Nothing here is MNPI. Not investment advice. Compliance officers are super fun at parties.

Feb 12, 2021 • 27 tweets • 6 min read

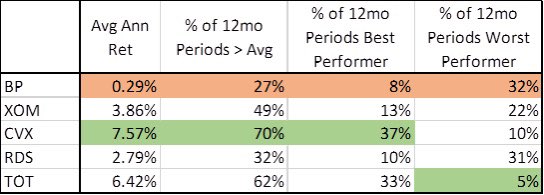

Ok it’s time for the $BP thread. I will demonstrate that BP is a terrible company to interact with in any way, whether you work there, doing business with BP, or (heaven forbid) are a shareholder. I’ll try to organize this in a logical faction.

From an employee perspective, your first concern should be safety. Between 2007-2010, BP refineries in TX and OH accounted for 97% of “egregious, willful” violations issued by OSHA. This is while BP operated only ~8% of total US capacity. In other words, BP facilities were

Sep 29, 2020 • 11 tweets • 3 min read

As promised, a thread on renewables and why they can’t work (as is). First of all, it’s important to understand there are 2 types of power production: base load & peak load. Base load is the min power demand throughout the day, & peak load take the fluctuations thru the day

1/

Natural gas power plants can adjust to fluctuations in demand, and gas peaker units are able to kick on and produce incremental power for just a few hours a month when prices make them economical. The problem with renewables (wind and solar) is there is no way to increase.

2/

Aug 19, 2020 • 7 tweets • 2 min read

Why Katie is everything wrong with the world: a thread.

1. Katie’s prevalence include EFT stemmed from her blind support of Vicki Hollub. She framed all criticism as gender-based (try selling that one to Holly, Suttles, HammBone, Gallagher, Sheffield, etc). In the end, EFT was right. It was an awful deal and resulted in huge

1/

Aug 16, 2020 • 8 tweets • 2 min read

For all the new #EFT members:

A primer on E&P investing:

1. A long only strategy in E&P companies IS a commodity bet. Long term shale co-WTI return correlations sit 35-60%. A long shale strategy requires a bullish oil thesis.

2. The basis of this is the business model.

1/

There is no sustainable advantage in E&P. The companies are price takers in a volatile, capital-intensive market.

3. The companies are simply an aggregation of assets. Each well has a type curve. Model type curve, find your required discount rate, and you get the value of

2/

May 2, 2020 • 7 tweets • 2 min read

Thread 1/n

What happened in energy private equity is pretty simple. It started out with solid returns and providing needed capital to people too small for public markets. These were the “good guys.” They helped small-time oilmen de-risk their wealth and grow

2/n

But the fee structure is such that moar = better. So endowments/pensions/other inst. money see this nice return, and they develop a “private equity natural resources” allocation. Now all the energy PE guys aren’t competing against all other capital destinations,

Feb 5, 2020 • 6 tweets • 1 min read

While I largely believe E&P’s deserve to be where they’re at, I think there are decent cases for why $50 WTI can’t work. Particularly with cap markets largely closed off to shale, you either live within CF or die. Anonymous surveys of shale co’s show

1/

that all the $30 and $40 oil has been pulled out, albeit at $65 breakeven when oil was at $90. There is a huge inventory build coming from Coronavirus effects, but all in all, I see a lot of upside for oil. With decline curves steeper than ever, industry should be becoming

2/

Feb 5, 2020 • 4 tweets • 1 min read

Let’s play guess the legend #EFT#flaring

***data from EIA and only runs through 2018

It’s state-by-state for big flarers, with offshore counted as a state, and rest of US lumped together