Systematic trader, fund manager. Web: https://t.co/Qga9clOPid

Step 1 - Primary research stays human-driven.

Step 1 - Primary research stays human-driven. 2/ The setup:

2/ The setup: 1/ The Philosophy

1/ The Philosophy 1/ What is a "Swing"?

1/ What is a "Swing"?

The idea is simple:

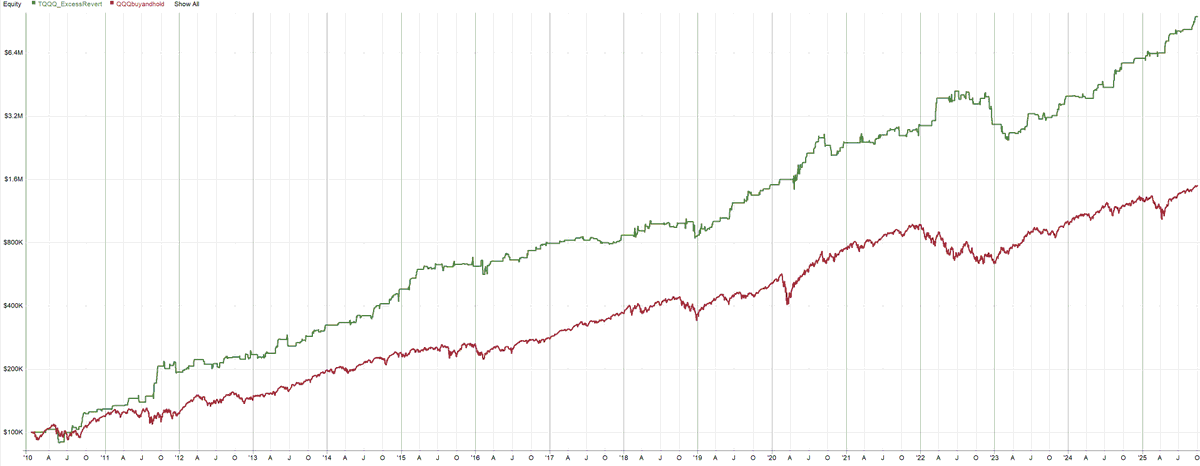

The idea is simple: Leveraged ETFs (like $TQQQ, 3× $QQQ) don’t perfectly track their target.

Leveraged ETFs (like $TQQQ, 3× $QQQ) don’t perfectly track their target. 2/6

2/6 1/

1/ 2/5 My personal game-changer?

2/5 My personal game-changer? (2/7) The Allure & Danger of Raw Profit

(2/7) The Allure & Danger of Raw Profit