Long-Term Investor | Focus on Quality Fundamental Analyses and Insights | Join 4000+ readers: https://t.co/XZyrRNCFMg | https://t.co/hbCC9qnITA

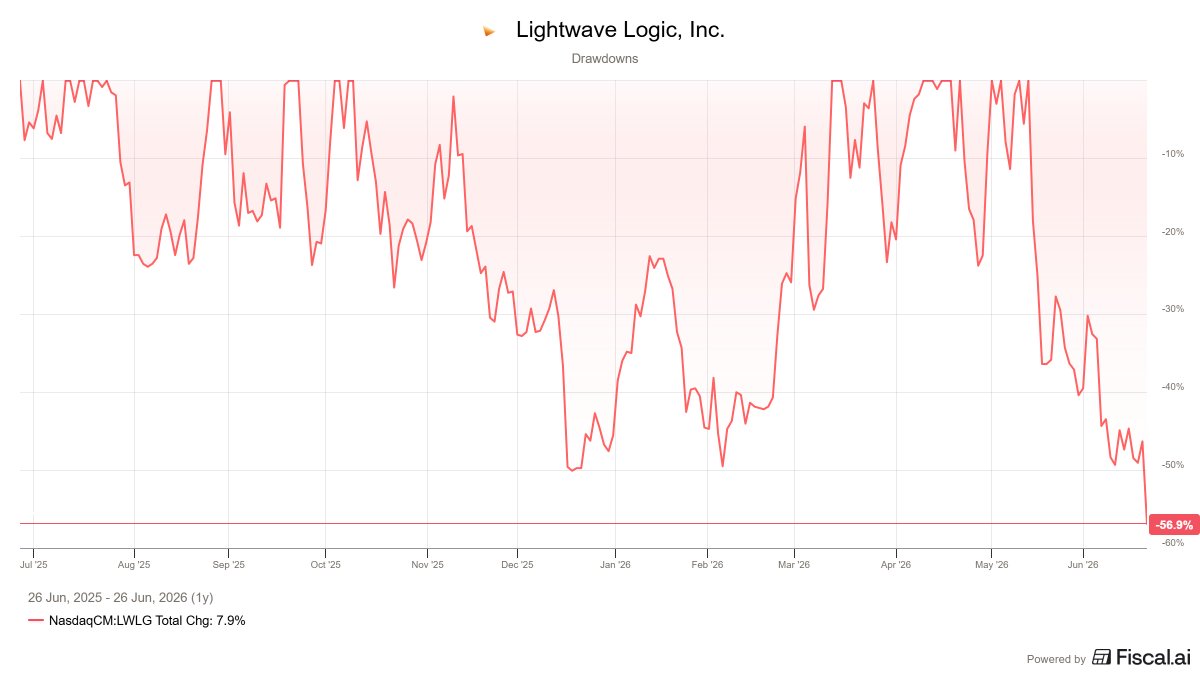

2. $LWLG - 57%

2. $LWLG - 57%

2. $NOW - ServiceNow

2. $NOW - ServiceNow

2. $ADBE - Adobe

2. $ADBE - Adobe

1/ Origin story

1/ Origin story

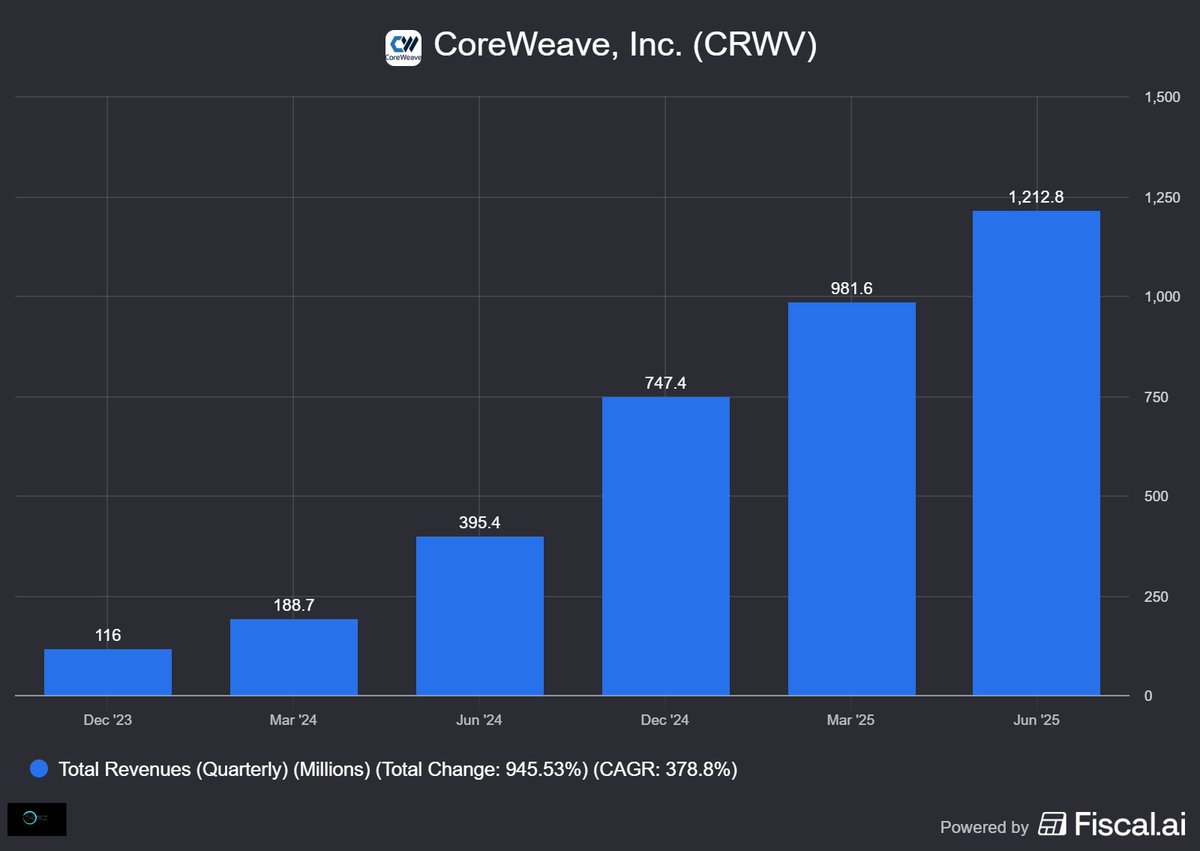

2/ $CRWV | Coreweave

2/ $CRWV | Coreweave

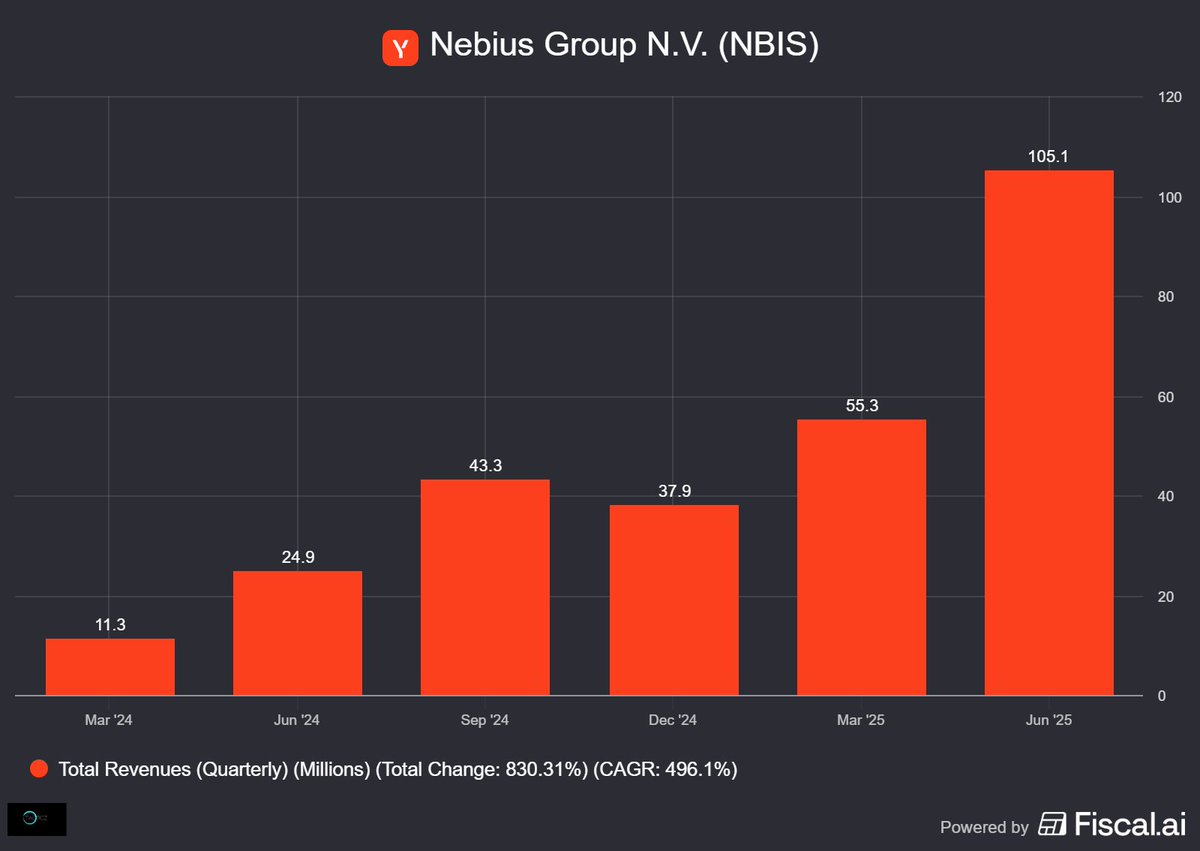

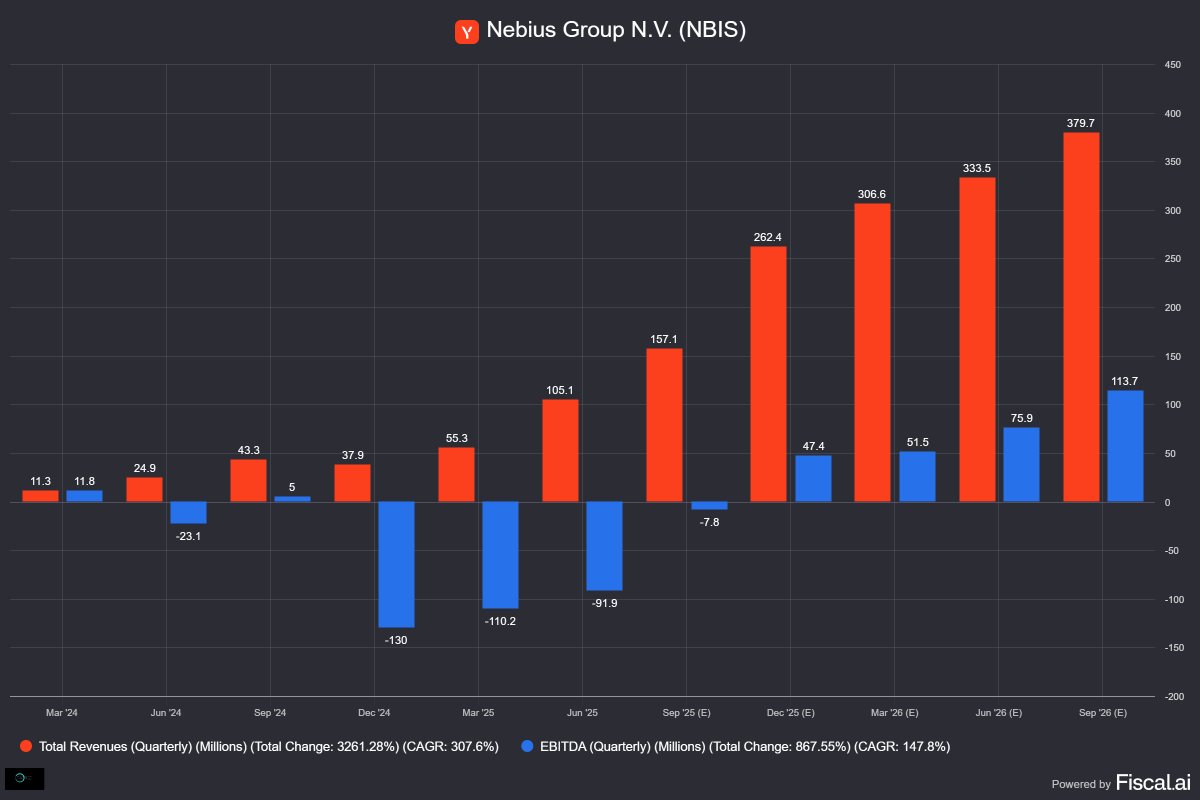

2/ $NBIS | Nebius

2/ $NBIS | Nebius

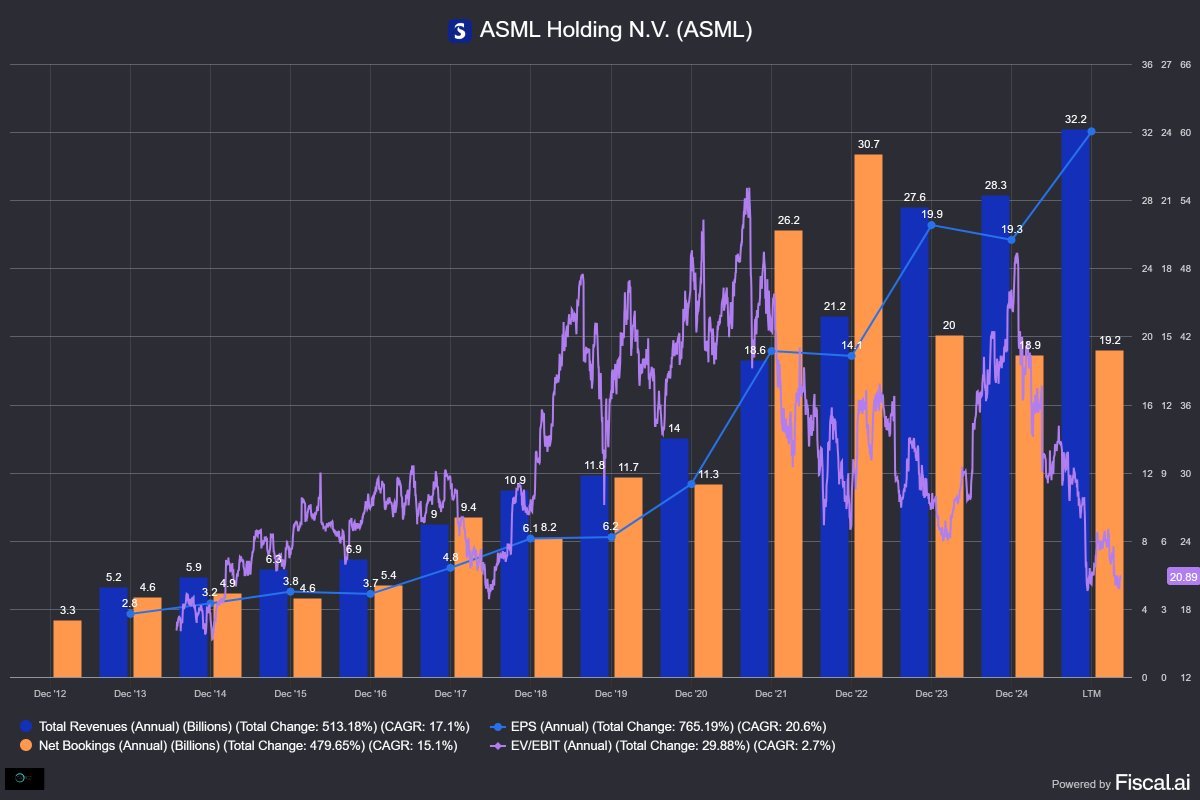

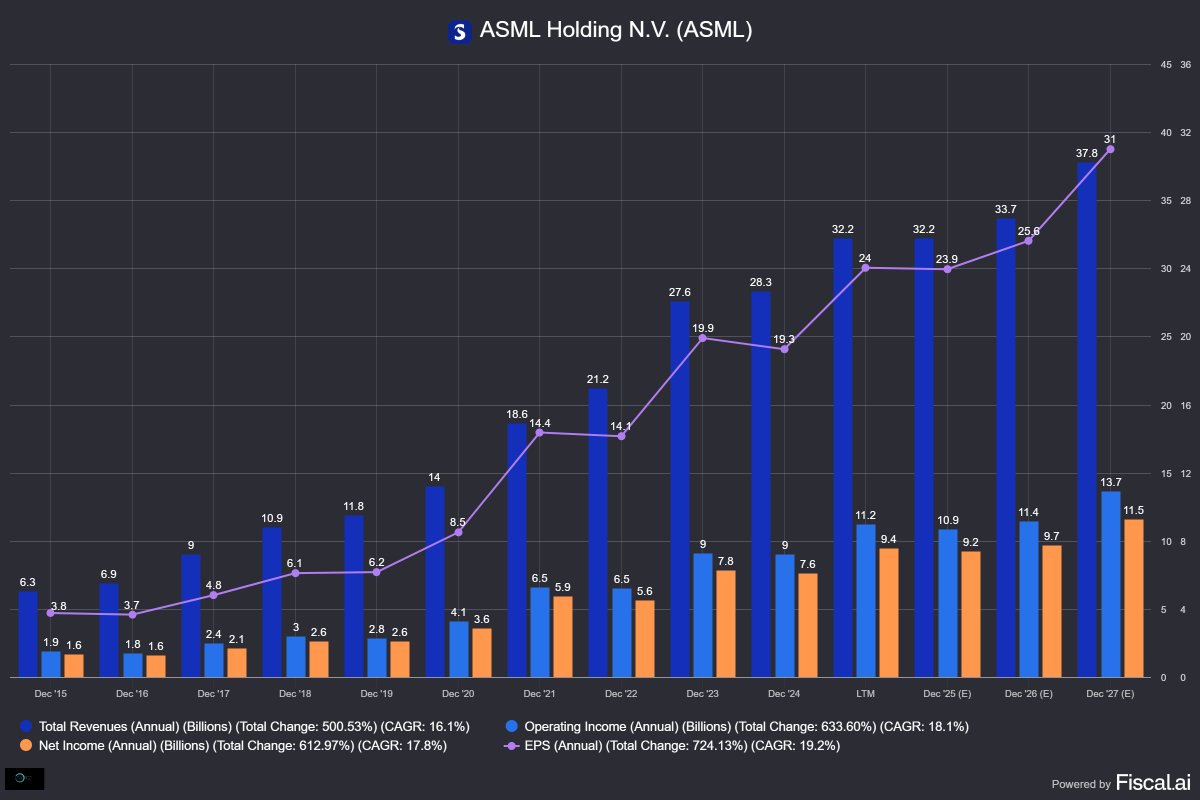

2/ $ASML | ASML

2/ $ASML | ASML

2/ The price collapse

2/ The price collapse

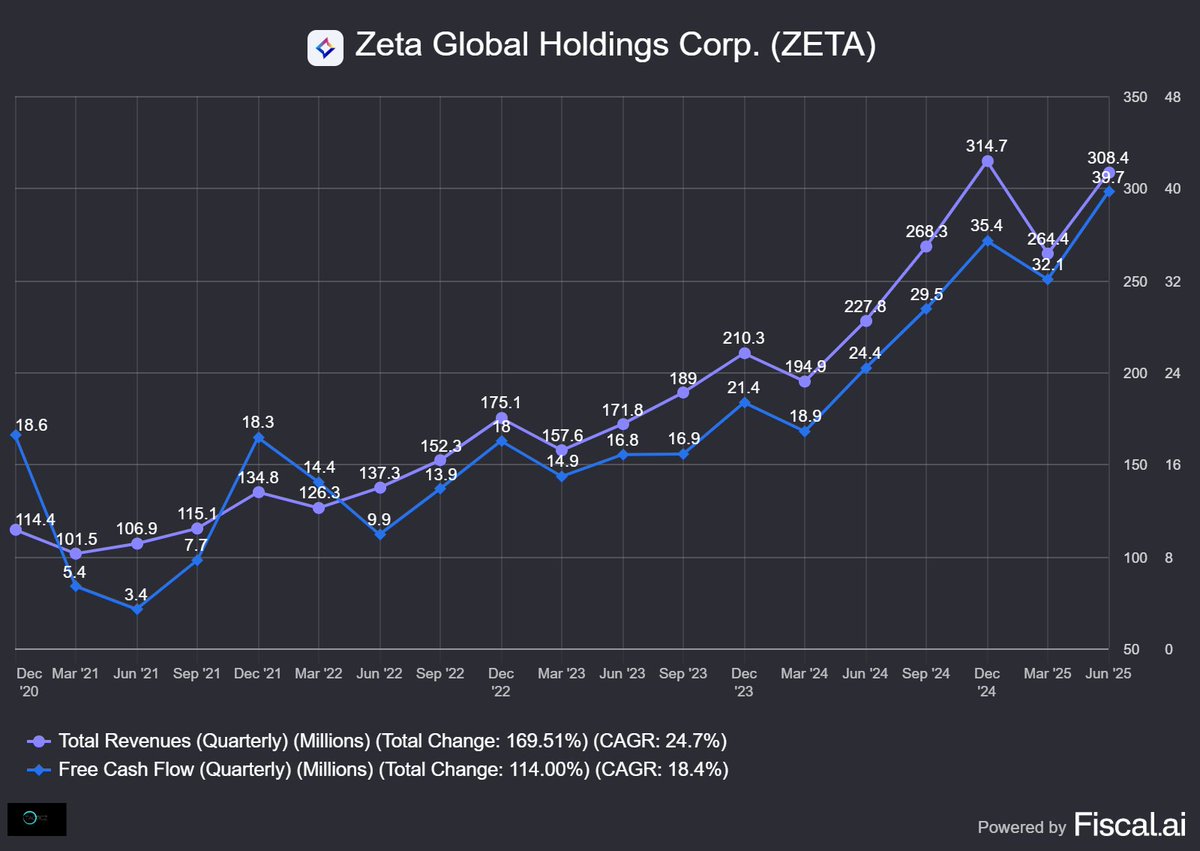

2/ $ZETA | Zeta Holdings

2/ $ZETA | Zeta Holdings

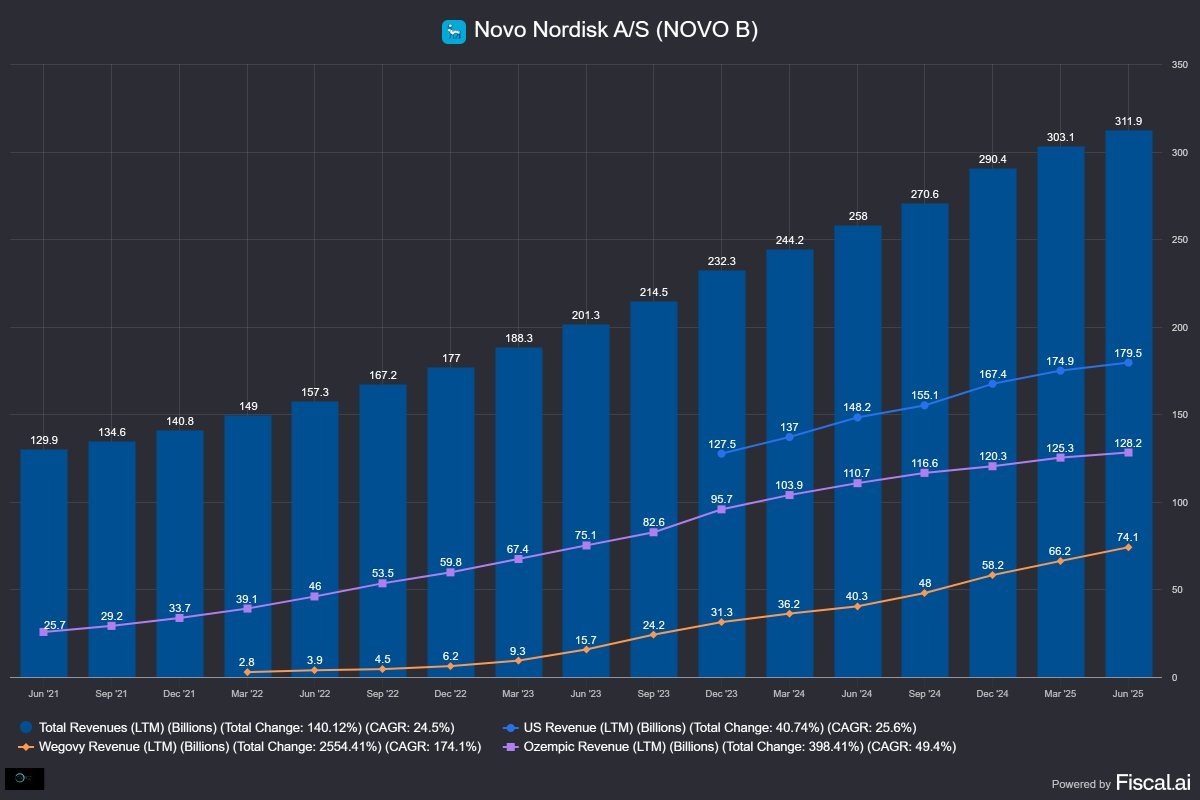

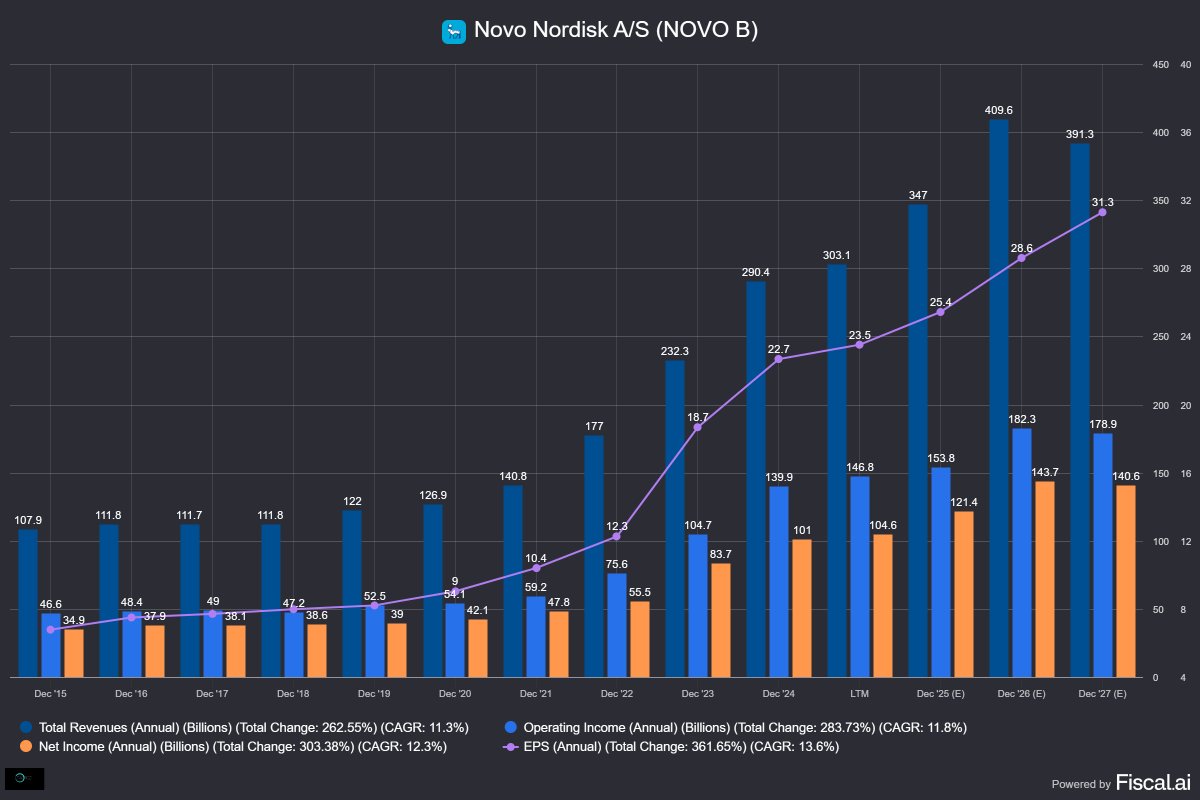

2/ $NVO

2/ $NVO

1/ The Company 🇩🇰

1/ The Company 🇩🇰

1/ $DLO The company 🇺🇾

1/ $DLO The company 🇺🇾 1/ The Company 🇳🇱

1/ The Company 🇳🇱

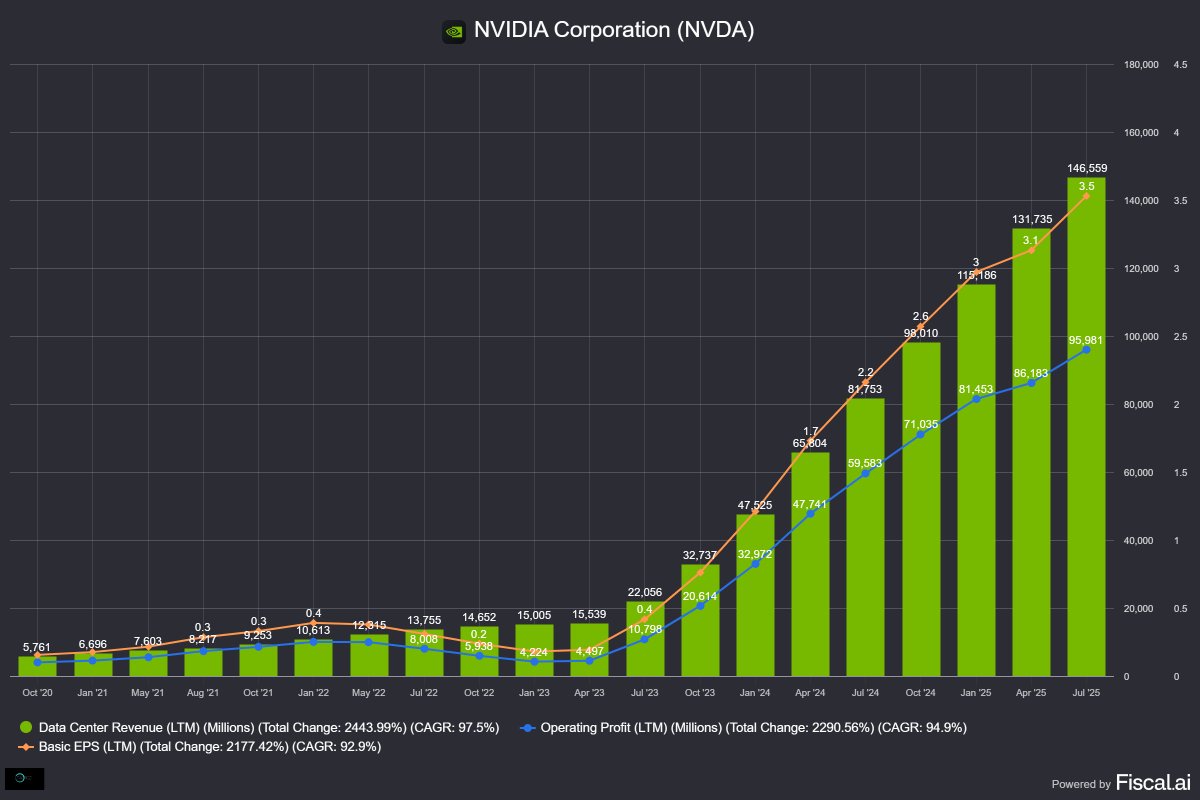

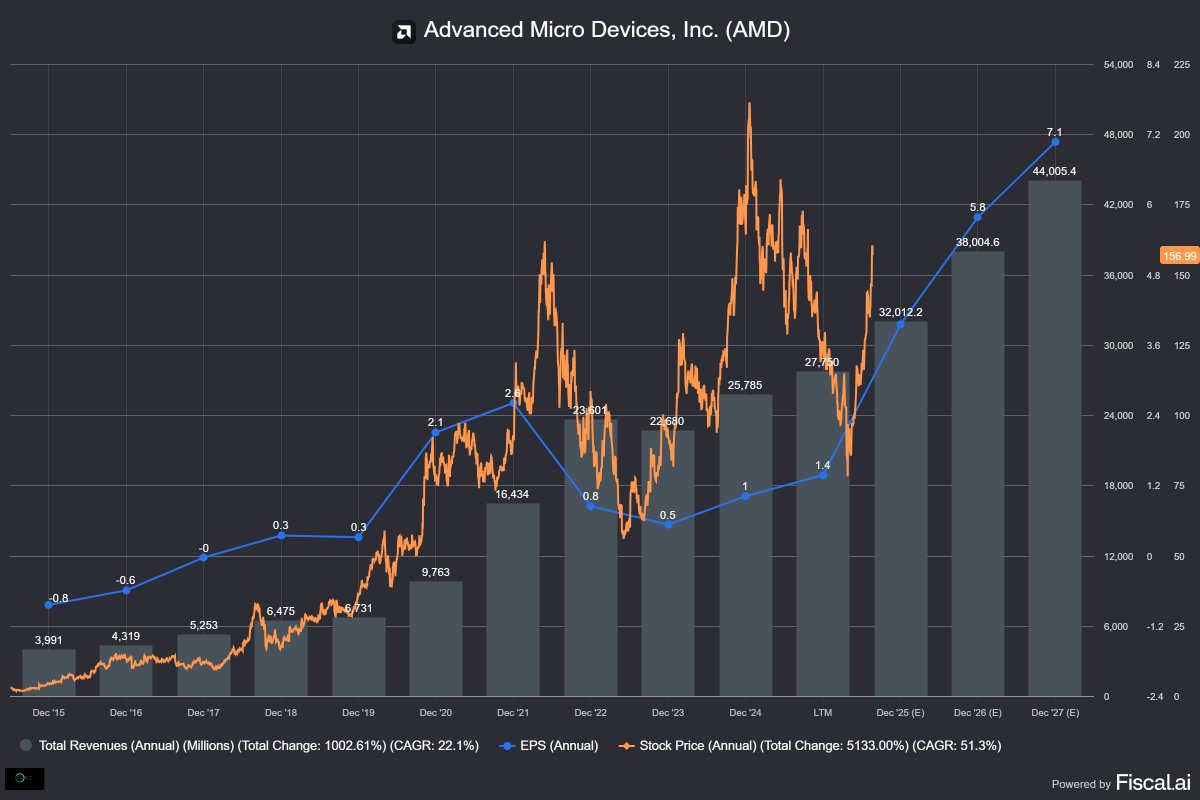

2/ $AMD

2/ $AMD

1/ $EVO Revenue growth accelerated

1/ $EVO Revenue growth accelerated

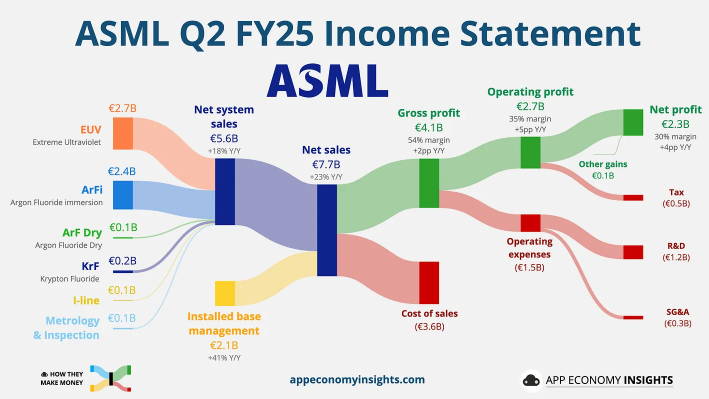

2/ ASML 🇳🇱

2/ ASML 🇳🇱

2/ $DLO

2/ $DLO

2/ $NVO

2/ $NVO

2/ One-stop Shop

2/ One-stop Shop

2/ Sign of confidence

2/ Sign of confidence

2/ $CRWV Coreweave

2/ $CRWV Coreweave