Investments & market insights 📈

Daily updates + my portfolio growth 💸

YouTube 🎥 https://t.co/dUuKweywva

2/

2/ 2/

2/ 2/

2/ 1/ $HIMS CEO Andrew Dudum compares $HIMS to early $AMZN and $NFLX —and he’s right.

1/ $HIMS CEO Andrew Dudum compares $HIMS to early $AMZN and $NFLX —and he’s right. 1/

1/ 1/

1/ 1. The Setup

1. The Setup 1/

1/ 1. The Setup

1. The Setup 1.

1.  1.

1. 1/

1/ 1.

1.

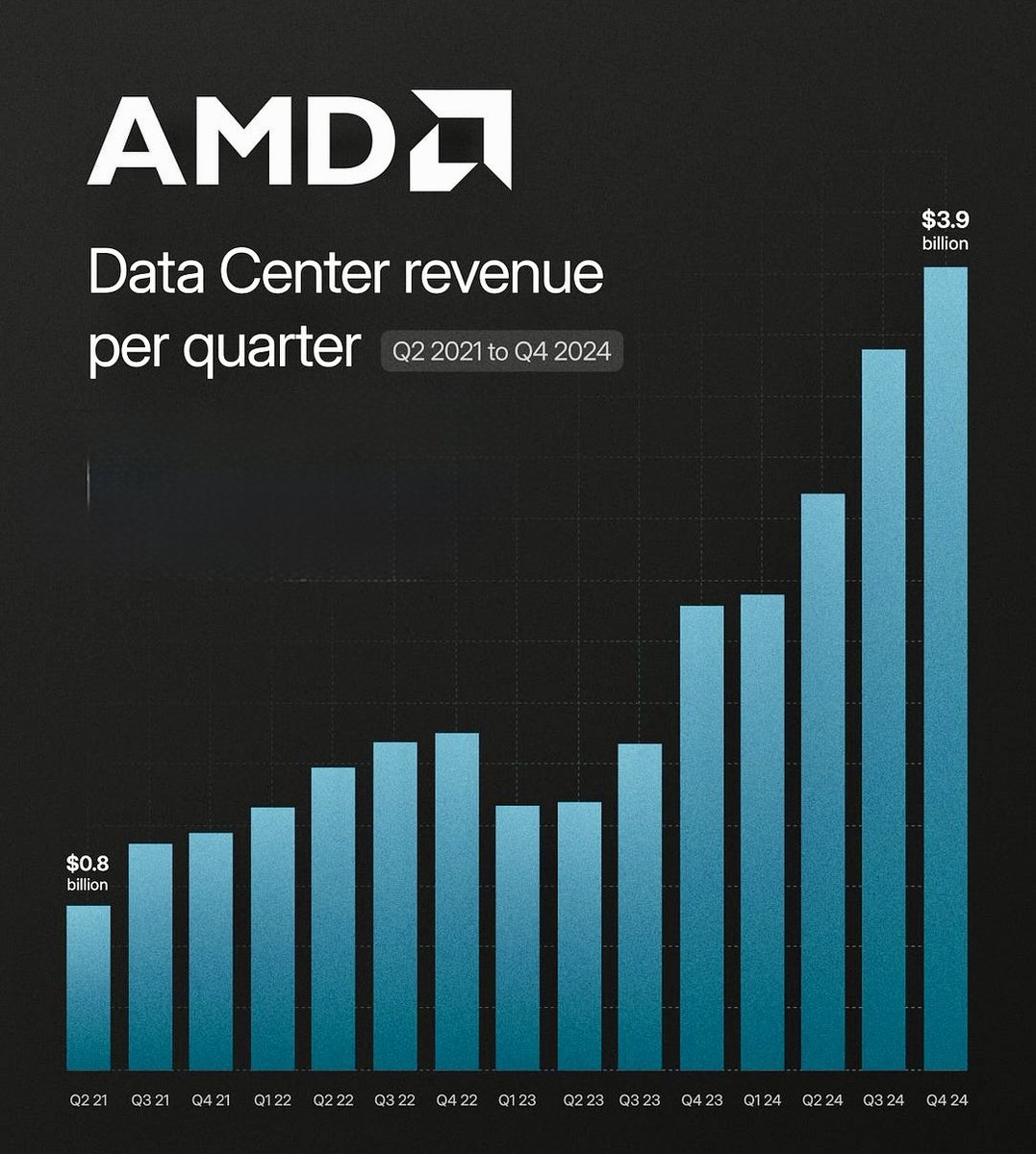

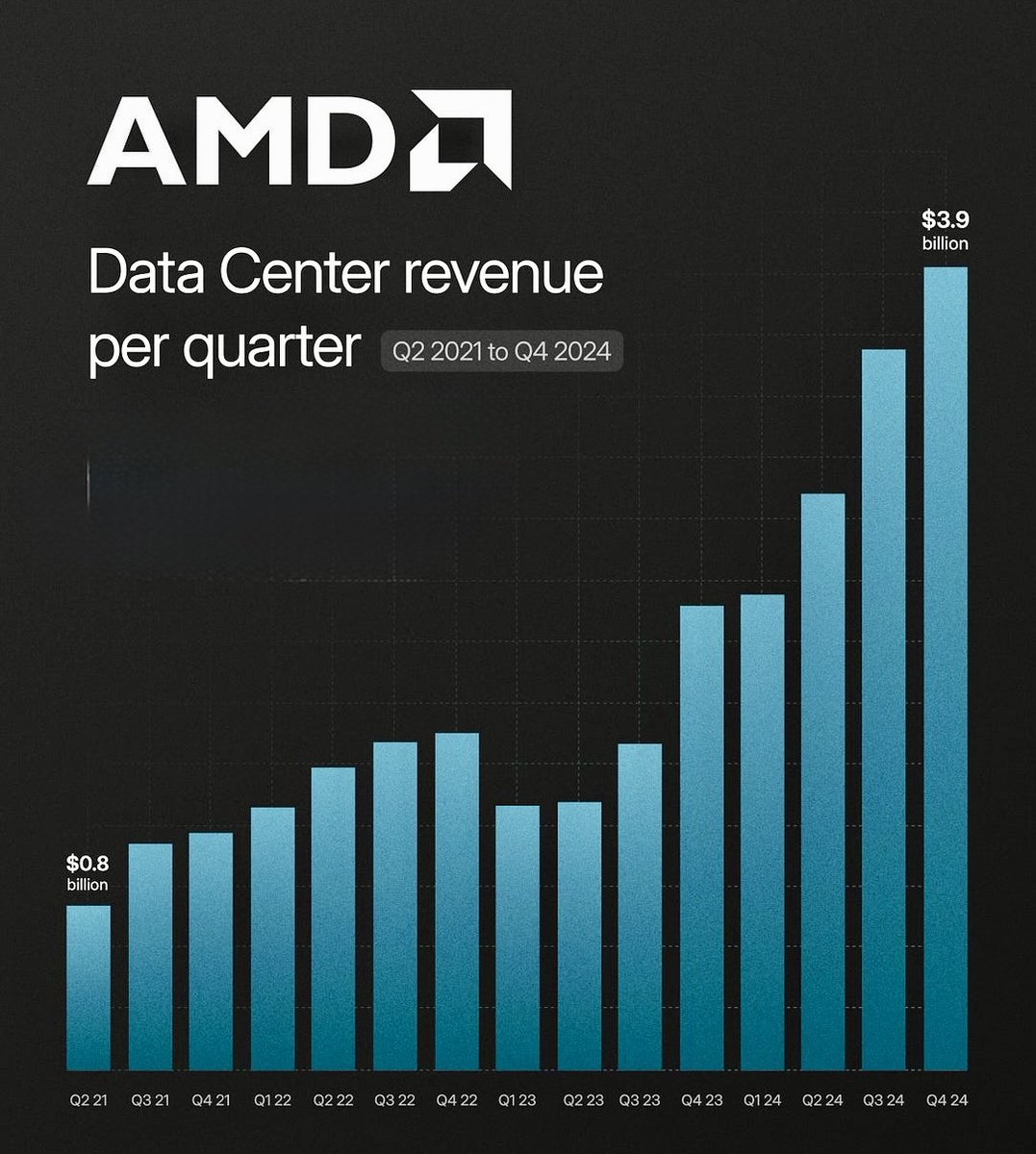

1/ In just 2.5 years, $AMD data center revenue grew nearly 5×, from $0.8B in Q2 2022 to $3.9B in Q4 2024.

1/ In just 2.5 years, $AMD data center revenue grew nearly 5×, from $0.8B in Q2 2022 to $3.9B in Q4 2024.