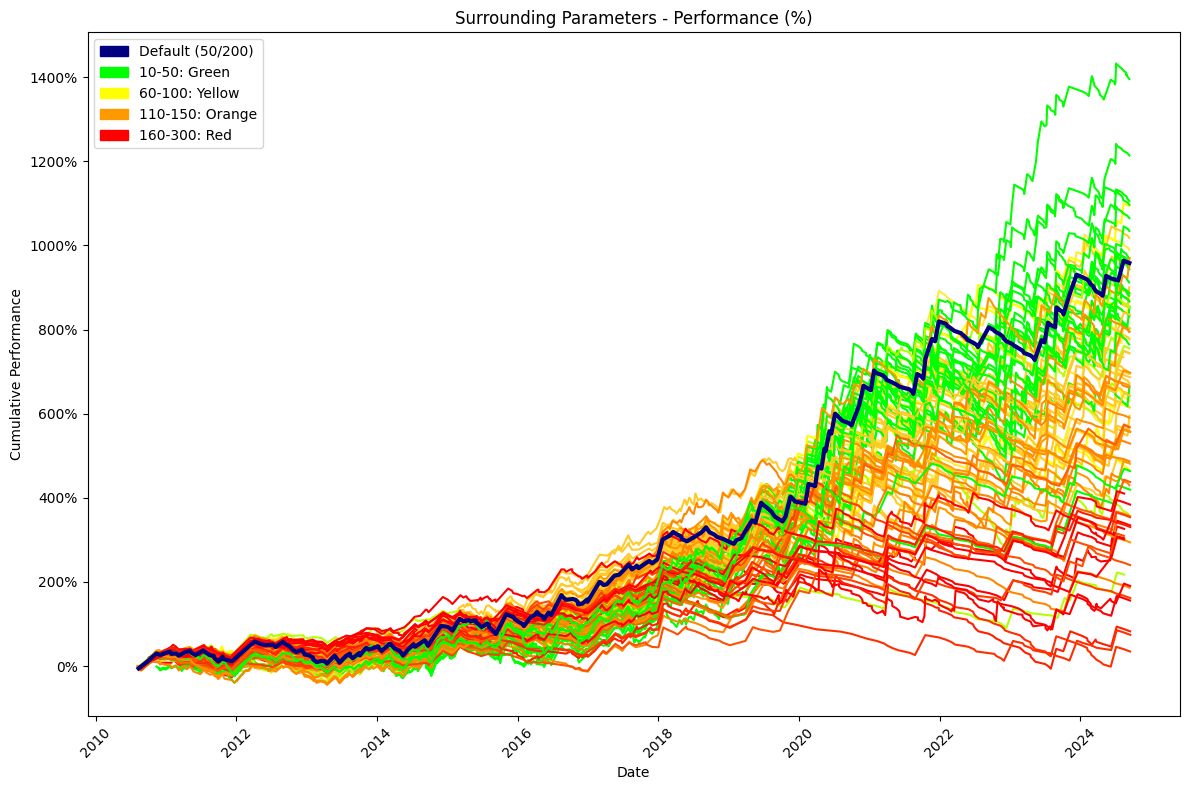

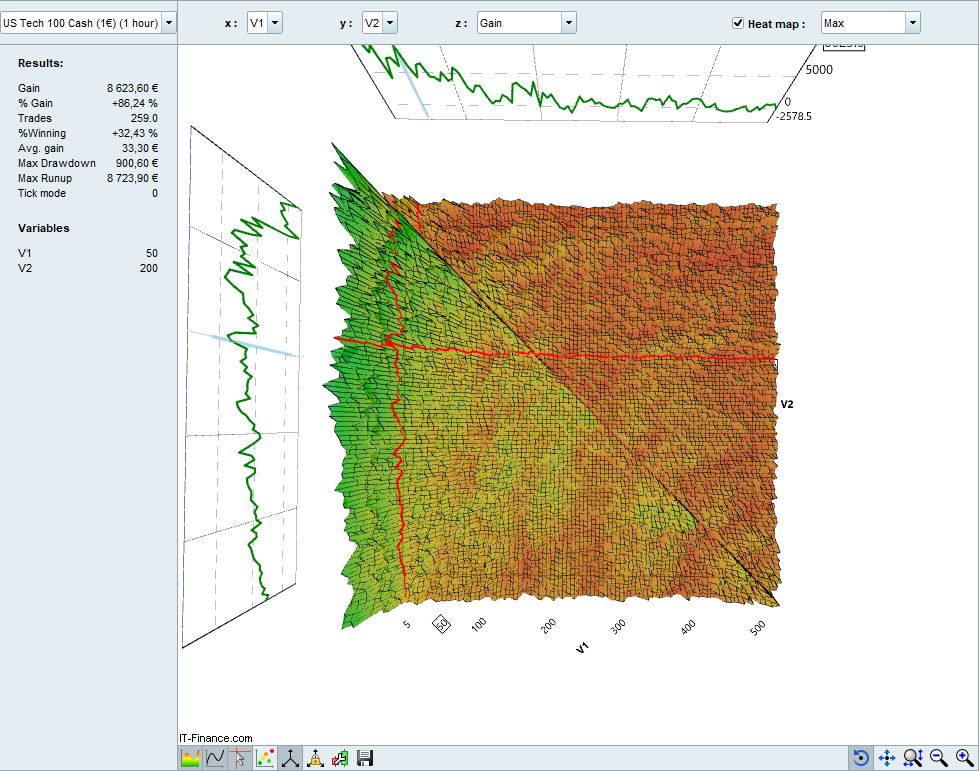

In algorithmic trading, every strategy has parameters that guide how it makes decisions. BUY when MA50 crosses over MA200 for example.

In algorithmic trading, every strategy has parameters that guide how it makes decisions. BUY when MA50 crosses over MA200 for example. @snalanningen More than likely, you've come across the topography of the parameter space.

@snalanningen More than likely, you've come across the topography of the parameter space.

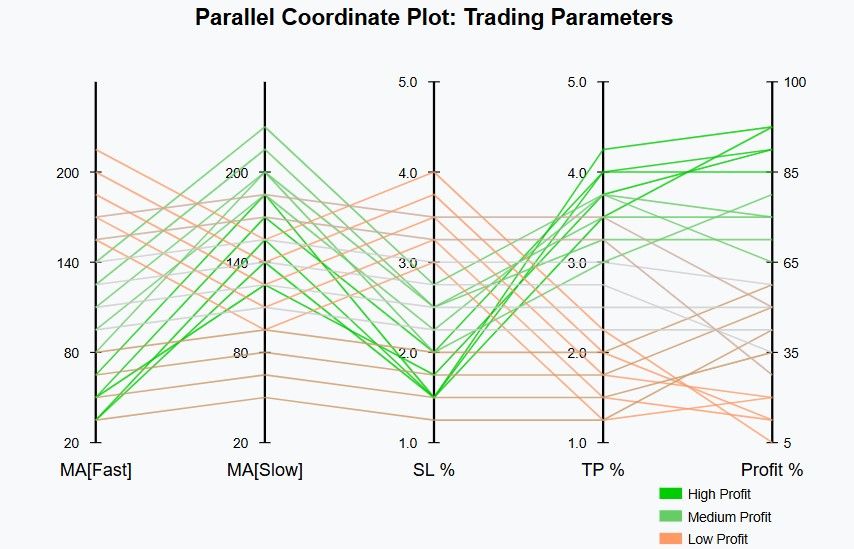

A week ago we took our Larry Connors 2RSI system that we developed using ChatGPT and ran it through the "Up & Down" test.

A week ago we took our Larry Connors 2RSI system that we developed using ChatGPT and ran it through the "Up & Down" test.