I run a real estate private equity firm. 300+ clients helped, $50MM+ in deal volume with the Acquisitions Bootcamp: https://t.co/dWVeG9SxuB

The first thing you’ll want to take a look at are the rents.

The first thing you’ll want to take a look at are the rents. 1. Having to take on short-term bridge debt

1. Having to take on short-term bridge debt The goal is twofold. 1. To be able to build a P&L in the market from scratch and 2. To know where/where not to buy in the market

The goal is twofold. 1. To be able to build a P&L in the market from scratch and 2. To know where/where not to buy in the market // Deal 1 //

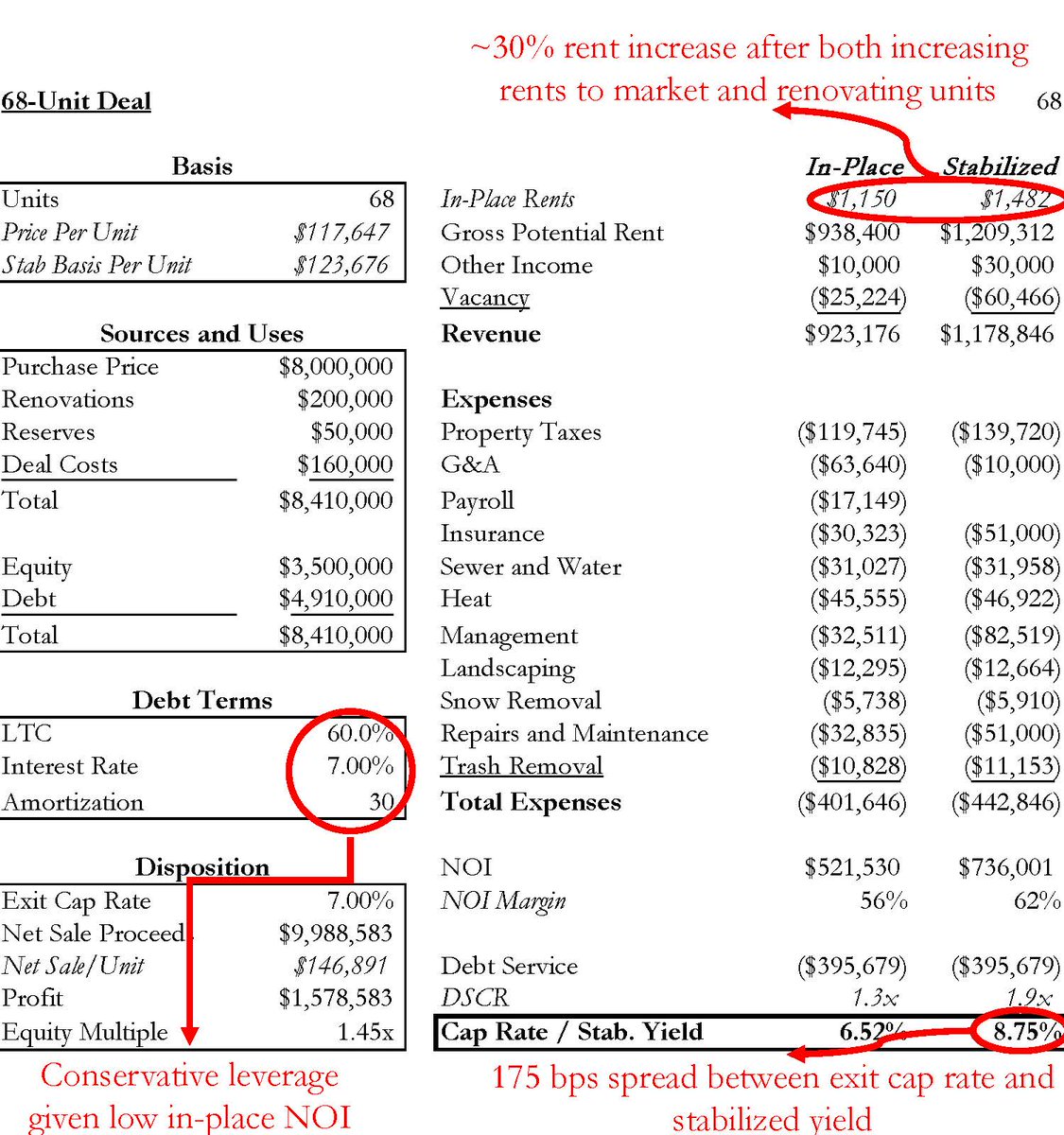

// Deal 1 // Step 1: Look for cities/towns under 250k population

Step 1: Look for cities/towns under 250k population // Deal 1 //

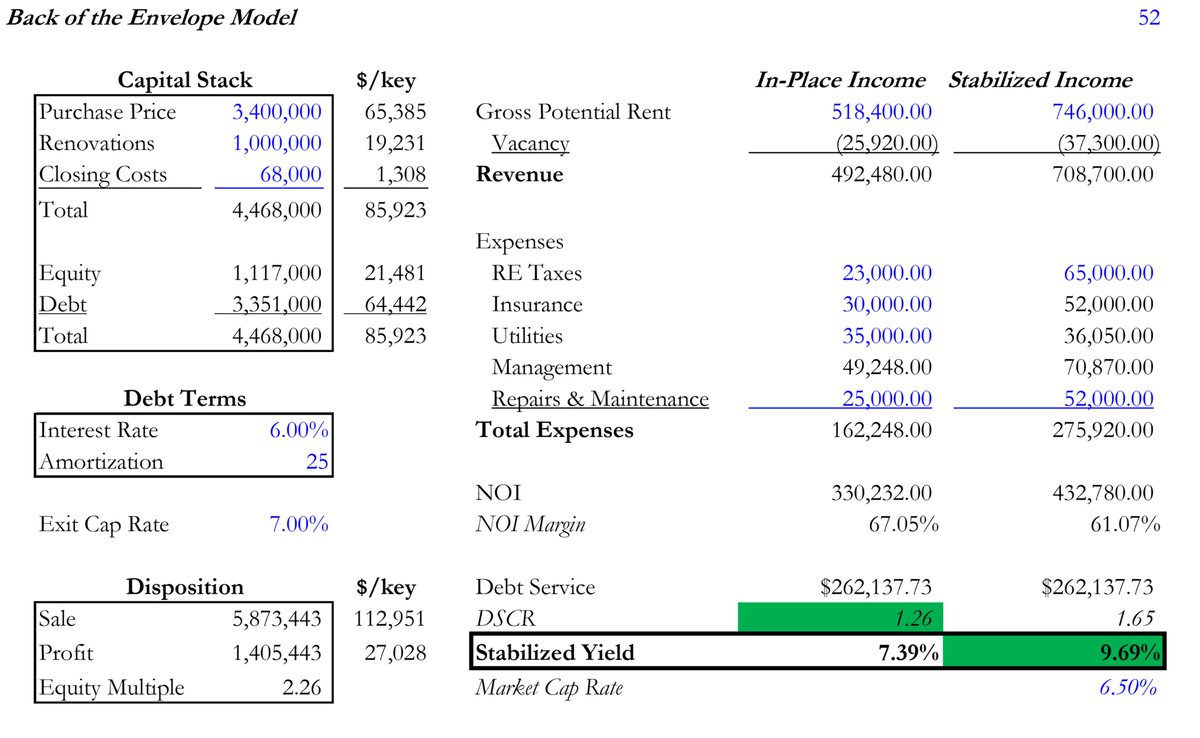

// Deal 1 // 1. Stabilized cap rate (yield):

1. Stabilized cap rate (yield):  // Deal 1 //

// Deal 1 // 1. Stabilized cap rate (yield):

1. Stabilized cap rate (yield):  // Deal 1 //

// Deal 1 // 1. The deal wasn’t listed on loopnet (came straight from a not-that-well-known broker). Means 90%+ of the market didn’t even see it

1. The deal wasn’t listed on loopnet (came straight from a not-that-well-known broker). Means 90%+ of the market didn’t even see it 1. Stabilized cap rate (yield):

1. Stabilized cap rate (yield):  Step 1: Look for cities/towns under 250k population

Step 1: Look for cities/towns under 250k population