$345M in free cash flow.

$1.18B in cash (67% of market cap).

7 insiders bought in the last 90 days.

I read every earnings call. Here’s what I found.

Chewy trades at 20x FCF.

Roku trades at 22x.

Sonos at 10x.

Peloton trades at 5x.

Same playbook:

hardware → subscription → cash flow.

The market is pricing it like it’s broken.

Jan 30 • 4 tweets • 1 min read

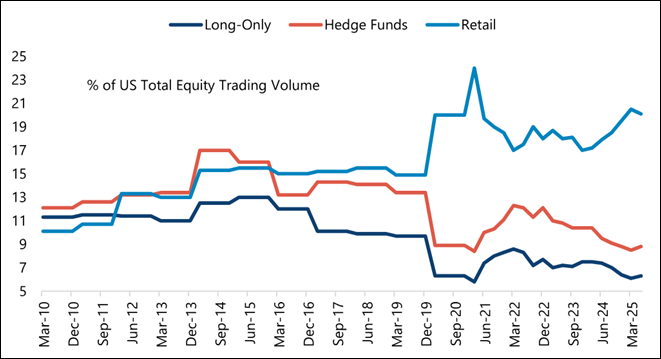

Retail isn’t a side show anymore — it is the market.

That’s why this cycle moves faster, breaks harder, and turns sharper.

This chart matters more than any earnings headline.

Retail is now ~20%+ of total US equity volume — structurally higher than any prior cycle.

That changes how selloffs behave.

Jan 29 • 6 tweets • 1 min read

Yesterday told you more about the AI vs software shift than a dozen earnings beats.

SAP sold off.

ServiceNow was “good, not good enough.”

Different companies.

Same signal.

The market is repricing how value is created in the AI era.

Legacy software is still growing.

That’s not the problem.

The problem is that AI compresses time:

• Shorter contracts

• Faster deployment

• Less backlog visibility

Backlog was king in SaaS.

Throughput is king in AI.

Different scorecards.

Jan 29 • 7 tweets • 1 min read

META, MSFT, TSLA earnings all say the same thing in different ways.

This is not a peak-capex moment.

This is commitment.

The market keeps confusing margin pressure with strategic dominance.

That’s the mistake.

META is the cleanest example.

Yes, opex and capex are huge.

But revenue is accelerating through the spend.

That tells you demand is pulling supply forward, not management forcing spend.

Platforms don’t slow investment when returns are showing up early.

Jan 28 • 7 tweets • 1 min read

Everyone is staring at headlines.

The real story this morning is AI demand locking in, not peaking.

ASML, STX, TXN, Anthropic, RDDT — different parts of the stack, same message:

Customers are committing years forward.

That’s how power-law cycles actually begin.

ASML said it plainly:

“Customers now have a notably more positive medium-term outlook… reflected in a marked step-up in capacity plans and record orders.”

Read that again.

This isn’t sentiment. This is capex pulled forward into 2027+.

Bottlenecks don’t lie.

Jan 27 • 6 tweets • 1 min read

Everyone’s buzzing about Clawdbot.

My take:

the frenzy is overdone — but the direction is real.

Those are very different statements.

Here’s the distinction most people are missing:

Clawdbot isn’t a product.

It’s a preview.

An always-on, context-aware AI agent logged into your apps will exist.

But what’s going viral now is a fragile prototype, not a stable system.

The setup alone should give serious users pause:

– deep OS permissions

– app-level credentials

– message + email access

– no real governance layer

Jan 27 • 12 tweets • 2 min read

The market still thinks $BETR is just a mortgage lender.

That’s the misprice.

BETR is quietly turning the mortgage stack into software.

Mortgages are one of the last massive consumer workflows still run like it’s 1999:

Manual

Siloed

Slow

Expensive

Perfect conditions for AI to take share.

Jan 23 • 12 tweets • 2 min read

Most corporate treasuries are fragile for one simple reason:

They confuse stability with safety.

Cash looks stable.

Single-asset treasuries look “conviction-driven.”

Both break in regime shifts.

Antifragility doesn’t mean “more risk.”

It means benefiting from uncertainty instead of being crushed by it.

That requires uncorrelated convexity—not leverage, not bravado, not narratives.

Jan 23 • 13 tweets • 2 min read

Friday.

LaGuardia.

Trying to beat a snowstorm back to Toronto.

Perfect moment to explain why most “AI + crypto” systems eventually fail.

Everyone obsesses over models.

Signals.

Predictions.

Backtests.

That’s only one leg of the stool.

Jan 21 • 7 tweets • 1 min read

.@nic_carter nailed the core issue with X:

The platform can’t decide whether it’s optimizing for attention or ownership.

You cannot serve both at the same time.

Here’s the deeper frame:

X quietly abolished digital property rights.

Followers used to be your land.

Now they’re just leased attention, revocable by the algorithm.

Jan 21 • 7 tweets • 1 min read

The hardest part of investing isn’t picking the stock.

It’s buying it when the story looks dead.

In 2022, crypto wasn’t just down.

It was declared over.

FTX. Bankruptcies. Endless headlines calling it a fad. Justin Trudeau making fun of it.

Most people capitulated.

Jan 18 • 25 tweets • 2 min read

I want to tell a real investing story that still bothers me. Not because I was wrong. But because I was right and still failed. Thread.

In Nov 2020 I bought a Canadian company almost everyone thought was uninvestable.

Jan 16 • 12 tweets • 1 min read

Real question:

Why do politicians talk endlessly about “net zero” when almost no normal human being ever brings it up in real life?

Nobody at the grocery store is discussing “net emissions pathways.”

Nobody at the gas pump is debating “scope 3 offsets.”

Yet it dominates political speeches.

Jan 9 • 8 tweets • 2 min read

A move in mortgage rates from ~6% to ~5.6% doesn’t sound dramatic.

But Morgan Stanley now estimates that shift alone expands mortgage originations from ~$2.4T to nearly $3T.

That is a ~25% volume shock hiding inside a 40bp move.

Here’s the key stat most investors gloss over:

Every ~50bps drop in mortgage rates pulls ~$1T of mortgages back “in-the-money.”

That’s not theory. That’s millions of households crossing an affordability threshold.

Jan 9 • 15 tweets • 2 min read

Yesterday the US government quietly changed the rules of the housing market.

Mortgage rates are no longer just “the market.”

They are now a policy lever.

That matters more than today’s price action.

When Donald Trump announces $200B of mortgage bond buying, that is not stimulus theater.

That is an admission that housing liquidity is systemically important.

Jan 8 • 12 tweets • 1 min read

Most people think credibility comes from branding, credentials, or being loud.

It doesn’t.

Credibility is a lagging indicator of visible asymmetric outcomes.

One undeniable win changes how the world treats you. (Ask Mark Cuban or Kevin O'Leary.)

Ten explanations never will.

Markets don’t reward effort.

They reward resolved results.

Jan 8 • 11 tweets • 2 min read

Everyone heard NVIDIA’s CES keynote.

Very few understood what it confirmed.

We are no longer in an “AI training cycle.”

We’ve entered the AI factory era.

The bottleneck is no longer intelligence. Open models are good enough.

The bottlenecks now are: – inference – uptime – throughput – power – memory – networking

That’s infrastructure, not software.

Jan 7 • 10 tweets • 1 min read

Goldman quietly made an important point this week:

2026 upside may be real — but leadership is fragmented, so convexity matters more than conviction.

That’s a condition.

Rising Dynasty supplies the response.

Most people hear “buy calls” and do the wrong thing:

Why the NVIDIA CES + JPM conversations quietly changed the outlook for AI power stocks

Most people watched NVIDIA’s CES keynote and heard “faster chips.”

That wasn’t the message.

The real takeaway was this:

AI factories are now being planned years in advance — at the land, power, and shell level.

At JPM’s CES fireside, NVIDIA confirmed something important:

Customers are already planning 2027+ data centers around Rubin-era systems. Not next quarter. Not next year. Multiple years out.

That’s not a bubble signal. That’s infrastructure planning.

Jan 6 • 14 tweets • 2 min read

There’s a predictable pattern every time real geopolitics collides with ideology.

Over the weekend, the same voices erupted in outrage over Venezuela, anchored to two familiar complaints:

1.“International law”

2.“This was just about oil”

First: international law.

What exactly is “international law” in practice?

Who enforces it?

Who has ever changed a consequential geopolitical decision because of it?

Jan 4 • 14 tweets • 2 min read

Mark Carney, like Justin Trudeau before him, likes to say “Canada is an AI superpower.”

Saying it does not make it true.

Systems do.

Let’s start with the uncomfortable fact pattern.

Some of the most important minds in modern AI are Canadian by training and lineage.

They all chose to build elsewhere.