My mission is to spread financial wellness. Email: admin@gichukikahome.com WhatsApp: +254793410596

Jun 5 • 7 tweets • 3 min read

5 NSE stocks we're BUYING this June.

- Two banks trading below book.

- A beverage giant mid-re-rating.

- An insurer hiding behind a high price tag.

- And a small-cap with 90%+ upside.

Our Wealth Atlas calls for June 2026👇🧵

1/ Car & General

The bear case is "FY25 was a one-off."

But CEO Vijay Gidoomal's post-results guidance says otherwise:

Kenya's two-wheeler market is set to recover to 14–15k units/month in 2026, up from 8k in FY25 (peak was 20k) — a named, quantified catalyst, not a hope.

And Tanzania, now the largest market at 49.7% of revenue, has already passed its prior peak, putting a structural floor under earnings.

That's why we model FY26E EPS of KES 38.6 — yet the stock trades at just 2.05x it. A grower with explicit forward guidance shouldn't sit this cheap.

Jun 3 • 16 tweets • 4 min read

There are three funds that every investor should have:

1/ An Emergency Fund

2/ A Sinking Fund

3/ A Run Away Fund

Here's what they are and how to create them👇

1/ An Emergency fund.

What is it?

This is a set amount of money that covers your daily expenses for a certain period of time.

It should cover your daily *normal* expenses for a period of 3-6 months.

Jun 1 • 8 tweets • 3 min read

SpaceX is IPO-ing on June 12 at a $1.75T valuation.

The largest listing in history: bigger than Saudi Aramco's $29.4B raise in 2019.

🧵 A thread on the SpaceX IPO, what it's really worth, and the best way to get exposure before June 12.

SpaceX is three distinct businesses:

→ Space (launch + Starship R&D): $4.1B revenue, FY2025

→ SpaceXAI (terrestrial + orbital AI compute): $3.2B revenue, scaling fast

Total FY2025 revenue: $18.7B — up 33% year-on-year.

May 21 • 19 tweets • 5 min read

Most Kenyans keep their savings in a money market fund and call it "investing."

There's nothing wrong with that, but if you want real wealth building, you need to own a piece of Kenyan businesses.

Here's how to build a serious stock portfolio on the Nairobi Securities Exchange. 🧵

1. How should you structure your portfolio?

First, think of your portfolio in three buckets:

a) Anchor stocks - these should represent 50–60% of your portfolio

They should include stable, blue-chip companies like Safaricom, Equity Group, KCB.

These are stable, profitable, and market leaders in their respective industries.

May 20 • 15 tweets • 4 min read

You are the greatest asset in your financial life.Remove you — and everything collapses.

A thread on why protection comes before investment 🧵

Every day you wake up and produce.

Your income funds your lifestyle, educates your children, supports your family, and carries your dreams.

But here's the hard question most people avoid:

What happens to everything you've built… when you can no longer produce it?

May 20 • 9 tweets • 3 min read

If I was a beginner investor who just started investing in the NSE,

Here’s how I would invest KES 500K in the NSE today

Portfolio breakdown below👇👇

1. Which platform I’m I using to invest?

The newly launched Ziidi Trader by Safaricom on the “My One App” is easy to get started as it only takes a few seconds for you to get started

And also is cost effective as it is cheaper compared to other stock brokers and there are no charges when moving your money from your Mpesa wallet to the Ziidi Trader platform.

I've seen so many people here saying they've already liquidated — or are planning to liquidate — their NSE positions ahead of the 2027 elections.

Here's why that may not be the smartest move. 🧵👇

First, let's address the elephant in the room: does the NSE actually crash during election years?

The data will surprise you.

The NSE All Share Index has been positive in 2 of the last 3 electioneering periods:

📈 2012: +40.4%

📈 2017: +28.4%

📉 2022: -23.4%

And that 2022 drop?

The Russia-Ukraine war tanked global markets that year — the S&P 500 was also down 18%.

That wasn't a Kenya story. That was a world story. Equities tanked globally, not only in Kenya.

chart credit @kenyanwalstreet

May 17 • 6 tweets • 2 min read

Your employer's group life cover is not enough.

Here's why you should get a personal whole life cover separate from your employers' group life cover👇👇

Group life cover through your employer ends the day your employment does.

Resign. Retrenchment. Company closes down. You retire.

In any of these scenarios your cover disappears with your job.

You are left completely unprotected.

May 10 • 9 tweets • 3 min read

The NSE is full of noise.

But right now, there are 5 stocks with real fundamentals, real upside, and in some cases — dividends about to hit your account.

Here are the top 5 stocks I'd buy on the NSE this May.

A thread.🧵

Before we get into the picks — a quick framework.

We look at 3 things:

1. Is the stock undervalued vs. its earnings power? 2. Is there a near-term catalyst (dividend, results)? 3. Does the risk-reward make sense at current prices?

Every pick below passes all three. Let's go.

May 10 • 12 tweets • 4 min read

Here's how smart families are using whole life insurance to protect their wealth and that of their families.

Breakdown below👇

Smart parents understand that financial planning has 3 critical stages:

a) Wealth Creation — This involves buying assets and building good portfolios.

Think stocks, bonds, real estate, business. Building assets. Your goal is to growth your networth

b) Wealth Protection — This is where you protect yourself and your family from any eventualities in life. Insurance that protects against death, critical illness, permanent disability.

c) Legacy Planning — wills, trusts, succession planning.

Most of us only focus on the first step. But if something happens to you before steps 2 and 3 are in place...

All that wealth you worked so hard to build could go to waste. Or worse — spark conflict.

May 8 • 13 tweets • 4 min read

🧵 THREAD:

How to use a Whole Life Insurance policy to replace your income & protect your family's cash flow

Read this especially if you have children or dependents.

1/ Let me start with an uncomfortable truth that most people avoid thinking about.

If you died tomorrow, what happens to your family financially?

Not emotionally — we know that's devastating. I mean practically. Who pays rent?

Who pays school fees? Who puts food on the table?

Most families in Kenya are one funeral away from financial collapse. That's not dramatic. That's reality.

May 6 • 4 tweets • 2 min read

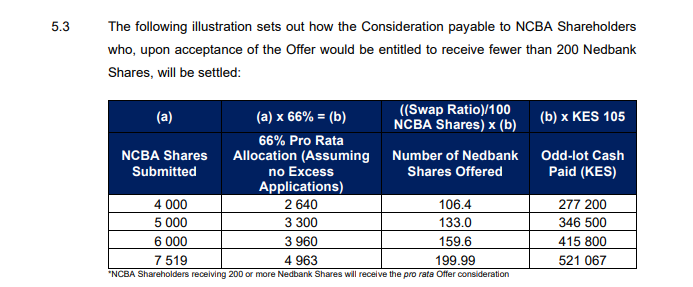

About the Ned bank - NCBA deal, there's something that many people are getting wrong.

What's the maximum NCBA shares you need to own for you to qualify for the full cash payout of KES 105?

It's not 4500, 5000, 7400, 9400, etc

The correct figure is 7519 NCBA shares

The offer document says that shareholders who would receive fewer than 200 Nedbank shares upon tendering their 66% entitlement shall be paid entirely in cash at KES 10,500 per 100 NCBA shares (= KES 105 per share) instead of the standard 80% NED shares / 20% cash mix.

Working backwards from the exchange ratio of 4.02994 NED per 100 NCBA shares tendered:

To receive exactly 200 NED shares:

200 ÷ 0.0402994 = 4,963 NCBA shares tendered. Since you can tender a maximum of 66% of your holding:

4,963 ÷ 0.66 = 7,519 shares total holding.

The KES 105 all-cash alternative therefore applies ONLY to shareholders holding fewer than approximately 7,519 NCBA shares in total.

Holders of 7,520 or more shares receive the standard KES 98.72 equivalent (80% NED + 20% cash).

(See image below that confirms the same in the offer document)

May 4 • 14 tweets • 7 min read

Two bonds are live in Kenya's primary market.

KMRC is raising KES 3.0bn — an 8-year amortising bond, min. KES 100,000, closes 21 May 2026

I&M Bank is raising KES 10.0bn — a 5yr 6m bullet bond, min. KES 500,000, closes 15 May 2026

Both offer a coupon of 12.20% p.a.

Which one should you pick?

Breakdown below👇👇

Let's start with the KMRC one.

Kenya Mortgage Refinance Company is a public-private partnership whose shareholders include the Government of Kenya and the World Bank's IDA.

Its entire purpose is to provide long-term funding to mortgage lenders so that more Kenyans can access affordable home loans.

It does not take deposits, it does not run a commercial lending book — it is essentially a development finance vehicle with quasi-sovereign backing.

That ownership structure matters enormously when you are assessing credit risk.

May 2 • 16 tweets • 5 min read

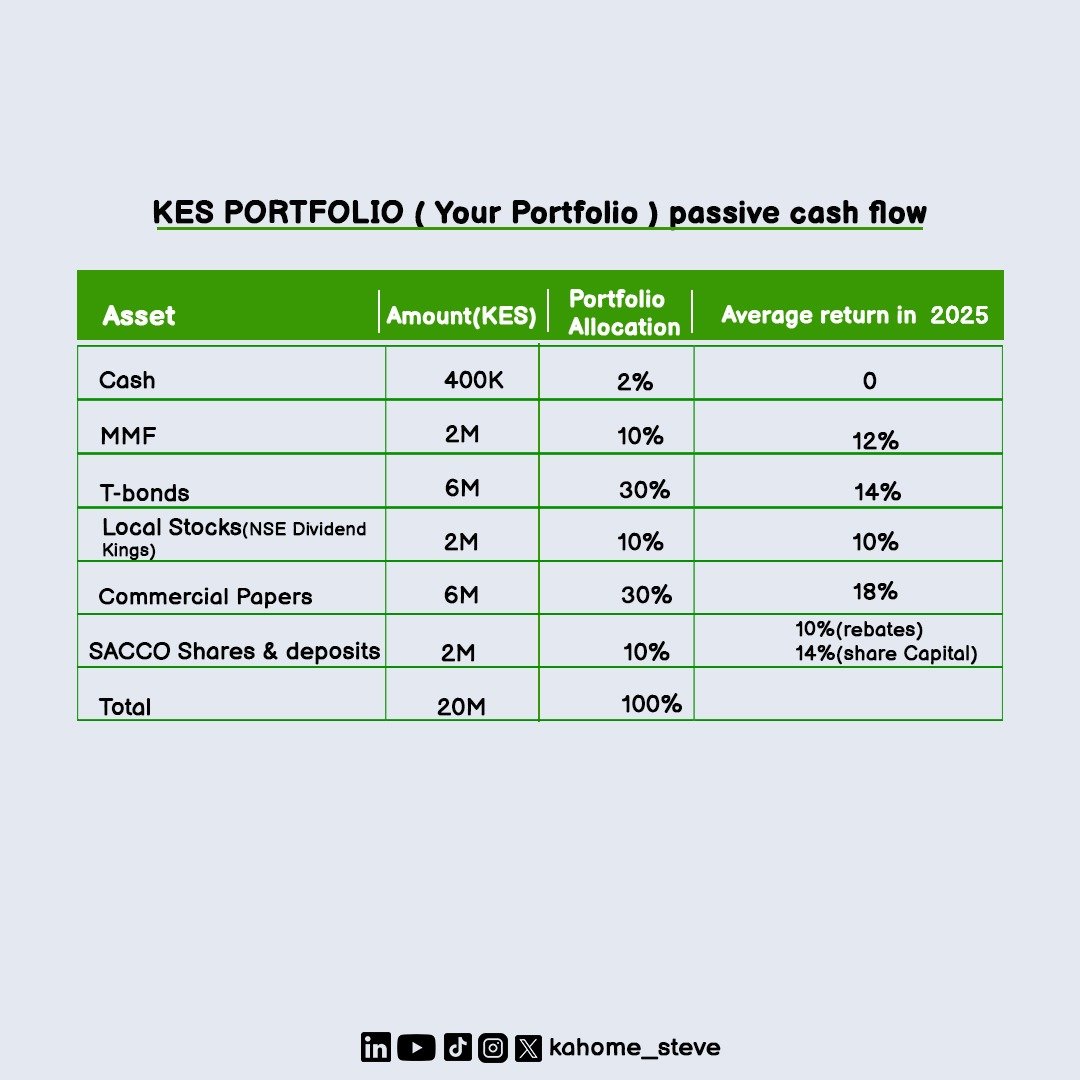

Assuming you can manage to save 20K - 50K a month for the next 5 years,

You can easily create a portfolio that generates a passive income of 10K - 30K per month.

Here's a simple portfolio that you can create👇

A portfolio is a collection of assets owned by one person or an entity.

Simply put, a portfolio represents all the investments that you own.

These assets or investments may include stocks, bonds, real estate, mutual funds, etc.

May 1 • 11 tweets • 5 min read

In Kenya, one of the best personal finance decisions you can make is staying away from any personal debts.

Stay away from mortgages, stay away from car loans, stay away from any type of consumer debt.

Here's why you should stay away from these debts👇

1. In Kenya, the cost of borrowing is way higher than the return of most asset classes.

The average bank loan is at 13-17% while arguably one of the best returning asset class in Kenya, long term Treasury bonds, can only give you 13%

Hence it makes more financial sense to save up for anything rather than financing it with a loan.

This is because you will be making more money for the bank, than you can make in your investments.

Hence you will be losing money in the long run. Working so hard but only rewarding your bank.

Apr 30 • 10 tweets • 3 min read

5 Pieces of Financial advice that work in other developed markets but not in Kenya:

1. Use other peoples' money AKA debt to build wealth (more so in Real Estate)

"Use a mortgage to develop a property, use rental income to repay the mortgage."

This doesn't work in Kenya

Loans in Kenya are super expensive thanks to our Central bank rate and high returns from GoK bonds

Banks would rather lend money to the government than to individuals & businesses.

The average benchmark asset in Kenya returns lower than the average cost of lending.

This is not the case in developed markets.

For example, the S&P 500 has averaged higher returns that the average mortgage rate in the U.S. since 1957

Apr 28 • 5 tweets • 3 min read

90% of Kenyans save their money in the wrong saving avenues.

These include:

1. Banks' saving accounts

2. Banks fixed deposit accounts with low returns

3. Chamas that do merry go rounds

4. Mshwari Lock savings account

5. Under the mattress

Instead of these, there is a better alternative 👇

Where should you ideally save your money and what should you consider when choosing a saving avenue?

✅Security of your funds.

You don't want to save your money in a place where there's a high likely hood of you losing your money.

✅Greater returns than inflation rate.

The CBK has the normal inflation rate in Kenya at around 5%(plus or minus 2.5%)

Hence you want to save your money in an avenue where you can easily beat the inflation rate while exposing your money to very little risk.

✅ Ease of access. For most people, they want to save their money in an avenue where they can easily access their money in case of an emergency or any financial need.

Apr 28 • 13 tweets • 4 min read

🧵 THREAD:

How to use a Whole Life Insurance policy to replace your income & protect your family's cash flow

Read this especially if you have children or dependents.

1/ Let me start with an uncomfortable truth that most people avoid thinking about.

If you died tomorrow, what happens to your family financially? Not emotionally — we know that's devastating.

I mean practically. Who pays rent? Who pays school fees? Who puts food on the table?

Most families in Kenya are one funeral away from financial collapse. That's not dramatic. That's reality.

Apr 27 • 10 tweets • 3 min read

Components of a complete Financial plan?

1. An Emergency fund

2. A sinking fund

3. A KES portfolio

4. A USD portfolio

5. A Wealth Protection portfolio

Breakdown below 👇👇

Here's the breakdown:

1/ An Emergency fund.

What is it?

This is a set amount of money that covers your daily expenses for a certain period of time.

It should cover your daily *normal* expenses for a period of 3-6 months.

Apr 25 • 13 tweets • 5 min read

Should you invest in the local stock market (Nairobi securities Exchange) or in offshore/global markets?

What are the differences, pros and cons of each?

What does it take to invest in each and what strategies should you employ?

Breakdown below👇👇

1/ How much do you need to get started investing?

For NSE, it depends with the stock you want to buy.

With the recent introduction of single shares trading, you can buy as low as one share of the company you want to invest in.

Hence you can start invest with as low as KES 10

For global markets, it depends with the broker you choose.

Most brokers now allow trading of fractional shares. Hence you can start with as low as 1$

Apr 21 • 13 tweets • 4 min read

🧵 THREAD:

How to use a Whole Life Insurance policy to replace your income & protect your family's cash flow

Read this especially if you have children or dependents. 👇

1/ Let me start with an uncomfortable truth that most people avoid thinking about.

If you died tomorrow, what happens to your family financially?

Not emotionally — we know that's devastating. I mean practically. Who pays rent? Who pays school fees? Who puts food on the table?

Most families in Kenya are one funeral away from financial collapse. That's not dramatic. That's reality.