Tech investor for ~25 years. Ran large hedge fund for 10 of those. Here to help. Not investment advice. I never reach out to sell ANYTHING.

How to think about buying indexes when trading at above average multiples?

How to think about buying indexes when trading at above average multiples?

Semis

Semis

"Can you help me buy car insurance"

"Can you help me buy car insurance"

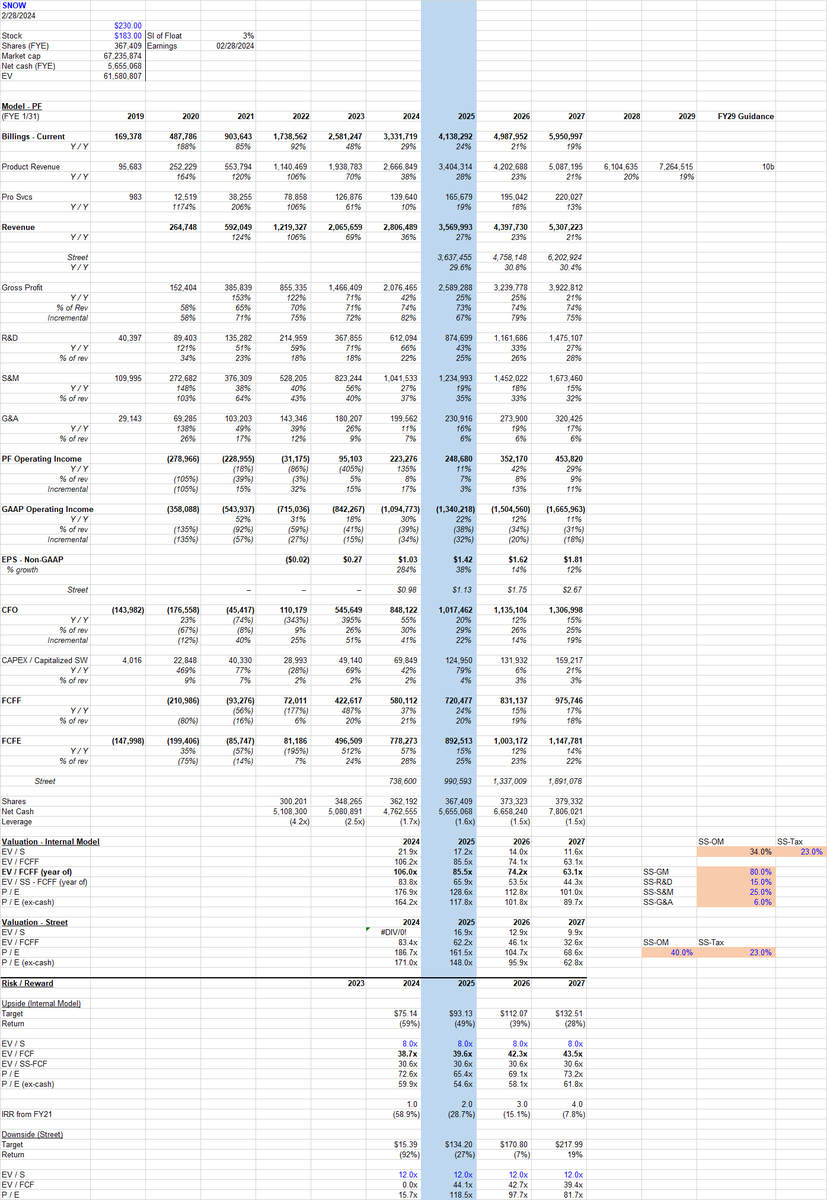

Qtr was fine:

Qtr was fine:  New CEO: The CEO change is not that surprising as Slootman had been running the company from Bozeman (and remote work is not this guy’s style) but the timing does seem abrupt. New CEO is not from central casting – 15 years at GOOGL primarily in engineering but then ran Ads / Commerce for 5 years. Then cofounded Neeva which was a consumer-focused search start-up he ran for 4 years. Slootman is an enterprise software carnivore, and the new guys has modest relevant experience. He still has “Learning Snowflake” as his current role on LinkedIn. Oh boy. Doesn't strike me as normal CEO change so either CEO did something untoward or board fired him for basically missing the AI boat and now having to play catch-up from far behind.

New CEO: The CEO change is not that surprising as Slootman had been running the company from Bozeman (and remote work is not this guy’s style) but the timing does seem abrupt. New CEO is not from central casting – 15 years at GOOGL primarily in engineering but then ran Ads / Commerce for 5 years. Then cofounded Neeva which was a consumer-focused search start-up he ran for 4 years. Slootman is an enterprise software carnivore, and the new guys has modest relevant experience. He still has “Learning Snowflake” as his current role on LinkedIn. Oh boy. Doesn't strike me as normal CEO change so either CEO did something untoward or board fired him for basically missing the AI boat and now having to play catch-up from far behind.

Deliveries -> Bad. 1,734 were up 19% qq but missed guidance of 1,800, and well below production of 2,391 in the qtr. This is a new car company in a scale game, so they need deliveries to be exploding right now for this to work. Deliveries for the year were 5,997 up 37% - they need to be growing >100% at this small scale. (2/9)

Deliveries -> Bad. 1,734 were up 19% qq but missed guidance of 1,800, and well below production of 2,391 in the qtr. This is a new car company in a scale game, so they need deliveries to be exploding right now for this to work. Deliveries for the year were 5,997 up 37% - they need to be growing >100% at this small scale. (2/9)