Have gotten a bunch of questions in DMs regarding how intrinsic value can change/increase over time...

Especially if a business is worth the present value of all future cash flows...

Here’s how I think about this (1/n)

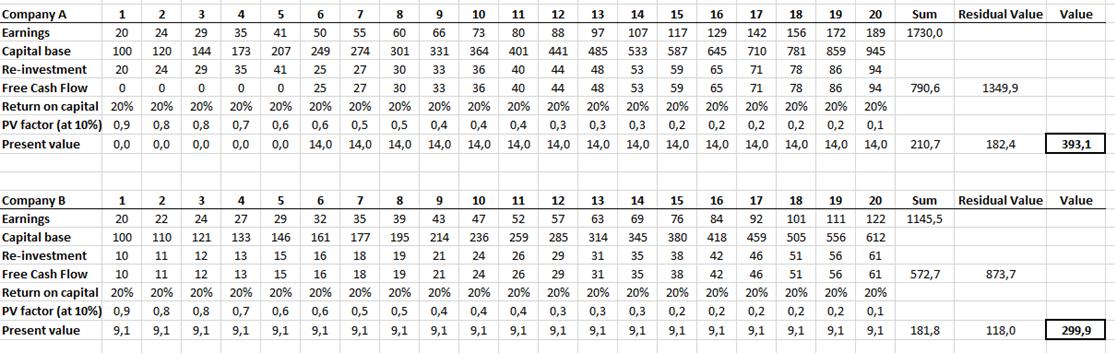

Indeed, intrinsic value is the PV of future cash flows. If investors had perfect foresight, there would be no changes in value. But they don’t...

IV increases either because future FCFs are higher than initially expected or they’re less risky. Each can be further broken down

Oct 6, 2020 • 29 tweets • 5 min read

(1/n) Value investing is about buying something for less than it’s worth. 2 problems with the implementation of this:

1/ People don’t have the same definitions/frameworks for thinking about what something is worth

2/ The worth of things changes over time, esp in dynamic markets

Relating to point 1, many investors equate ‘what it’s worth’ with a low multiple. This approach is decreasingly useful for various reasons

Investing has always been about a company generating more long term FCF than the market thinks (or with less risk than the market thinks)

Jul 5, 2020 • 5 tweets • 1 min read

I’ve thought about this a lot, and I think the answer depends in part on the type of competitive advantage.

For example, for economies of scale, there are various signs of it getting stronger that often depend on the type of customer benefit/value proposition

If better convenience or lower prices vs alternatives are the benefit via scale economies shared, then you want to follow customer value and pricing relative to peers, and you want to see the gap (as well as perception) widen or at least maintain vs peers. Costco is an example

Jun 21, 2020 • 56 tweets • 12 min read

A thread on things I’ve read over the years that have resonated with me, influenced my investing & made me rethink things. Will add to it over time

(Didn’t include the names of authors, so you can judge the passages based on their own merits)

Some of the topics include...

- Creative & Independent thinking

- Change

- Quality

- Mispricing & Expectations

- Valuation

- Patience

- Portfolio management

Jun 12, 2020 • 26 tweets • 4 min read

(1/n) Have been seeing quite a few of these types of questions recently: what stocks would you never sell?

To me, that begs the question: what would you need to see to make you confident that you wouldn’t need to sell a stock for a decade or two?

If you bring it back to first principles, you need a strong probability that the company will continually surpass expectations (not necessarily linearly) over a long period

What are some of the things that cause companies to continually surpass expectations?

Nov 29, 2019 • 13 tweets • 7 min read

A week ago I asked for some interesting investing follows that think creatively. Here are some of my thoughts…

I like this quote:

'Knowledge has become much more commoditized because of greater transparency and more training. To get a real alpha edge, you have to go from knowledge to insight. To do that, you need imagination; you get paid for imagination' - Michael Hintze

Oct 22, 2019 • 6 tweets • 1 min read

Ask yourself a simple question: what do investors that hold stocks for 10/20/30x returns (or more) have in common?

It’s a question I have wondered about because I haven’t been able to do this. So I’ve been asking the investors I know that have been able to

The conclusion I’ve come to is that almost none of them use multiples. But all of them have some way to determine & follow expectations...in some cases with sell side expectations, in some cases reverse DCFs, in some cases it’s intuitive. It’s almost always explicit vs implicit

Oct 11, 2019 • 14 tweets • 2 min read

I often ask for book/paper recommendations. In the hopes of getting a conversation started & finding new books, I’ll share some of my investing related favorites by topic (that I haven’t seen recommended much)...

On Critical Thinking

-Critical Thinking by Paul & Elder

-Your Deceptive Mind by Novella

-The Psychology of Intelligence Analysis by Heuer

-A More Beautiful Question by Berger

-Asking Essential Questions by Elder

-How Life Imitates Chess

Oct 4, 2019 • 20 tweets • 3 min read

Some things that have helped me improve vs the traditional 'value investor' I was 15 years ago. Two categories: quality & contrarianism

On quality: spend more time on direction vs width of comp advantage...

Spend more time on differences in operating model (or business model) and nuanced patterns associated with high returns (example small % of customer costs but mission critical) vs general 'moats', ie spend more time on the actual operating intricacies

Aug 2, 2019 • 18 tweets • 3 min read

There’s lots of discussion on twitter regarding competitive advantage, growth/quality etc. I’ve learned a lot from it.

There is much less on mispricing. Would be interested in starting a discussion on this...

Going back to first principles, why do things become mispriced?

In my experience, there are mainly 2 reasons:

- investors are missing something (analytical, informational)

- investors are exaggerating something (behavioral)

Almost all of the reasons behind mispricing fall into one of those two buckets (although there are multiple forms)

Jul 5, 2019 • 43 tweets • 9 min read

This summer, it'll be nearly 20 years since I started playing guitar. Mostly Jazz & Blues, but also Folk & Bluegrass.

Of all the things I've learned, two really stand out as the biggest drivers of improvement. They both have interesting applications to investing...

In guitar soloing, there's a trend towards memorization vs understanding. People memorize scales instead of trying to understand why certain notes sound good in a given context. This is a mistake

Jun 28, 2019 • 6 tweets • 1 min read

Am currently reading ‘The MVP Machine’. Very interesting book that has lessons for investing. The ‘Moneyball’ approach in baseball involved buying ‘statistically cheap’ players. But because they became easy to identify quantitatively, the process was quickly copied...

This somewhat removed the inefficiency. A better approach began to take form: find players that have the potential to be much better if developed properly, but that don’t ‘screen well’ initially...

Jun 7, 2019 • 13 tweets • 3 min read

A company's value is driven by one thing: risk adjusted cash flows

This depends mainly on:

-Growth

-ROIC

-Cost of capital

Outperformance requires anticipating revisions to cash flow estimates. If high returns (& growth) are maintained, there are likely to be revisions higher

To understand this deeply, it’s important to disaggregate cash flow into growth & ROIC, to see how they're linked