DELTA tells us how much the car will move if we give it a little push.

Jan 29, 2023 • 5 tweets • 3 min read

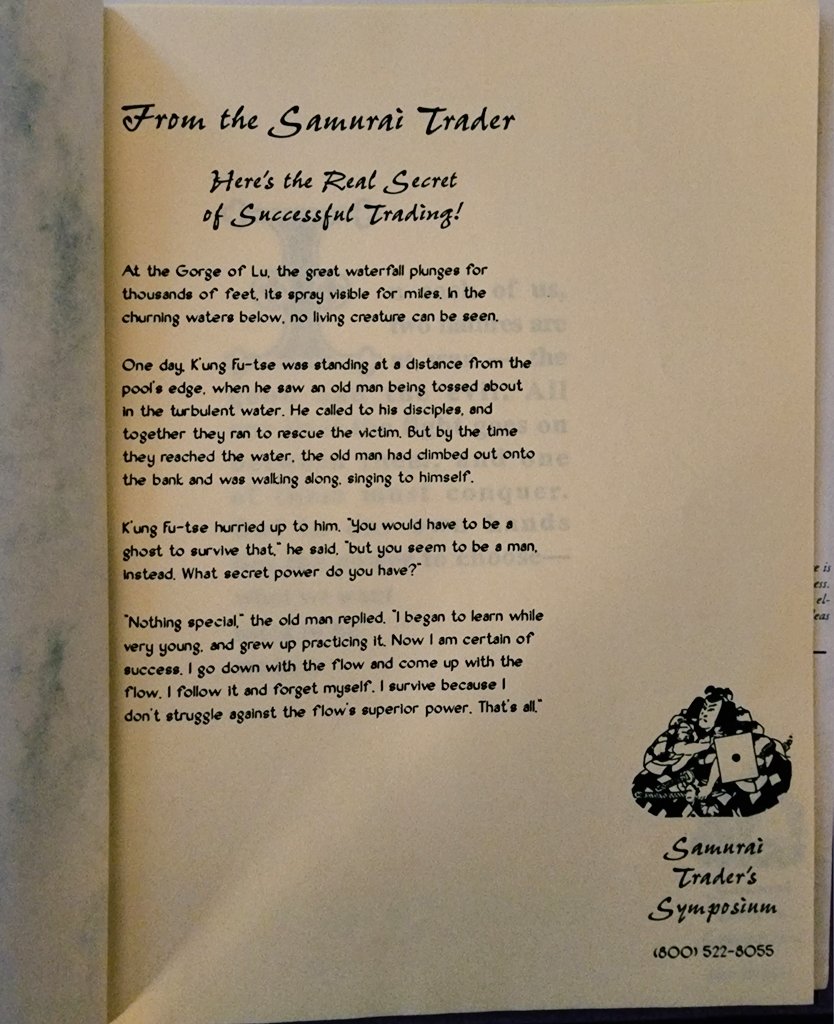

Found something old but gold.

In 1997 my family travelled to Chicago to attend a trader's conference.

"Samurai Trader's Symposium".

It was hosted by the author of the book "Zen in the Markets: Confessions of a Samurai Trader" by the late Edward Allen Toppel.

The book is mostly about Trading Psychology, which had a big impact on my dad's trading when he first started out. The Author, Eddie as we called him, was a top trader on the Chicago exchange at the time. He became a close friend to our family.

Jan 7, 2023 • 17 tweets • 4 min read

Hello! This is a master thread that contains my past threads on options, trading psychology and my own experiences in the market. I hope they provide you with valuable and practical insights.

10 mistakes in my 14 years of trading as an option seller

How to become a successful trader

(for beginners) 🧵

1. We need adequate funds to begin our trading journey. If you don't have enough funds, my suggestion would be to borrow money from relatives or close friends. In the long run you will realise that your relationship will only grow stronger.

Oct 15, 2022 • 12 tweets • 2 min read

10 things that have helped me stay profitable as a full-time trader for nearly two decades 🧵

1) Following the market. Market speaks to us in one language: Price. Be it volatility or direction, the ideology has always been simple: to follow the price as closely as possible. Whenever I have astrayed from the objectivity of price, have been severely punished by the market.

Jul 15, 2022 • 13 tweets • 2 min read

Trading during Low Vix 🧵

The most tough environment for option sellers is the transition between high to low Vix. One gets well accustomed in handling the regular IV spikes & the high theta decay that follows afterwards.

Jun 4, 2022 • 19 tweets • 3 min read

Why Theta decay alone is not a real edge for option sellers 🧵

If there is one certainty in the markets, it's that all OTM options will expire zero. Human beings crave certainty & if it's mixed with a hope of financial gain, then they will leap towards it in the first go.

Apr 8, 2022 • 4 tweets • 1 min read

If you compare trading with other profession/startups, there's negligible starting cost, with all the freedom in the world of both time & no restriction of location.

So there has to be some catch to it, as it looks too good to be true.

Even after getting this good of a deal,

new entrants will argue about why they can't start making consistent money on the onset, without first learning the process which takes few years atleast.

Being such a low cost business model, all trading requires is consistent hustle, humility & eagerness to learn everyday.

Mar 19, 2022 • 12 tweets • 2 min read

10 mistakes in my 14 years of trading as an option seller 🧵

1. Staying neutral all the time. Majority of the years i have been a neutral option seller. I now realise that having a little sense of direction would have given me an added advantage with better utilisation of capital & also leverage (till the time it was available).

Feb 22, 2022 • 5 tweets • 1 min read

HIGH VOLATILITY SCENARIOS

Volatility can rise in different ways. Below are few scenarios which i remain mindful of during market.

1) Small delta move, rise in IV

This is not usually a dangerous scenario because you have received more premiums, though MTM is momentarily -ve.

+

2) High delta move, rise in IV

Major damage happens in such scenario in non-directional & the loss also becomes irrecoverable. Usually this scenario happens in a persistent low realisation environment where adjustment cost is high.

Good opportunities come after this move.

+

Nov 28, 2021 • 6 tweets • 1 min read

CHRONOLOGY of most used option strategies by me over the years:

2009: Strangle, Long Strangle

Initially had the belief that can play volatility both sides

2010: Strangle, Straddle

Used to convert positional strangles to straddles near expiries

2011: Calendar Spreads, Straddle

2012: Calendar Spreads, Straddle

Nifty current & next month were the only liquid options for Calendar

2013: Calendar Spreads, Butterfly, Straddle

2014: Diagonal Spreads, Ironfly

2015: Diagonal Spreads, Ratios, Straddle

(Started learning greeks mainly how to maintain delta)

Nov 13, 2021 • 6 tweets • 2 min read

Option traders find a strategy & backtest it for 10+ years to see how it performed through various combinations of entry, exits, SLs.

One has to understand that market regimes keep changing after 3-4 years.

What worked in 2017 doesn't work with same effectiveness in 2021.

1/

Looking back i was a completely different trader in 2008 to 2015 to now. Ofcourse one keeps improving his skills but it also happens because markets keep evolving.

Whatever strategy works for a particular time period loses it's edge as more people start pouring into it.

2/

Oct 30, 2021 • 7 tweets • 2 min read

Nifty or Banknifty for option selling? 🧵

There are times when i have traded exclusively in bnf for atleast a couple of yrs, when the weeklies got introduced.

Stopped trading in it for an yr when nf weekly got introduced & bnf started having price freeze issues on expiry days.

Idea has always been to master just one index.

Before the introduction of bnf weeklies, there was no other choice than nf monthly options. Bnf monthly didn't have good liquidity as compared to nf at that time.

Even next month nf options had better liquidity than bnf options.

Aug 7, 2021 • 10 tweets • 2 min read

SURVIVORSHIP BIAS

Survivorship bias is the tendency to analyze the strategies that performed exceptionally well and ignore all those that didn’t reach our criteria. We have an inclination towards focusing on the survivors, even if they survived out of luck rather than viability.

So basically we are testing our ideas on an incomplete data. The missing data may conceal losing trades or winning trades, causing us to deploy a strategy which we shouldn't or vice versa. Backtest results with this bias will not represent the true picture.

Jul 17, 2021 • 10 tweets • 2 min read

FIRST ACCOUNT OF OPTIONS

We have this perception that Options are relatively new trading instruments, but they actually go back to the times before Christ was born. Getting to know the origins of this fascinating trading instrument can help us appreciate the depth of it.

1/

The very first account of options was mentioned in Aristotle's book named "Politics", published in 332 B.C. That's how far back humans have used the concept of buying the rights to an asset without necessarily buying the asset itself.

2/

Jun 18, 2021 • 16 tweets • 3 min read

A THREAD

Topic: HOW TO TRADE IN RISING PREMIUMS SCENARIO

Option sellers specially Straddle sellers feel that rising premiums give them excellent opportunity to make easy money. So what they are seeing is the theta aspect of options & ignoring the delta/gamma/vega forces.

1/

With rising premiums come high delta moves. There is a reason why premiums are all increasing up in the first place. High uncertainty & fear is what's controlling the markets during such times. So a volatile 200 point move in nifty is always on the cards.

2/

Jun 4, 2021 • 7 tweets • 2 min read

Understanding HIGH & LOW VIX

VIX at 16: If you check today's IV behaviour, they were not spiking much even with decent delta move in BNF. The movement was subtle, giving some time to adjust. So someone having good adjustment mechanism can stay in the game longer.

1/

VIX at 20: The same delta move will be more fierce, coupled with rise in premiums. When premiums rise with movement, then the adjustment cost increases exponentially. The premiums can fall back at EOD, but the damage is done if caught in the spike.

2/

May 29, 2021 • 5 tweets • 1 min read

CHRONOLOGY OF SUCCESSFUL TRADING

• Learn basics of trading but no breakthrough for many months

• Find a good strategy or trading idea

• Implement that idea with some capital

• Start adding more capital because of good returns

• Start making decent returns for few months

1/

• Lose all previous month returns in a week

• Hault trading for some days

• Go back to the drawing board & improve the strategy

• Start again with 2nd step

• Repeat for n number of cycles (n depends solely on a trader's skill & huslte)

• Create a decent trading career.

2/

May 23, 2021 • 8 tweets • 2 min read

Indeed Pathik bhai, it's the most dangerous scenario for any kind of option writer. The way i handle it is by converting a straddle/strangle into ratio spreads which i have explained in the past in the below tweets. Usually it's only one side where premiums are spiking. +

So we need to stay away from that side & convert our position to the opposite side in ratios.

Many go the 920 straddle way, that is exiting the losing leg & running the profit one. The only problem with that is that by doing that they have exited the non-directional realm +

May 23, 2021 • 8 tweets • 4 min read

@Pathik_Trader Indeed Pathik bhai, it's the most dangerous scenario for any kind of option writer. The way i handle it is by converting a straddle/strangle into ratio spreads which i have explained in the past in the below tweets. Usually it's only one side where premiums are spiking. +

@Pathik_Trader So we need to stay away from that side & convert our position to the opposite side in ratios.

Many go the 920 straddle way, that is exiting the losing leg & running the profit one. The only problem with that is that by doing that they have exited the non-directional realm +

May 22, 2021 • 11 tweets • 2 min read

PSYCHOLOGICAL EFFECTS OF POSTING MTM SCREENSHOTS

We all see traders posting their profits regularly on twitter. This post is not about how geniune they are or not. Let's not get into it. It's about how posting regular profits affects the psychology of the trader posting it.

1/

After posting series of screenshots & receiving all the acknowledgement from the followers, the ego gets a nice boost. This feeling is even more overwhelming than the actual satisfaction of the profit earned. That is the extra dopamine which we receive from the praise.

2/

The book is mostly about Trading Psychology, which had a big impact on my dad's trading when he first started out. The Author, Eddie as we called him, was a top trader on the Chicago exchange at the time. He became a close friend to our family.

The book is mostly about Trading Psychology, which had a big impact on my dad's trading when he first started out. The Author, Eddie as we called him, was a top trader on the Chicago exchange at the time. He became a close friend to our family.