Abojani for everyday investor. Empowering retail investors through investor education || Contact us: learning@abojani.com

Telegram https://t.co/sK9t9VIeeL

@cheruiyotkb @Davinedavid1 @mmnjug A REIT is essentially a regulated investment structure that pools capital from multiple investors to acquire, manage, and operate income-generating real estate. Instead of owning a building directly, investors own units in a trust that holds property assets.

@cheruiyotkb @Davinedavid1 @mmnjug A REIT is essentially a regulated investment structure that pools capital from multiple investors to acquire, manage, and operate income-generating real estate. Instead of owning a building directly, investors own units in a trust that holds property assets.

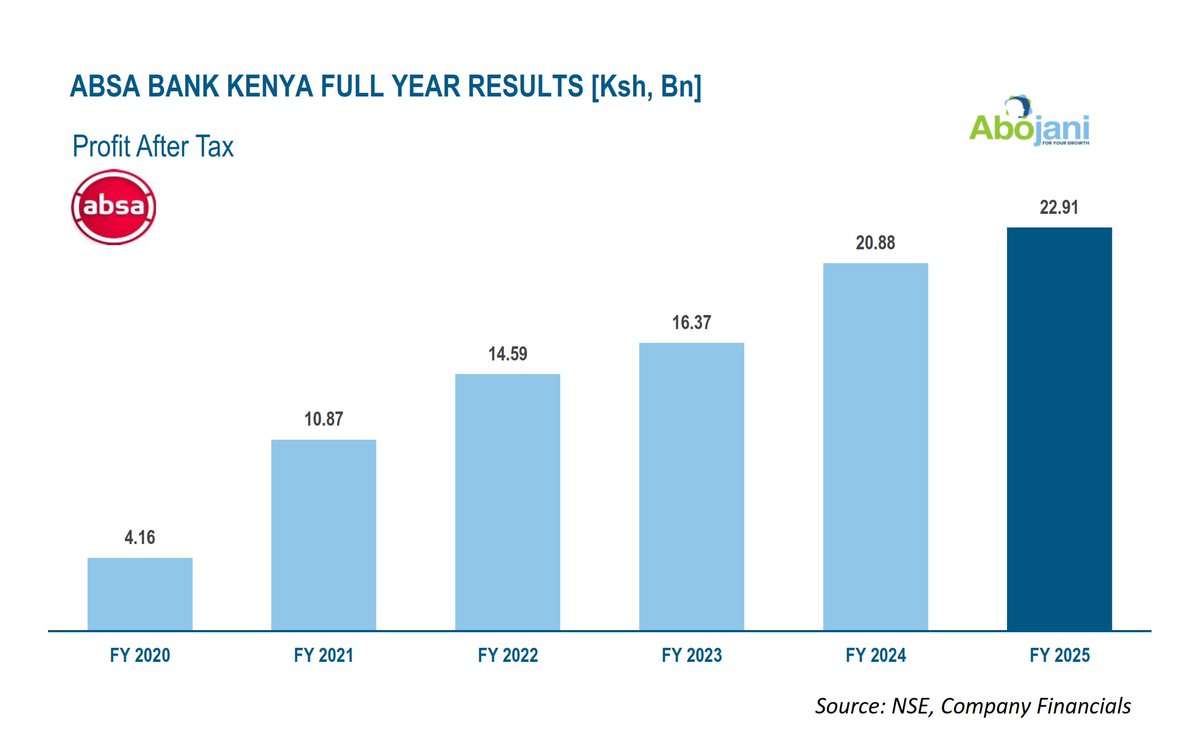

Five years later, the results are in.

Five years later, the results are in.

A Real Estate Investment Trust is a regulated investment vehicle that pools money from many investors to collectively own and operate income-generating properties. Think of it like a unit trust, but instead of holding stocks or bonds, it holds real assets; office buildings, shopping malls, student accommodation, industrial parks.

A Real Estate Investment Trust is a regulated investment vehicle that pools money from many investors to collectively own and operate income-generating properties. Think of it like a unit trust, but instead of holding stocks or bonds, it holds real assets; office buildings, shopping malls, student accommodation, industrial parks.

1. Build Something

1. Build Something In practice, traditional real estate investing comes with barriers that are difficult to ignore. The capital required to enter the market is often high, making it inaccessible to many. The assets themselves are illiquid, meaning they cannot be easily converted to cash when needed. There is also the operational burden of managing property, tenants, and maintenance. On top of this, direct ownership often concentrates risk in one location or one asset.

In practice, traditional real estate investing comes with barriers that are difficult to ignore. The capital required to enter the market is often high, making it inaccessible to many. The assets themselves are illiquid, meaning they cannot be easily converted to cash when needed. There is also the operational burden of managing property, tenants, and maintenance. On top of this, direct ownership often concentrates risk in one location or one asset.

You see, retirement can be a ruthless teacher. Reality quickly hit home for Dr.Odundo even as his busy schedule changed. Through his personal experiences in retirement, he now shares 5 Mantras that have helped him thrive and maintain his quality of life….

You see, retirement can be a ruthless teacher. Reality quickly hit home for Dr.Odundo even as his busy schedule changed. Through his personal experiences in retirement, he now shares 5 Mantras that have helped him thrive and maintain his quality of life….

One evening, after closing shop and getting home, his phone rang around 9 p.m.

One evening, after closing shop and getting home, his phone rang around 9 p.m. One of the biggest mistakes is treating budgeting as a once-a-month exercise instead of a daily financial system. People create a budget at the beginning of the month with good intentions, but without tracking or discipline, it quickly becomes a theoretical document. Spending happens based on emotion, convenience, and social pressure rather than the plan. Eventually, the budget is abandoned altogether, and money begins to move without direction......

One of the biggest mistakes is treating budgeting as a once-a-month exercise instead of a daily financial system. People create a budget at the beginning of the month with good intentions, but without tracking or discipline, it quickly becomes a theoretical document. Spending happens based on emotion, convenience, and social pressure rather than the plan. Eventually, the budget is abandoned altogether, and money begins to move without direction......

Research documented by the Harvard Business Review shows that 70–90% of mergers and acquisitions fail to create shareholder value or achieve their intended outcomes.

Research documented by the Harvard Business Review shows that 70–90% of mergers and acquisitions fail to create shareholder value or achieve their intended outcomes.

1. Fire or property damage:

1. Fire or property damage:  1⃣Audit Your Financial Life

1⃣Audit Your Financial Life  Simply linked to customers’ existing DTB debit cards, this solution eliminates the need to carry cash, physical cards, or mobile phones, providing a seamless and convenient payment experience.

Simply linked to customers’ existing DTB debit cards, this solution eliminates the need to carry cash, physical cards, or mobile phones, providing a seamless and convenient payment experience.

2) HF Group reported a profit before tax of Ksh 1.61 billion for the financial year ended 2025, representing a 250% growth from Ksh 0.46 billion recorded in 2024.

2) HF Group reported a profit before tax of Ksh 1.61 billion for the financial year ended 2025, representing a 250% growth from Ksh 0.46 billion recorded in 2024.

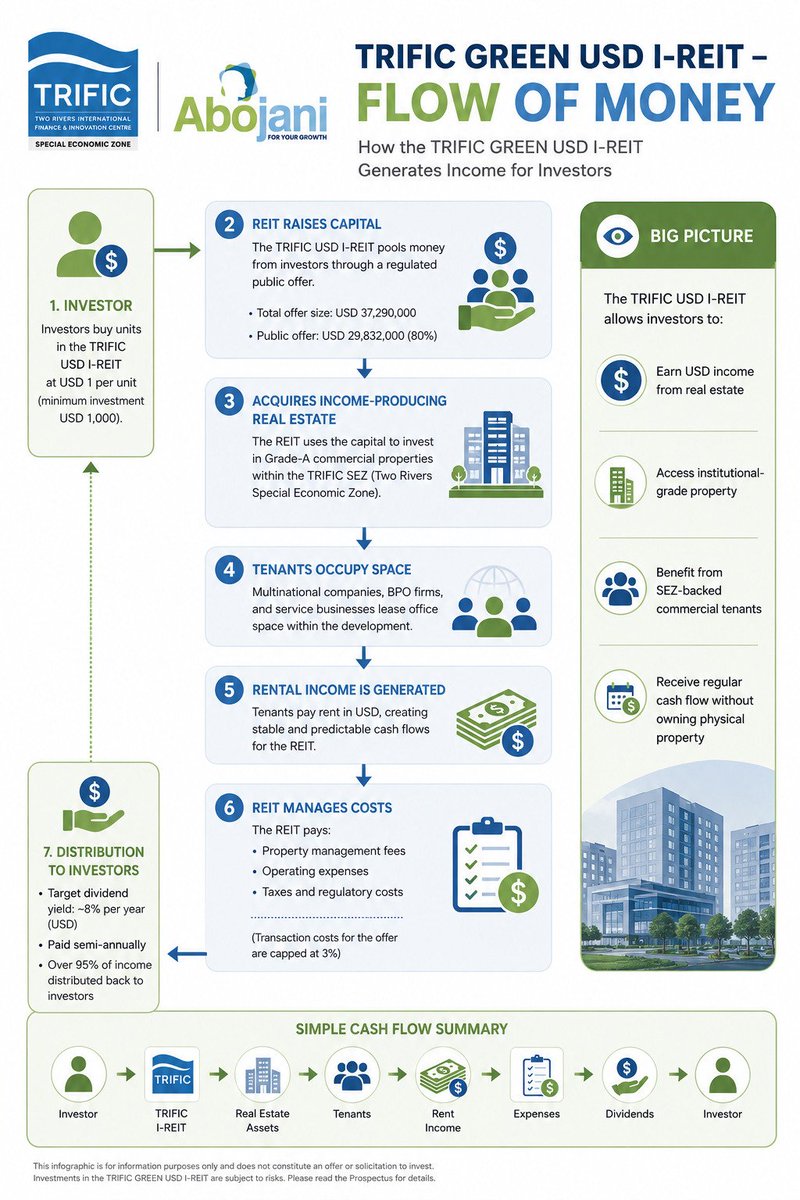

The framework that defines SEZs is governed by the Special Economic Zone Act and regulated by the Special Economic Zones Authority (SEZA). According to @SEZAuthority_ke Annual Report 2024, the authority noted cumulative investment commitments of approximately KES 91 billion across licensed SEZs. While commitments reflect investor confidence, actual capital deployment and operationalization remain the more critical long-term goal.

The framework that defines SEZs is governed by the Special Economic Zone Act and regulated by the Special Economic Zones Authority (SEZA). According to @SEZAuthority_ke Annual Report 2024, the authority noted cumulative investment commitments of approximately KES 91 billion across licensed SEZs. While commitments reflect investor confidence, actual capital deployment and operationalization remain the more critical long-term goal.

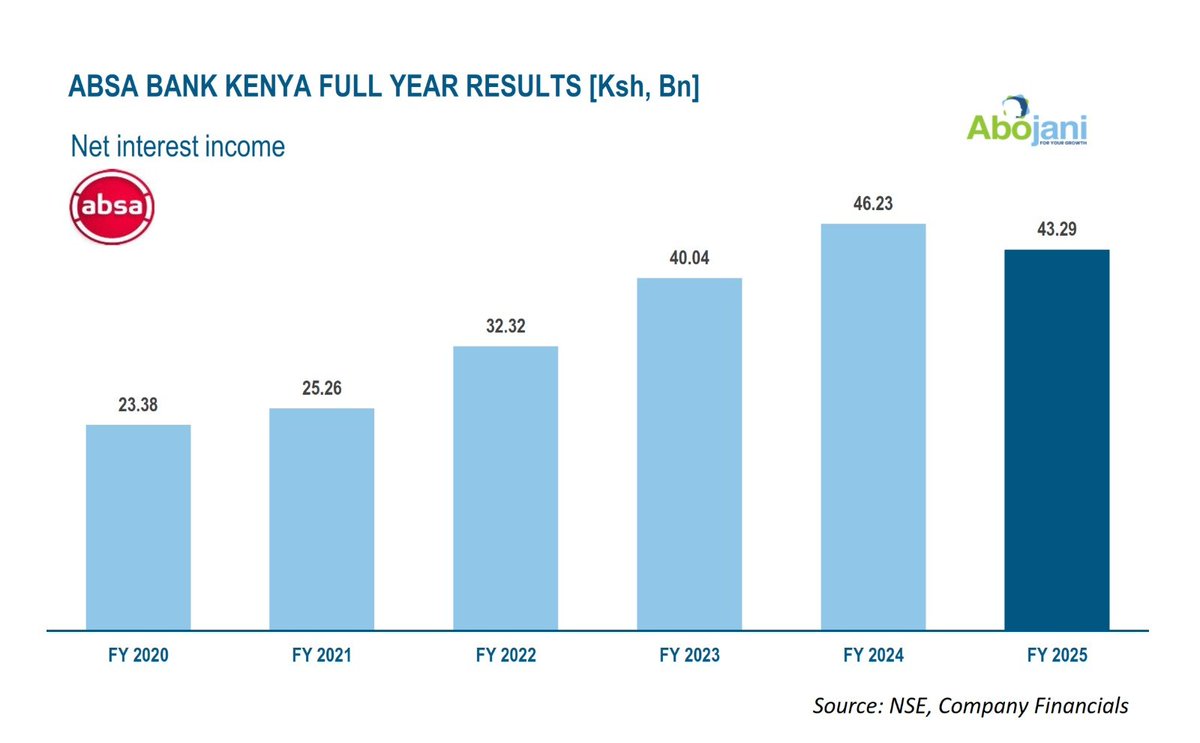

2⃣Net Interest Income

2⃣Net Interest Income

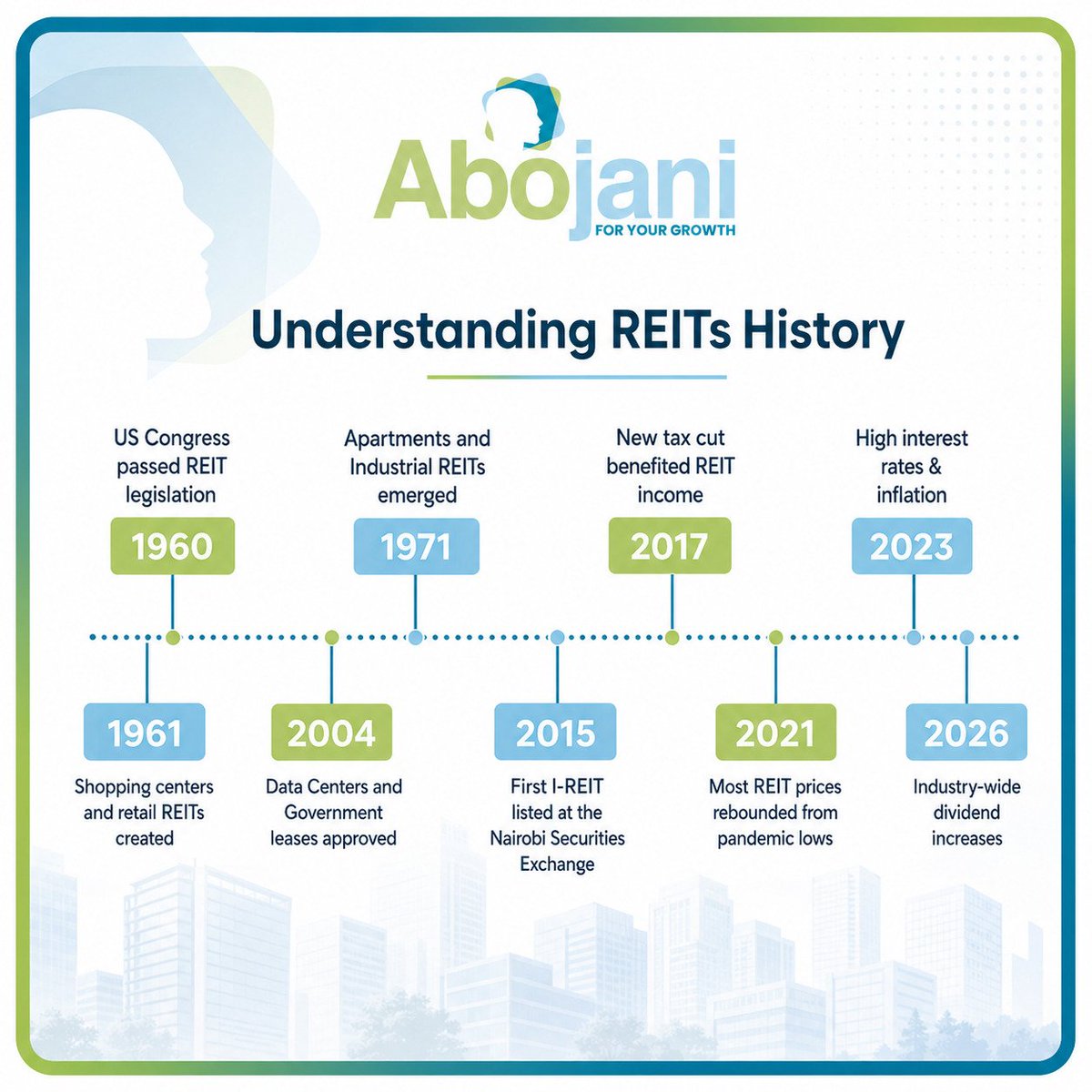

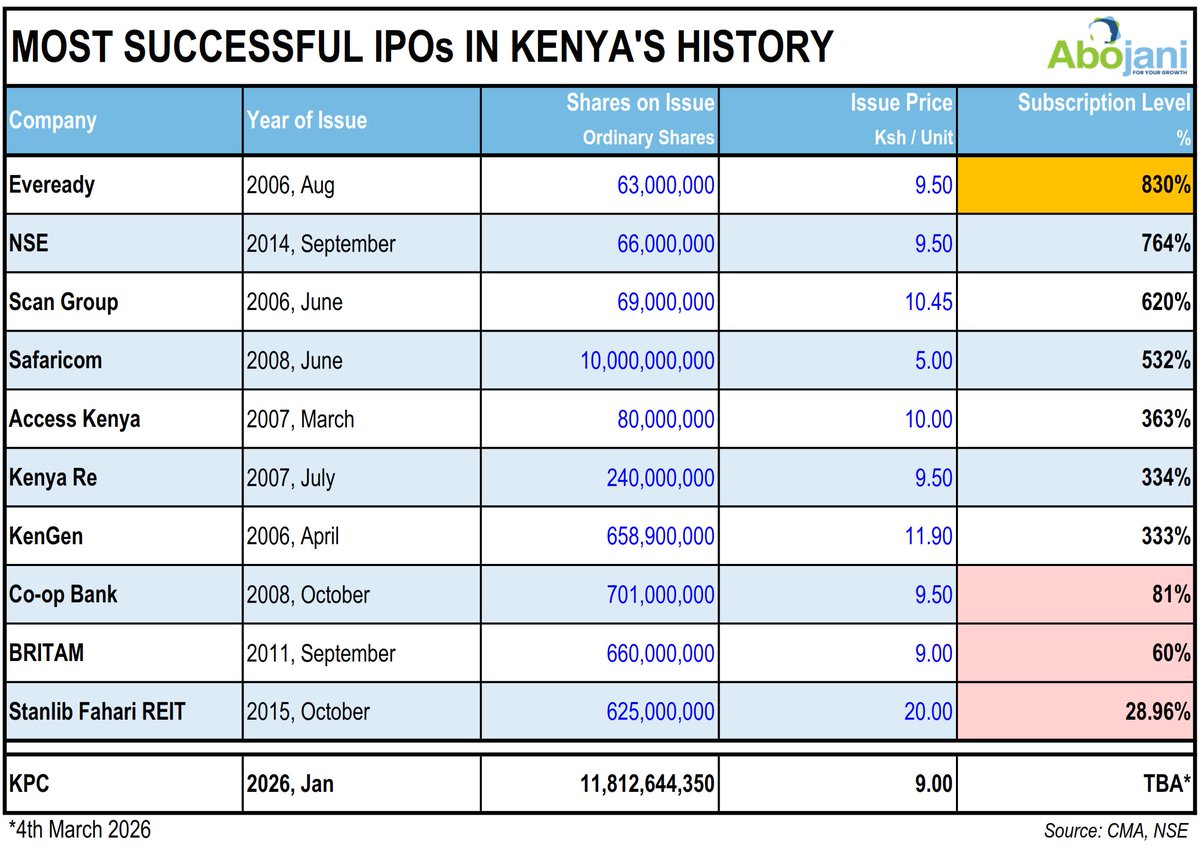

Back home, Kenya Commercial Bank was the first company to issue an IPO in Kenya, listing at Sh20.00 in 1988 at the Nairobi Securities Exchange.

Back home, Kenya Commercial Bank was the first company to issue an IPO in Kenya, listing at Sh20.00 in 1988 at the Nairobi Securities Exchange.

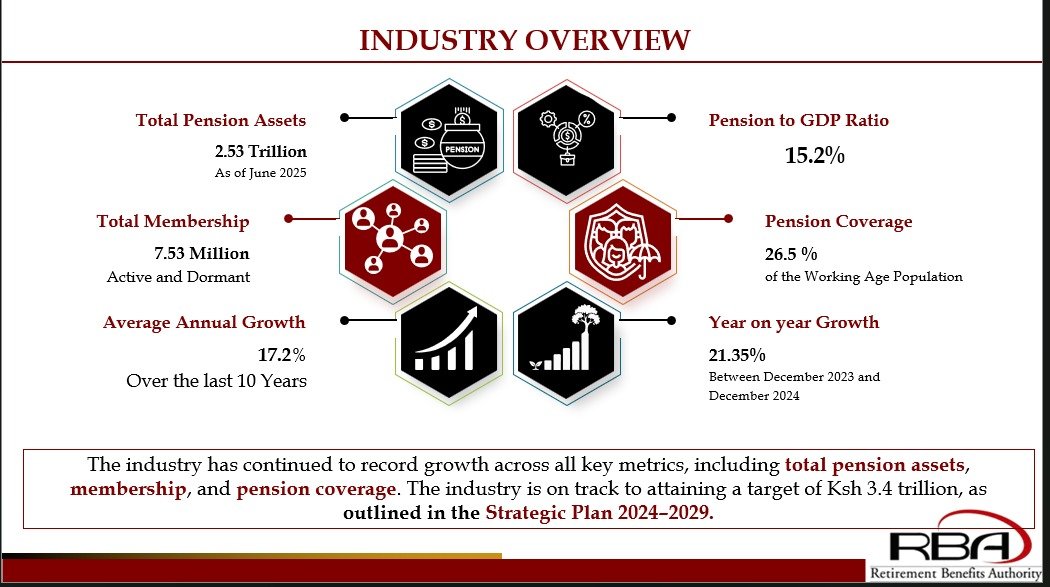

The retirement industry in Kenya is regulated by the Retirement Benefits Authority which just celebrated its Silver Jubilee in 2025.

The retirement industry in Kenya is regulated by the Retirement Benefits Authority which just celebrated its Silver Jubilee in 2025.