China research director for Gavekal Dragonomics. Aspiring blogger. Former Wall Street Journal. Places I've lived: Louisiana, Beijing, Pacific Northwest.

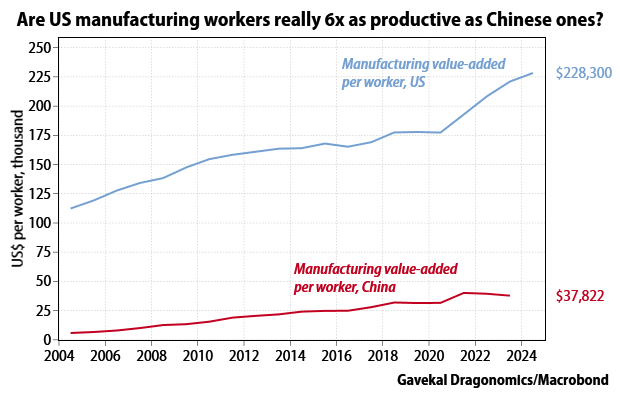

This means that on a per-worker basis, US manufacturing still looks insanely productive: each worker produces over $200,000 in value-added, while in China each manufacturing worker produces less than $40,000 in value-added. So the US still has a productivity edge. 2/

This means that on a per-worker basis, US manufacturing still looks insanely productive: each worker produces over $200,000 in value-added, while in China each manufacturing worker produces less than $40,000 in value-added. So the US still has a productivity edge. 2/

It's a good book, short and readable, mixing together the authors' personal experiences with the Chinese educational and the results of their long careers analyzing that system. For me it was eye-opening.

It's a good book, short and readable, mixing together the authors' personal experiences with the Chinese educational and the results of their long careers analyzing that system. For me it was eye-opening.

In its 2021 financial stability report, the PBOC ran banking-system stress tests based on various growth scenarios. In the worst one, the "severely adverse" scenario, it assumed 2.8% GDP growth in 2022. In other words, China is now actually in the severely adverse scenario.

In its 2021 financial stability report, the PBOC ran banking-system stress tests based on various growth scenarios. In the worst one, the "severely adverse" scenario, it assumed 2.8% GDP growth in 2022. In other words, China is now actually in the severely adverse scenario.

h/t to the Australian Financial Review for highlighting this interesting data

h/t to the Australian Financial Review for highlighting this interesting data