And if you restrict that to banks that were actually large enough to be investable 10 years ago... it's a pretty short list.

And if you restrict that to banks that were actually large enough to be investable 10 years ago... it's a pretty short list.

The ultimate product is very good! Yes, they are levered and the fees are high... but the net outcome is great.

The ultimate product is very good! Yes, they are levered and the fees are high... but the net outcome is great.

1) Bravo Bundle - takeout candidates. Despite the group name, some (e.g. TWLO, OKTA) would almost have to go to strategic buyers.

1) Bravo Bundle - takeout candidates. Despite the group name, some (e.g. TWLO, OKTA) would almost have to go to strategic buyers.

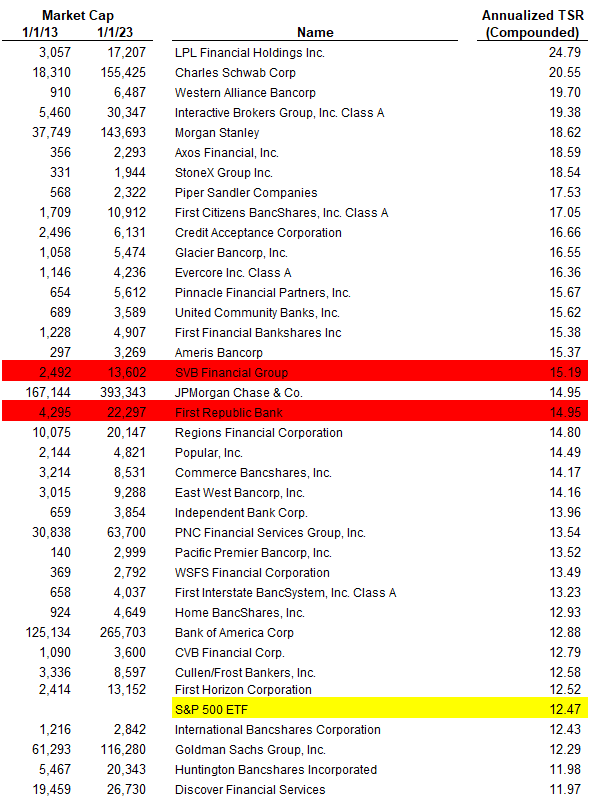

Can't really see it in the prior Chart due to the Y-axis:

Can't really see it in the prior Chart due to the Y-axis: