Feat 1: "Transforming" high risk, high funding to low risk, low funding.

Feat 1: "Transforming" high risk, high funding to low risk, low funding.

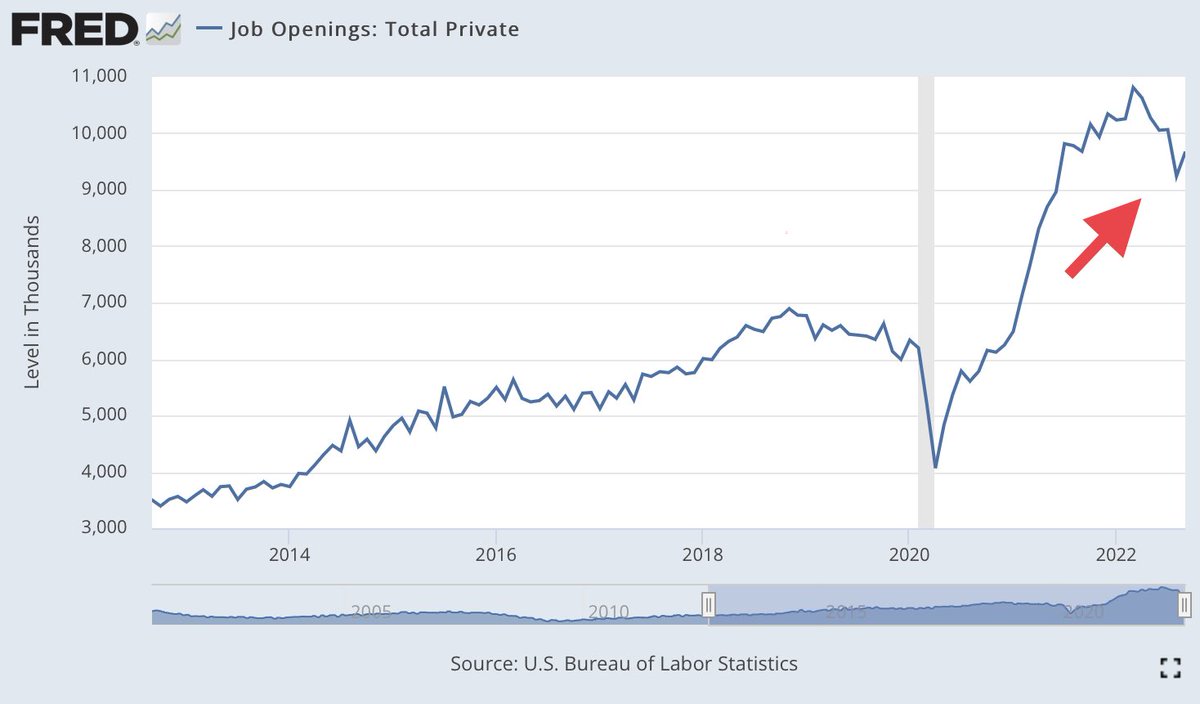

2. And yet, in spite of Fed hikes, job openings are near cyclical highs. Demand for workers outstrips supply.

2. And yet, in spite of Fed hikes, job openings are near cyclical highs. Demand for workers outstrips supply.