General Partner (FinTech/Enterprise/AI) @a16z, proud Canadian, mom of 2 boys, distance runner; Previous: product leader

Sep 20, 2024 • 4 tweets • 2 min read

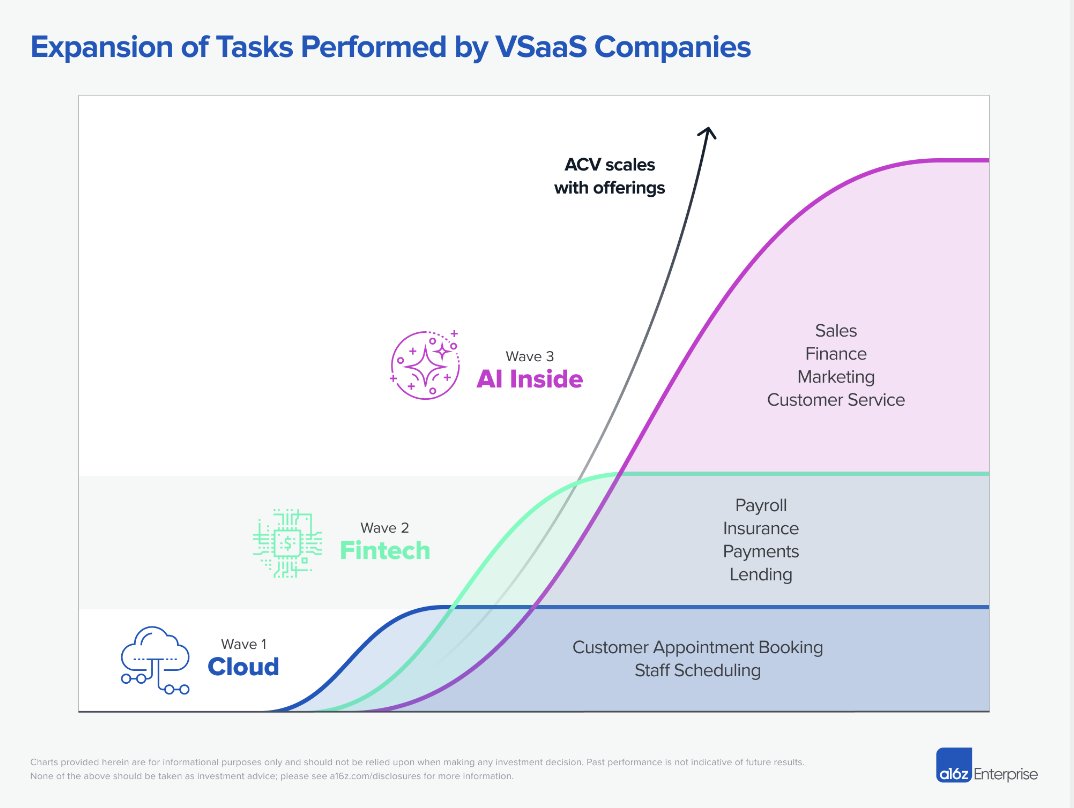

4 yrs ago we wrote: fintech scales Vertical SaaS, increases rev/customer 2-5x & opens new markets.

VSaaS - Now with AI Inside - is scaling once again. AI enables vertical SaaS companies to take on tasks previously too complex for software 🧠🧵👇

Evolution of VSaaS in 3 waves:

1⃣ Cloud🌥️, brought services online (e.g., Shopify for e-commerce, ServiceTitan for service workers)

2⃣ Cloud 🌥️+ fintech 💵, increased revenue by enabling VSaaS companies to embed financial services within their software offerings (Toast makes >80% of revenue from finserv)

3⃣Cloud 🌥️+ fintech 💵+ AI 🧠 expands the surface area of VSaaS by turning Labor into Software. This will be the most impactful product evolution to date!

Sep 21, 2023 • 12 tweets • 3 min read

1/ Software easily crosses borders-often just requiring language translation. Money also crosses borders- but w/ opaque FX rates & costly delays. We dive into who is solving these problems & opps for future. See #a16z global payment hub for a map & more! a16z.com/global-payment…2/ Companies today are "default global". They span multiple countries early on. But adding financial services can be extremely complex. Incumbents and entrepreneurs alike need cross-border infrastructure and full-stack solutions to simplify global expansion.

Mar 28, 2022 • 7 tweets • 3 min read

1/The logistics of starting a company in the U.S. are a mostly solved problem: Stripe Atlas for company formation, Mercury for business banking, Ramp/Brex for corporate cards, Carta for cap table management, Gusto for HR. Yet, just getting started in many countries is HARD 🧵

2/ In Brazil for instance, to form a venture backable company that can accept investment from US & Brazilian investors requires (busy and expensive) lawyers familiar with 3 countries (Brazil, Cayman, US) & often slow to open business bank accounts in both Brazil & US

Feb 10, 2022 • 5 tweets • 2 min read

1/ Every [fintech, crypto, marketplace, vertical SaaS] co is faced with a hard trade-off: let your newly recruited customers transact right away (great experience!), but accept potentially crippling financial risks:

2/ Risk category 1: Non-sufficient funds (NSF) - User transfers $$ to your wallet, you do a balance check to see if there are sufficient funds, but by the time your ACH pull request goes through--hours or even a day later--there may *not* be sufficient funds. You eat the loss.

Oct 15, 2021 • 13 tweets • 4 min read

1/ Open source will catalyze the financial services industry's biggest evolution to date. In this $25T industry, increasing power & influence will shift from suits to developers. future.a16z.com/open-source-fi…2/ For the developer perspective - my presentation at Fintech DevCon titled "from marble to code" which could have also been titled "Every Fintech company will spin out a Fintech infrastructure company"

Feb 18, 2021 • 5 tweets • 2 min read

1/ Why doesn't insurance just "come with" everything? Rental w. apartment lease, cyber w. domain name, pet w. dog etc. Instead, we buy the valuable thing, then go somewhere *else* to get insurance. New post w. @seema_amble on opportunities for startups bit.ly/3axjasM2/ More companies are realizing that by offering financial services, they can better retain their customers and increase revenue. Insurance is a big untapped opportunity. Why don't more platforms offer? Insurance is hard to build and hard to partner with. How could this change?

Apr 15, 2020 • 6 tweets • 3 min read

1) A strong finance team is critical, now more than ever. Companies of all sizes are dynamically planning for uncertain times ahead. New post w. @seema_amble:fintech & enterprise entrepreneurs are teaming up to modernize SW for the finance suite (finally!) a16z.com/2020/04/15/new…2) Finance teams spend the majority of their time gathering, scrubbing, synthesizing data from multiple systems (which is still often not available in real-time) - and only then can they provide strategic business advice

Jan 21, 2020 • 6 tweets • 2 min read

1) My presentation @ our annual @a16z Summit this year bit.ly/a16zFintech The "Amazon Web Services" era has arrived for financial services. Who benefits most? Consumers! -> more choice, better & more affordable products, regardless of geography or socioeconomic demographic

2) Similar to what AWS did for compute and storage, new infrastructure companies are rebuilding each layer of the banking stack and providing modern software “as a service.” Thus, the cost and complexity of building or adding financial services is coming down.

Nov 21, 2019 • 6 tweets • 2 min read

1) People hating banks is old news. It’s more interesting to look at root causes for the inertia. And more importantly, why is the centuries-old banking industry changing so suddenly? New post: Why our most hated institutions will become our most beloved bit.ly/37AGvpU2) What's unique about this disruption is that, rather than a single winner and many losers, all players stand to benefit. Incumbents will improve, it'll become faster to launch startups, and new brands that have nothing to do with financial services could become your bank!

Aug 12, 2019 • 8 tweets • 3 min read

1) The lack of a universally adopted real time payments system in the US is one of our largest regressive taxes. @sm90 and I discuss in the latest episode of @a16z 16minutes pod: a16z.com/2019/08/11/16m…2) Most employees live paycheck to paycheck and come dangerously close to 0 balance. With impossible to predict delays (in paychecks, $ from checks being available or cashed) - every mistake results in a $30 overdraft fee...adding to $34B in overdraft fees last year.