Adj. Prof. Financial Markets @ Unicatt, Milan.

Podcast: https://t.co/gltwX62e1g

All things Macro, Bonds.

Energy Specialist.

Ex Citi, ex UBM.

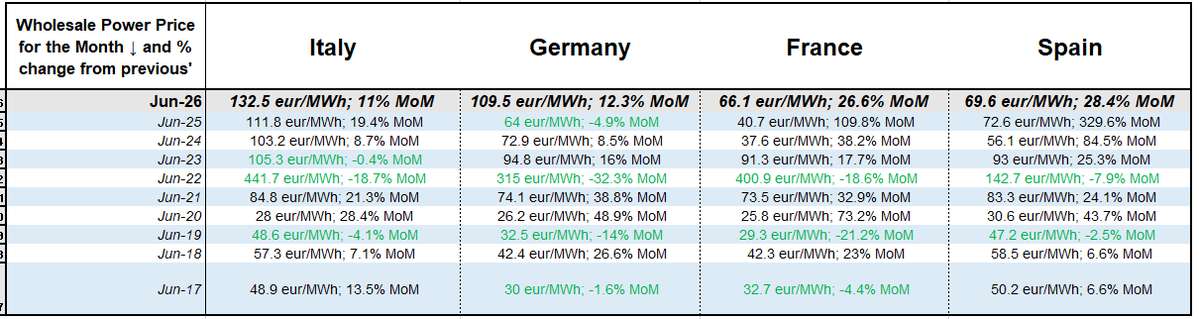

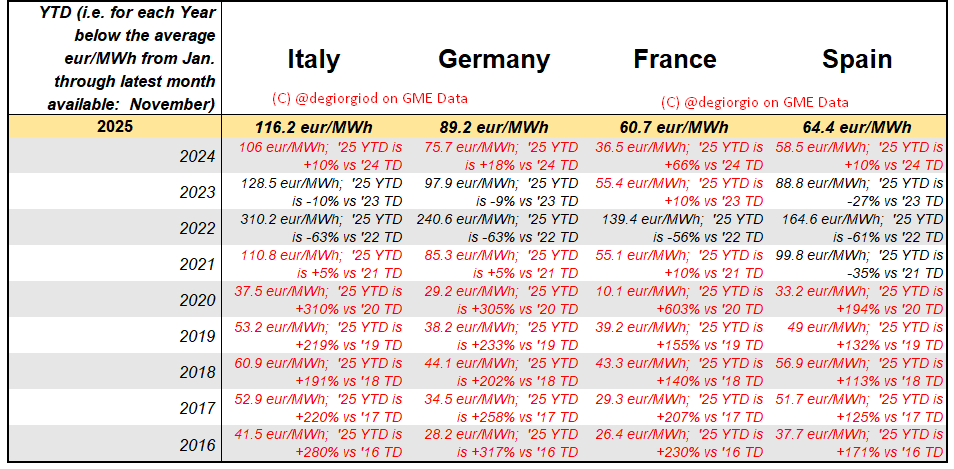

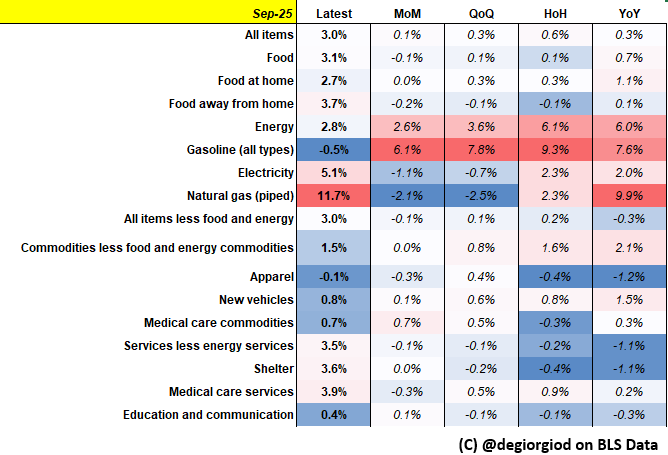

absolute terms in IT, DE (2nd-dearest June in 10yrs) and relative terms in both Spain (+28.4%MoM) and France (26.6% MoM).

absolute terms in IT, DE (2nd-dearest June in 10yrs) and relative terms in both Spain (+28.4%MoM) and France (26.6% MoM).

I appreciate a lot of commentators have been misled by headline prints over the past years - I blame them for their lame analysis.

I appreciate a lot of commentators have been misled by headline prints over the past years - I blame them for their lame analysis.

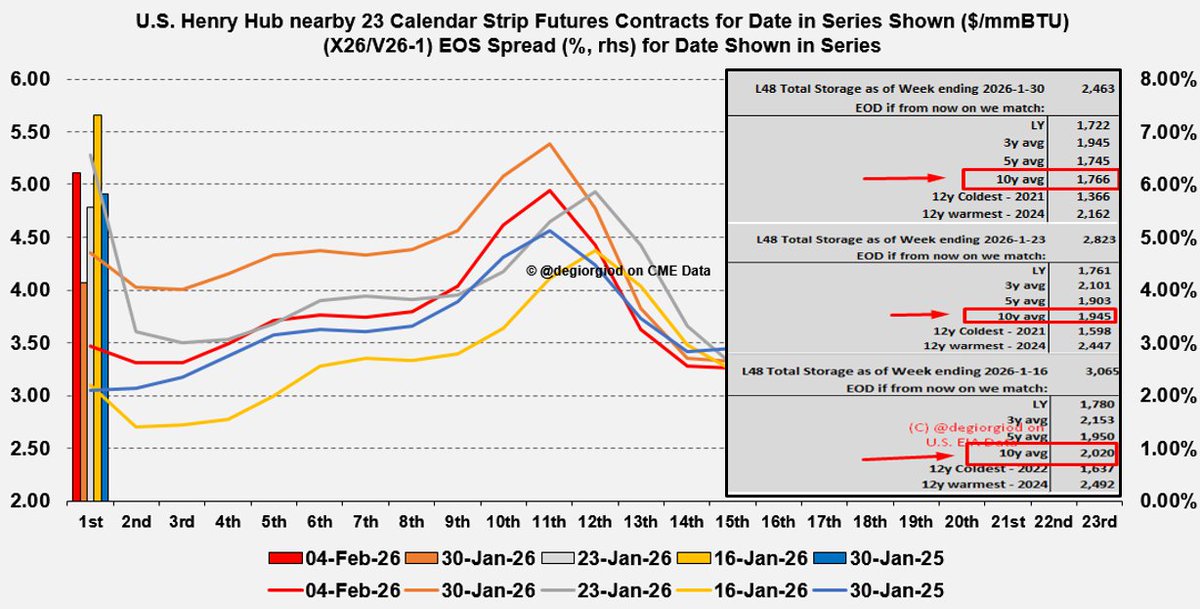

the military infrastructures of the all-important Iranian Oil Export terminal of Kharg Island, the focus of the interview was re-routed on the implications of this further development.

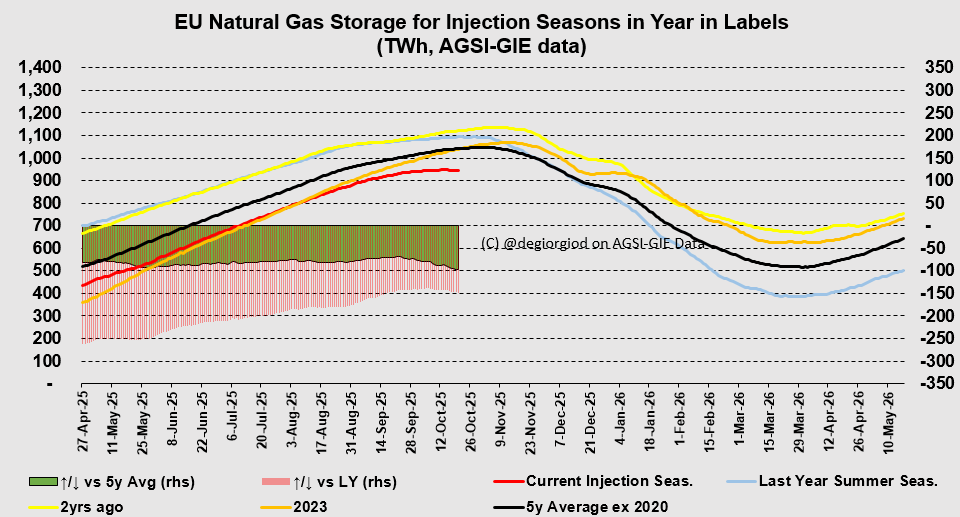

the military infrastructures of the all-important Iranian Oil Export terminal of Kharg Island, the focus of the interview was re-routed on the implications of this further development. 3. a grey box on the RHS of the chart, where I put my Storage model's levels for the last 3 EIA Reporting weeks and its EOD scenarios based on different assumptions of how the rest of the Draw Season may behave

3. a grey box on the RHS of the chart, where I put my Storage model's levels for the last 3 EIA Reporting weeks and its EOD scenarios based on different assumptions of how the rest of the Draw Season may behave we actually did.

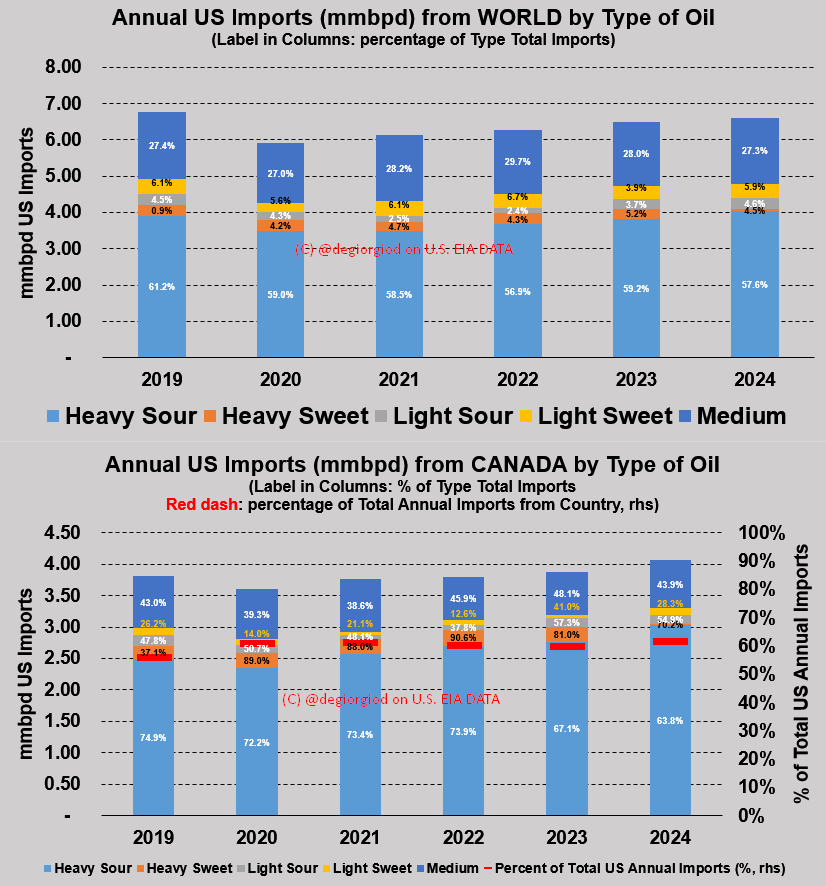

we actually did. anyone?), 60% of which (~4mmbpd) from Canada.

anyone?), 60% of which (~4mmbpd) from Canada.

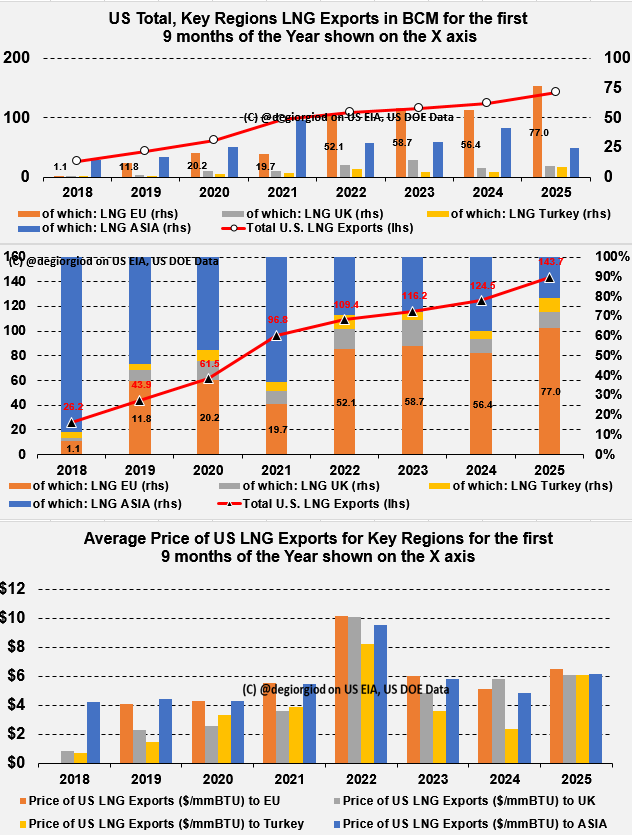

Dagli Stati Uniti (e *non* vuol dire che i venditori siano gli USA, ovviamente) son partiti 77miliardi di metri cubi di LNG per l'Europa, oltre il 60% dell'ammontare record (~144bcm) esportato nei primi 9 mesi del 2025.

Dagli Stati Uniti (e *non* vuol dire che i venditori siano gli USA, ovviamente) son partiti 77miliardi di metri cubi di LNG per l'Europa, oltre il 60% dell'ammontare record (~144bcm) esportato nei primi 9 mesi del 2025.

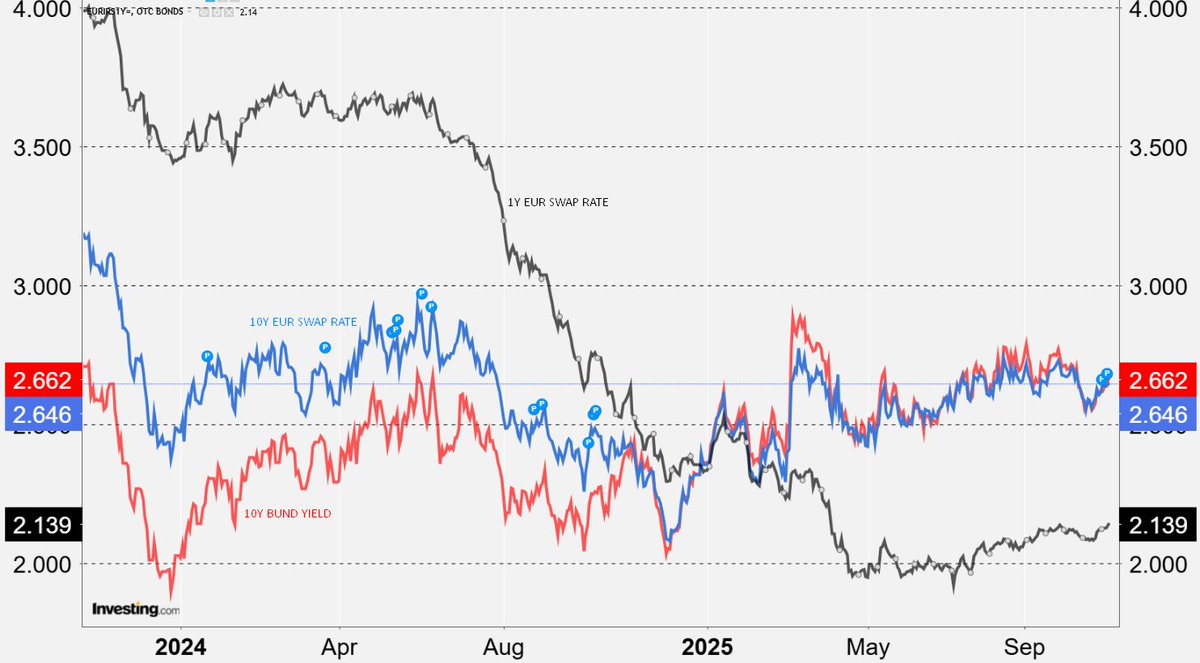

short-term Monetary Policy Action (its proxy here is the 1-year EUR Swap rate, black).

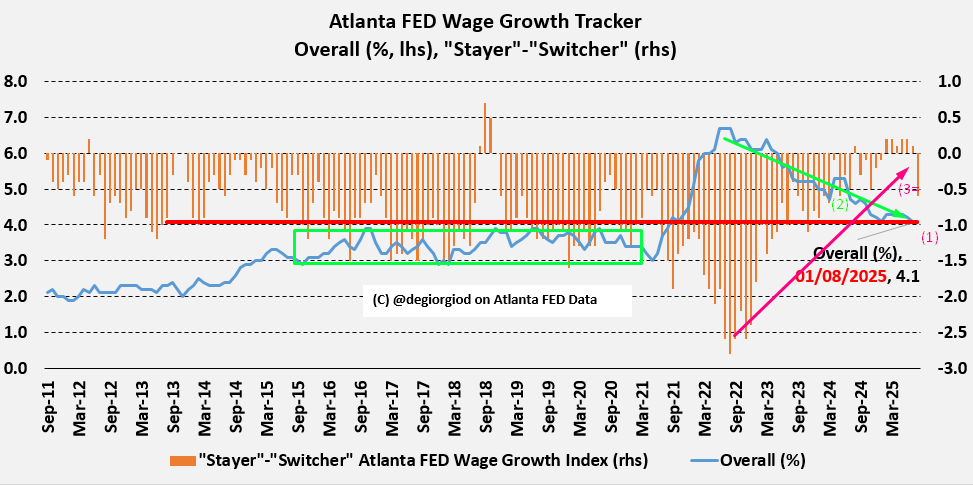

short-term Monetary Policy Action (its proxy here is the 1-year EUR Swap rate, black). a vibrant, dynamic Job/Salaries ecosystem where spending is solid and consistent with a lively (2) yet less hot wages/jobs set-up where Wages continue to clock @ 4.1% YoY (1), ~+0.5% more than pre-Covid era but with a clearly less tight (3) balance btwn Labour S/D as Stayers' 2/

a vibrant, dynamic Job/Salaries ecosystem where spending is solid and consistent with a lively (2) yet less hot wages/jobs set-up where Wages continue to clock @ 4.1% YoY (1), ~+0.5% more than pre-Covid era but with a clearly less tight (3) balance btwn Labour S/D as Stayers' 2/

Here's why:

Here's why: on November 5th, 2023).

on November 5th, 2023).

Things are frail already in Power-land...

Things are frail already in Power-land...

supine posture towards Washington in handling EU foreign affairs (see ↓) had alienated the only credible, usable, viable leverage in the hands of the EU and of its member states: trade, namely energy trade.

supine posture towards Washington in handling EU foreign affairs (see ↓) had alienated the only credible, usable, viable leverage in the hands of the EU and of its member states: trade, namely energy trade.