Founder, ValueQuest Capital LLP | Professor @FLAMEUniversity | Personal views, not advice. SEBI disclosures ↓ https://t.co/uWiFy4ffEp

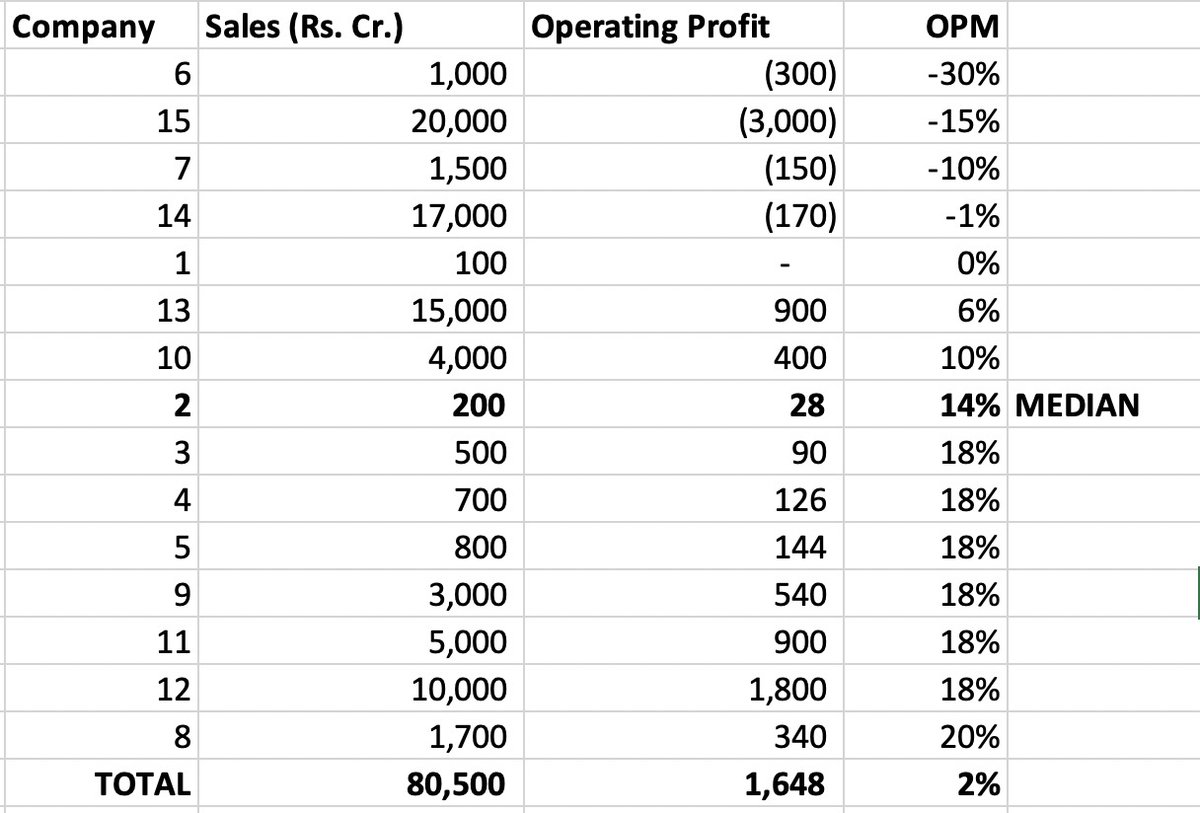

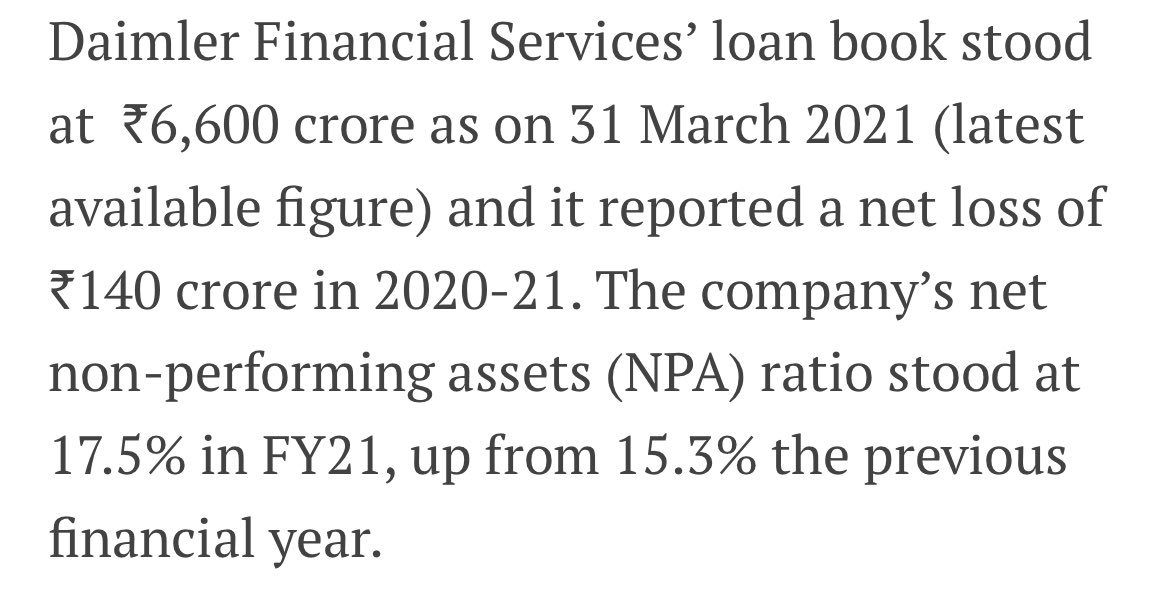

There are many ways in which the finance company can make the auto company’s P&L and balance sheet look pristine. One way is that all the loans (including bad ones) given to customers for creating the demand reside on the finance company’s balance sheet.

There are many ways in which the finance company can make the auto company’s P&L and balance sheet look pristine. One way is that all the loans (including bad ones) given to customers for creating the demand reside on the finance company’s balance sheet.

Zoom and Doom (for those who bought at or near peak)?

Zoom and Doom (for those who bought at or near peak)?

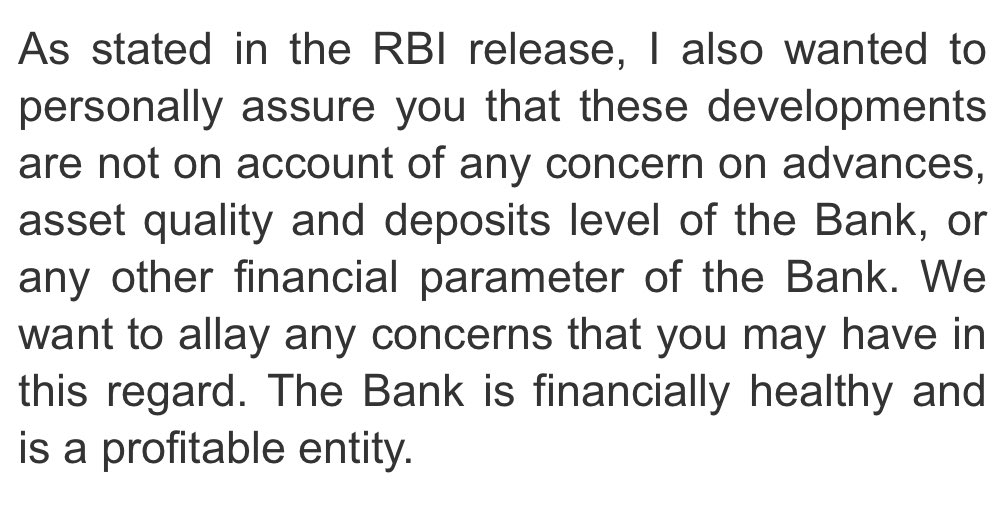

Now ask: Why was the existing CEO asked by RBI to proceed on leave and why did it appoint Mr. Yogesh Dayal as an Additional Director on the Board of the Bank?

Now ask: Why was the existing CEO asked by RBI to proceed on leave and why did it appoint Mr. Yogesh Dayal as an Additional Director on the Board of the Bank?

Whenever shortages appear, the typical manager simply can’t wait to expand capacity and thereby plug the hole through which money is showering upon him." - Buffett

Whenever shortages appear, the typical manager simply can’t wait to expand capacity and thereby plug the hole through which money is showering upon him." - Buffett