In light of OPEC panic. A quick lesson on US shale.

1. Producers have 20% quarterly decline rate. 2. Existing production is CF breakeven at 15-20/bbl on a blended basis between crude, NGL and gas 3. At 75 WTI the weighted sale price is ~50/bbl on average

So producers net 30-35/bbl gross CF. But declines are massive. Next quarter revenue declines 20% (and opex increases).

Hence that 25/bbl or so is reinvested into new wells. Good wells use 20/bbl. Bad ones 30.

Crude is 40%-50% of each new well. NGL/NG is split balance

Dec 9, 2024 • 9 tweets • 2 min read

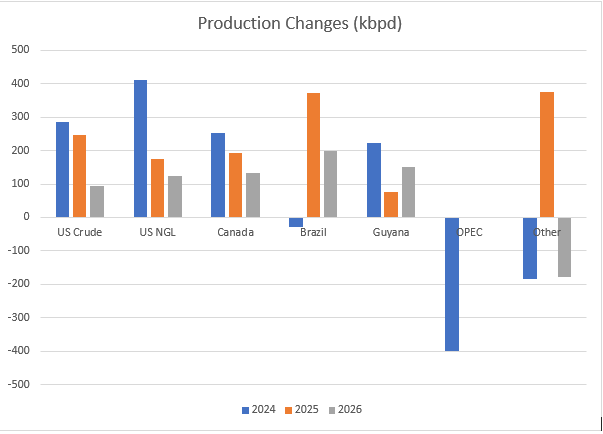

Lots of bearish SD models out there – and tremendous amounts of revisions happening at research firms and banks wrt OPEC, non OPEC and demand all at once.

So what do I see?

1/n

I am a strong advocate of Iran/Ven sanction enforcement under Trump.

Will get to that but first lets look at supply and demand predictions at the current curve for ’25 and ‘26.

2/n

Sep 5, 2024 • 8 tweets • 3 min read

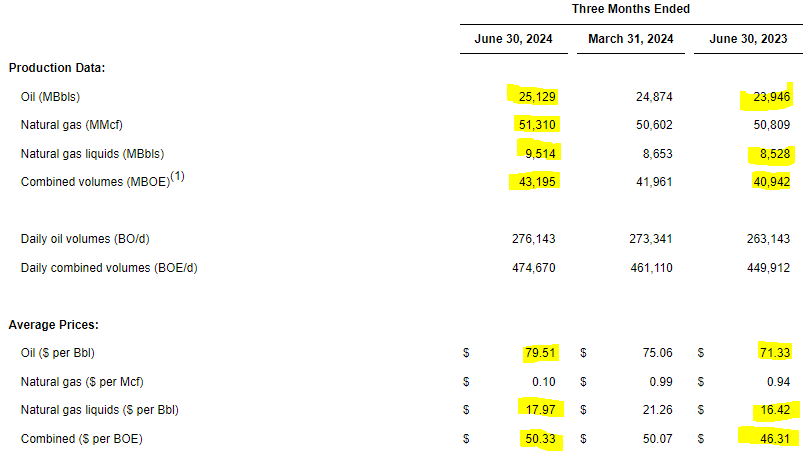

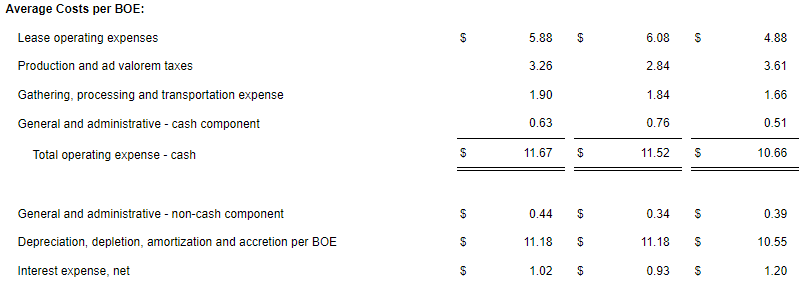

Lets talk Permian economics a moment.

I want to start with FANG has as a proxy for 1st tier geology/ops/infrastructure. This should be the lowest cost, highest volume/well.

The produce 58% oil and roughly 21% NGLs and 21% NG.

Their volume an pricing is below

1/n

#OOTT

They are a low cost operator (~13/bbl) that has increases over 1.00/bbl in the last yr.

They roughly lose 22% of volumes due to declines each quarter.

They spend ~600mm each quarter to drill and tie in ~80 wells - 7.5mm/well (cheap!).