Foxhole Investor🧘🏽♂️, Chain Reader📚, Fitness Focused💪

Disciple of Discipline.

All views are personal.

Book 2

Book 2

MOVE is widely used as a benchmark for measuring the level of risk in the US Treasury market. Higher MOVE readings generally indicate higher levels of market uncertainty or volatility, while lower readings indicate lower levels of market volatility.

MOVE is widely used as a benchmark for measuring the level of risk in the US Treasury market. Higher MOVE readings generally indicate higher levels of market uncertainty or volatility, while lower readings indicate lower levels of market volatility.

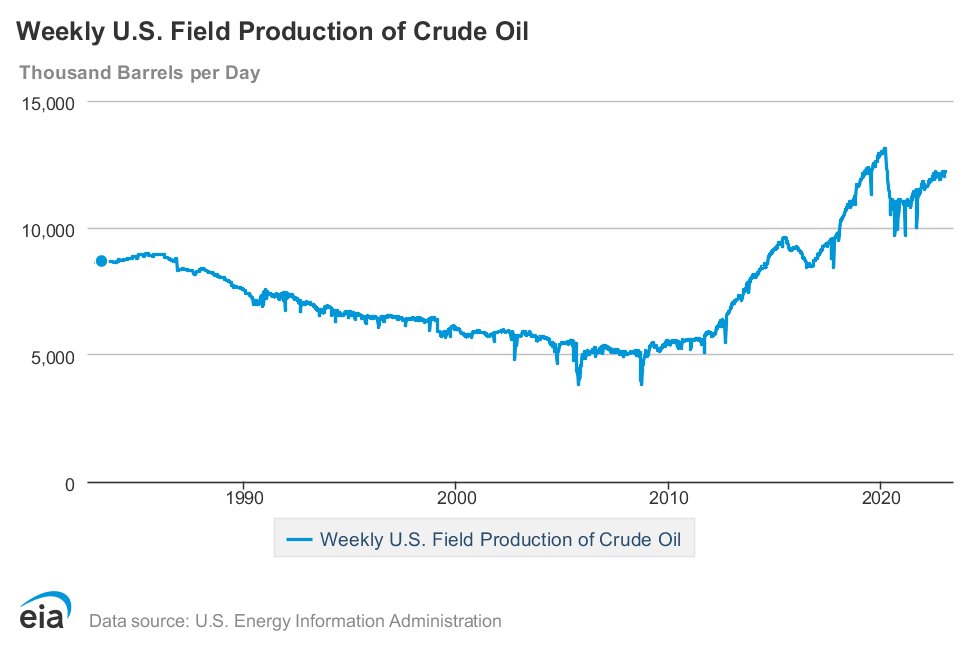

US Oil production also now at post COVID peak of 12.2mbpd. Sitll 900,00 bpd below the peak achieved in March 2020.

US Oil production also now at post COVID peak of 12.2mbpd. Sitll 900,00 bpd below the peak achieved in March 2020.

What Are We Saying?

What Are We Saying?