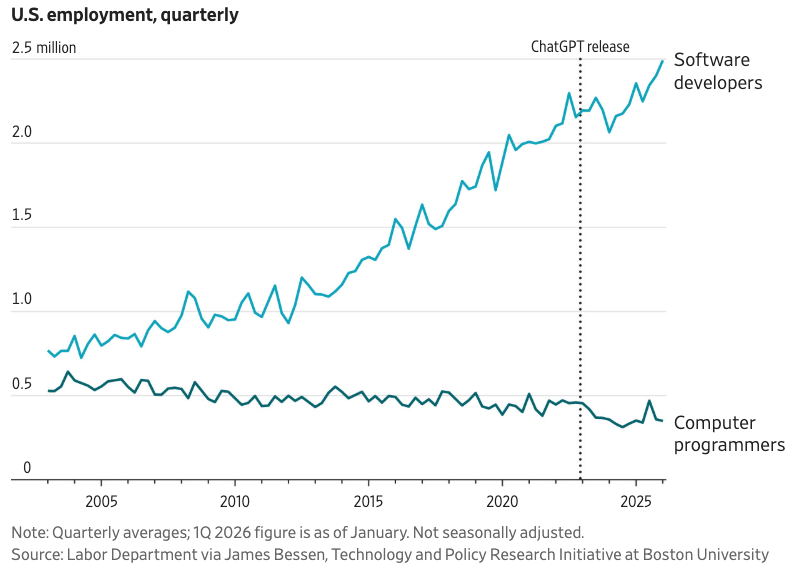

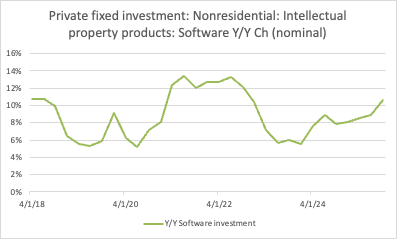

2/ Here's another: nominal business investment in software is accelerating (this incorporates developer salaries). This suggests software demand is elastic: as the price drops, demand rises even more. (Jevons paradox?)

2/ Here's another: nominal business investment in software is accelerating (this incorporates developer salaries). This suggests software demand is elastic: as the price drops, demand rises even more. (Jevons paradox?)

2/ This confirms what I have long suspected: Chinese growth does not "contribute" to global growth except in the purely arithmetic sense. It does not actually create positive feedbacks that lift other countries' growth. That's by design...

2/ This confirms what I have long suspected: Chinese growth does not "contribute" to global growth except in the purely arithmetic sense. It does not actually create positive feedbacks that lift other countries' growth. That's by design...

2/ Spears and Geruso don't invoke the usual risks of falling population such as a smaller labor force and more pressure on Social Security. Rather, they argue a larger, or stable, population is a good thing in and of itself.

2/ Spears and Geruso don't invoke the usual risks of falling population such as a smaller labor force and more pressure on Social Security. Rather, they argue a larger, or stable, population is a good thing in and of itself.

2/ Real home prices and price/income ratios aren't good valuation measures when real cost & quality of shelter is rising. Price to rent ratios are superior because owning and renting are close substitutes. So rents up 24% v. prices up 51% since 2019 is a big red flag.

2/ Real home prices and price/income ratios aren't good valuation measures when real cost & quality of shelter is rising. Price to rent ratios are superior because owning and renting are close substitutes. So rents up 24% v. prices up 51% since 2019 is a big red flag.