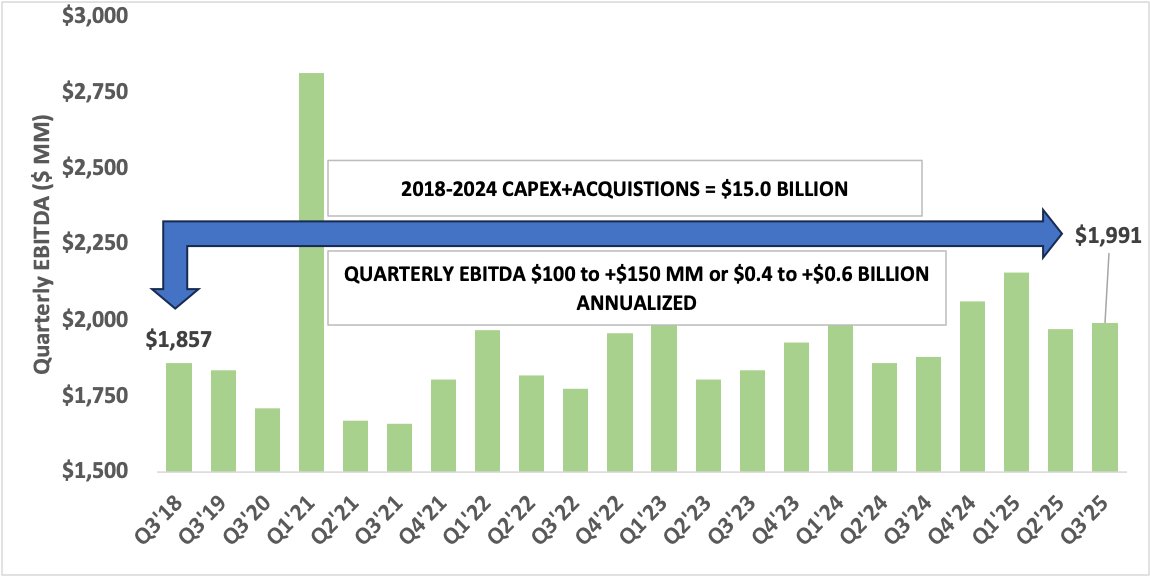

a) Compute ∆ EBITDA b/w Q3'25 & Q3'18

b) Annualize change in (a) = cumulative EBITDA growth

c) Calculate Total Capital Deployed b/w 2018 and 2024 = CAPEX + Acquisitions (incl. stock-for-stock) - Divestitures

Return = ∆ Annualized EBITDA ÷ Capital Deployed

Aug 29, 2024 • 11 tweets • 2 min read

(1/11)

Big transaction in Midstream-land with $OKE acquiring a 43% + GP interest in $ENLC and Medallion Pipeline from GIP for a combined value of $5.9 billion

Let's explore transaction economics beyond the headline numbers quoted in the PR/Presentation

🧵

(2/11)

$OKE presentation states that the $ENLC units + GP interest purchase are being executed at 8.3x 2025 EBITDA and Medallion purchase is being executed at 6.3x 2025 EBITDA

BOTH multiples INCLUSIVE of Base Case SYNERGIES which are, in aggregate, expected to be $250 mm

Mar 7, 2024 • 21 tweets • 5 min read

1/21

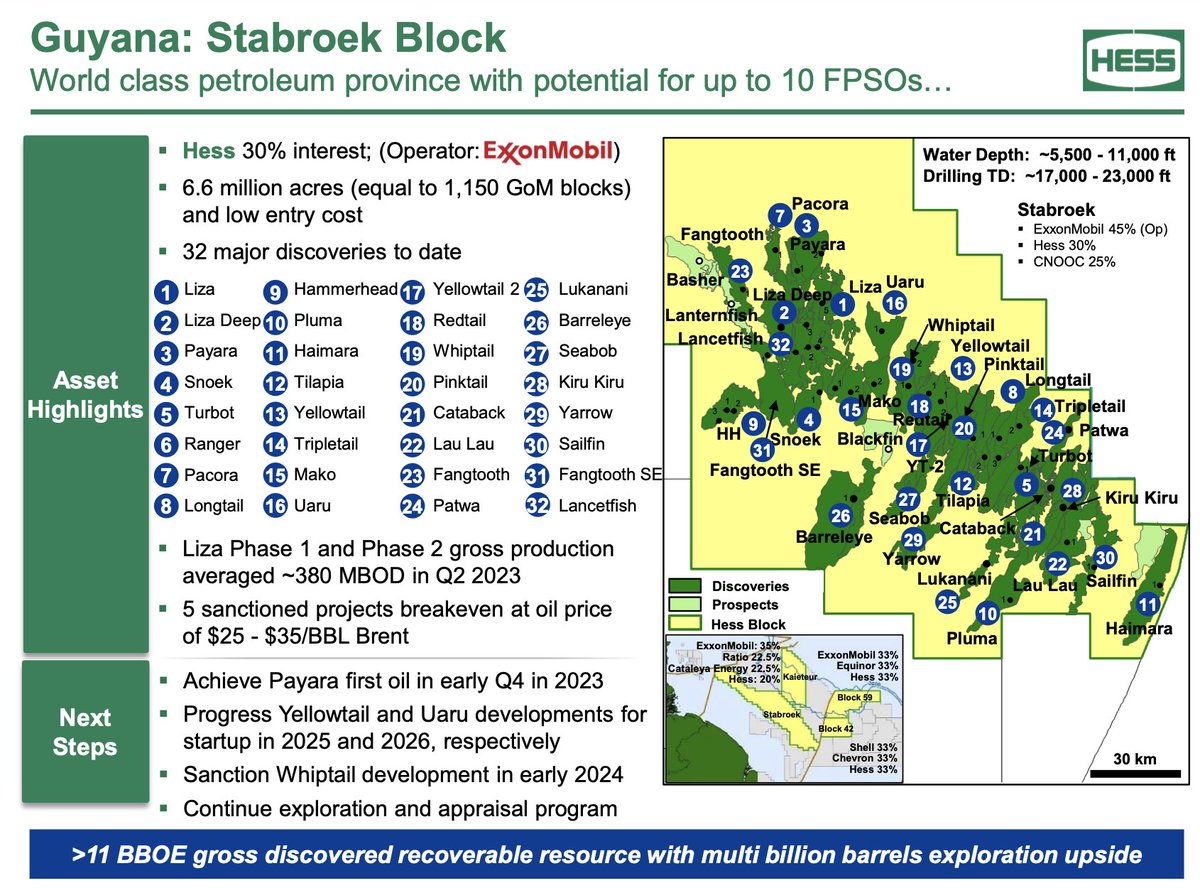

$HES - or more specifically, their 30% Working Interest in Guyana position is at the center of the battle between $XOM and $CVX with the matter of $XOM's ROFR now in arbitration.

I estimate $HES Guyana could be worth $30 to $32 billion.

Let's see why/how. A (long) 🧵

2/21

First: A review of the Guyana Production Sharing Contract

1) Royalty Rate of 2.00% 2) 75.00% Cost Oil Cap 3) 50.00% of Profit Oil to $XOM, $HES, $CNOOC collectively 4) Most Important: NO RING-FENCING

Nov 21, 2023 • 17 tweets • 5 min read

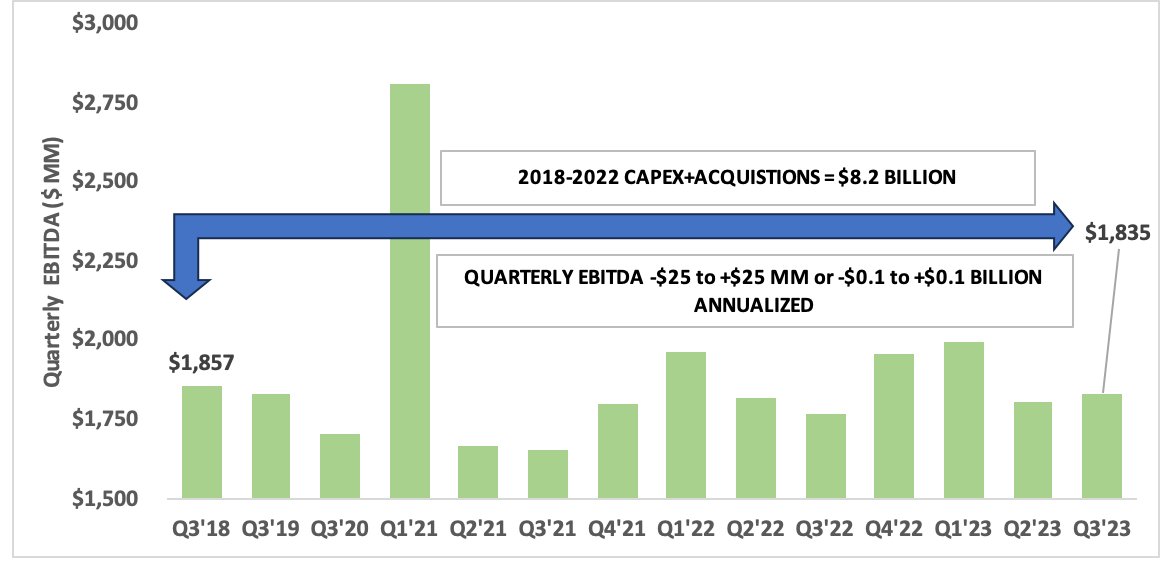

(1/17) Poor capital allocation has long been a source of consternation for US Energy Midstream investors. Starting 2018, the market started pushing back against the sector and the COVID pandemic provided an impetus for change. Has the sector changed its ways? A 🧵

(2/17)

For this exercise, I examine the capital deployment record of major US Midstream C-corps and MLPs since 2018

US C-corps examined: $KMI, $LNG, $OKE, $TRGP, $WMB

US MLPs examined: $EPD, $ET, $MPLX, $PAA

Oct 21, 2023 • 17 tweets • 3 min read

(1/17)

Here is a thread discussing midstream economics across commodities and service types that will hopefully debunk some of the absurdities being thrown around. Long thread:

Let's start with crude oil gathering. Rates can vary anywhere b/w $0.60/bbl to $1.25/bbl. This data is based on my experience looking at $PAA over the years. The rate in the Permian is closer to $1.25/bbl while in places like the Eagle Ford, it is closer to $0.60/bbl.

Jul 28, 2023 • 13 tweets • 3 min read

(1/13)

$TRP.TO out with an announcement to spin-off their Liquids Pipelines business.

A quick thread summarizing some of my thoughts on the SpinCo's valuation, future strategic direction, etc.

(2/13)

The Liquids Pipelines business is a c. C$1.3 to 1.4 billion EBITDA business with the Keystone system being the crown jewel.

Highly contracted assets linking low-decline oil sands production to high-complexity refining centers in the US.

Vital alternative to $ENB.TO

Mar 23, 2022 • 15 tweets • 3 min read

(1/15) Will try to provide my humble (and probably wrong opinion) on the question posed by QDC and Ed Morse’s bearish oil view. Thread 🧵

The main regions of demand growth are India and China.

China oil imports (Bloomberg) totaled ~508 million MT over LTM vs. 505 million MT in 2019

India’s been slower to recover and is running about -7% vs. 2019 (excl. LPGs) - data per Govt data

Jan 10, 2022 • 4 tweets • 1 min read

(1/4)

Thoughts on the $EPD - Navitas deal.

Using a $30/bbl price for NGLs, $3.00/mmbtu for natural gas, Fees of $0.50/mcf, and Opex of $0.20/mcf

EBITDA could range from $345 mm to $461 mm - key variable being % POP (I use a range of 10-15% share)

Deal multiple 7.0-9.4x

(2/4) Decent standalone multiple at $30/bbl NGLs and $3.00/mmbtu

What about downstream b benefits?

This is clearly where $EPD is looking to pick up economics

This will depend on how much of the c. 140 kbpd of NGLs can move on Shin Oak and then on to $EPD Fracs and dock

Nov 16, 2020 • 15 tweets • 4 min read

Hydrogen (H2) thread. Long but there's much to consider. H2 increasingly viewed as the solution for climate change issues.

$1/kg is the level that most consider as the point when H2 becomes the "silver bullet".

Two main pathways to produce H2 today:

1) Steam Reforming of Methane (SRM) 2) Electrolysis

Since SRM involves breaking down Methane (CH4), we will not discuss this here since it does not solve the CO2 issue. We will only examine Electrolysis.