Gen Z boy in a Gen X body.

Pronounciation: Jew ZEP peh (NOT pay!) Pah lay AW! low go.

Sister account: @yogappygappy.

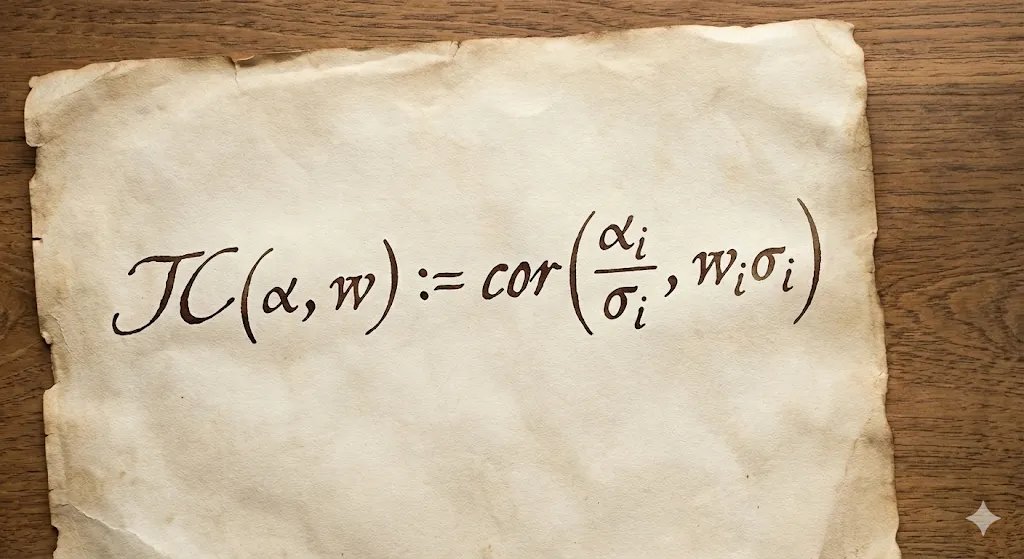

So: first, there is an introduction on the Information Coefficient. And also an intro to (Xsectional) quantitative investing using this concept. If you have bought my red book, you already know. This part connects to the Backtesting chapter over there.

So: first, there is an introduction on the Information Coefficient. And also an intro to (Xsectional) quantitative investing using this concept. If you have bought my red book, you already know. This part connects to the Backtesting chapter over there.

First, this is the quintessential "outsider" paper: academics (no slight intended) "looking into" a strategy run by traders. That's ok, although it is a few decades late and not very precise. This paper is the equivalent of seasons 7&8 of Game of Thrones.

First, this is the quintessential "outsider" paper: academics (no slight intended) "looking into" a strategy run by traders. That's ok, although it is a few decades late and not very precise. This paper is the equivalent of seasons 7&8 of Game of Thrones.

However, for an even more concise (free) introduction, Newman is very good.

However, for an even more concise (free) introduction, Newman is very good.