One particular data point has proven to be very useful through time—and it's fun because it's illustrative of the underlying reality.

One particular data point has proven to be very useful through time—and it's fun because it's illustrative of the underlying reality.

I see, I see.

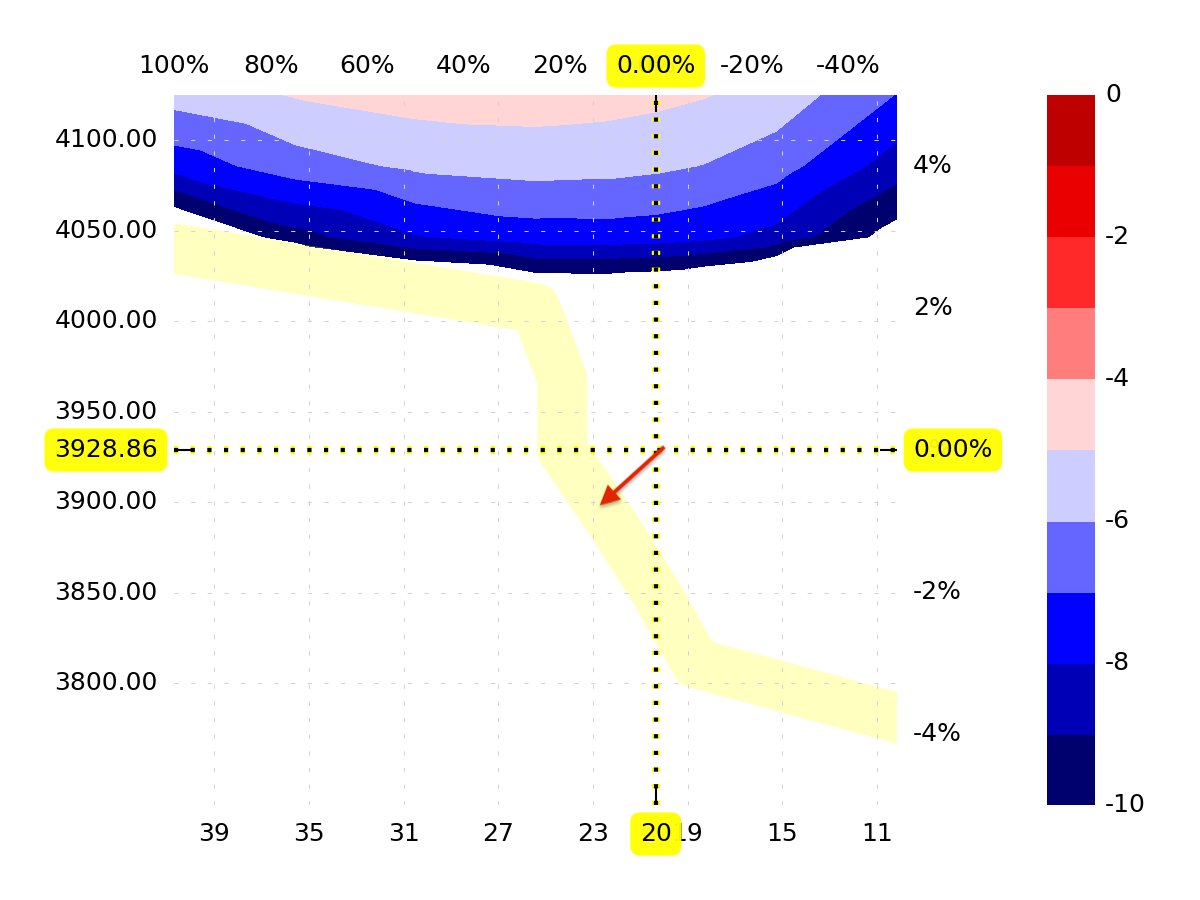

I see, I see. The CFTC CoT (TFF) data covering E-minis has been delayed for many weeks due to a "cyber incident," but when they finally release data from after January 24th, you'll likely note that Dealer Intermediaries have taken on a large short position in the intervening time.

The CFTC CoT (TFF) data covering E-minis has been delayed for many weeks due to a "cyber incident," but when they finally release data from after January 24th, you'll likely note that Dealer Intermediaries have taken on a large short position in the intervening time.

...you learn a lot about the way a stock trades that you wouldn't be able to learn by simply looking at a chart.

...you learn a lot about the way a stock trades that you wouldn't be able to learn by simply looking at a chart. And vice versa: Lower VIX relative to higher RV means better intraday performance for SPX.

And vice versa: Lower VIX relative to higher RV means better intraday performance for SPX.

Normally, this would be an opportunity for us to plug gamma exposure (GEX).

Normally, this would be an opportunity for us to plug gamma exposure (GEX).