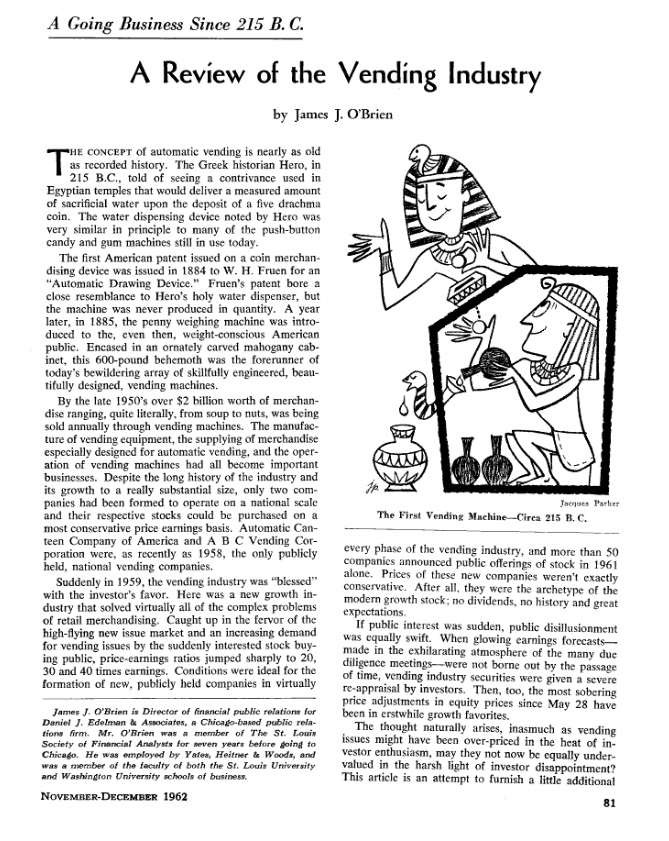

Business collector🚬🏋️♂️🛩️. Tweets are not financial advice & should not be construed as solicitations. They are for informational purposes only.

Historically, air travel has grown at about 2x GDP, with some variation across cycles, but generally speaking, as incomes rise, air traffic rises

Historically, air travel has grown at about 2x GDP, with some variation across cycles, but generally speaking, as incomes rise, air traffic rises

Equity valuations didn't really peak until read GDP growth accelerated at the end pre-COVID, obviously turbocharged by the corporate tax cut. Valuations were higher in the 90s despite high rates b/c real GDP growth was huge & inflation was super low

Equity valuations didn't really peak until read GDP growth accelerated at the end pre-COVID, obviously turbocharged by the corporate tax cut. Valuations were higher in the 90s despite high rates b/c real GDP growth was huge & inflation was super low

that affords you the ability to raise prices incrementally over time, which is reflected in sales growth in all but the energy-related segment

that affords you the ability to raise prices incrementally over time, which is reflected in sales growth in all but the energy-related segment

"Tobacco is the only Staples industry in which prices can consistently rise higher than inflation, and excise structures create a further advantage for manufacturers in disguising the level of price increase they themselves take."

"Tobacco is the only Staples industry in which prices can consistently rise higher than inflation, and excise structures create a further advantage for manufacturers in disguising the level of price increase they themselves take."

"When we tracked the economic profit of the world’s 2,393 largest companies over 10 years, we found [~]50% of a firm’s performance compared to the broader corporate universe is driven by what’s happening in its industry[.]"

"When we tracked the economic profit of the world’s 2,393 largest companies over 10 years, we found [~]50% of a firm’s performance compared to the broader corporate universe is driven by what’s happening in its industry[.]"

Positions have changed only via merger or spin-off. For example:

Positions have changed only via merger or spin-off. For example:

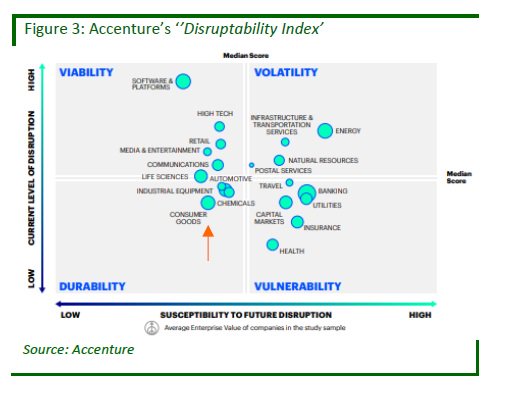

Jon's firm cites interesting data from Accenture, which shows that consumer goods score very highly in terms of 'durability'

Jon's firm cites interesting data from Accenture, which shows that consumer goods score very highly in terms of 'durability'

On a cumulative basis, the industry more or less kept up with the market until about 1970, then crushed. The first regulations due to safety concerns took place in the mid 1960s, which is about the time that the # of firms started to decline, I'm assuming due to consolidation

On a cumulative basis, the industry more or less kept up with the market until about 1970, then crushed. The first regulations due to safety concerns took place in the mid 1960s, which is about the time that the # of firms started to decline, I'm assuming due to consolidation

A good example of this is a company like Church & Dwight $CHD. Over the last ~40 years, it has rarely traded at a discount to the market. Conversely, Altria $MO has rarely traded at a premium to the market.

A good example of this is a company like Church & Dwight $CHD. Over the last ~40 years, it has rarely traded at a discount to the market. Conversely, Altria $MO has rarely traded at a premium to the market.

2. 2. JPM - The Agony & The Ecstasy (of concentrated stock positions)

2. 2. JPM - The Agony & The Ecstasy (of concentrated stock positions)

An excerpt from Howard Marks's 2001 memo that got me thinking about this:

An excerpt from Howard Marks's 2001 memo that got me thinking about this:

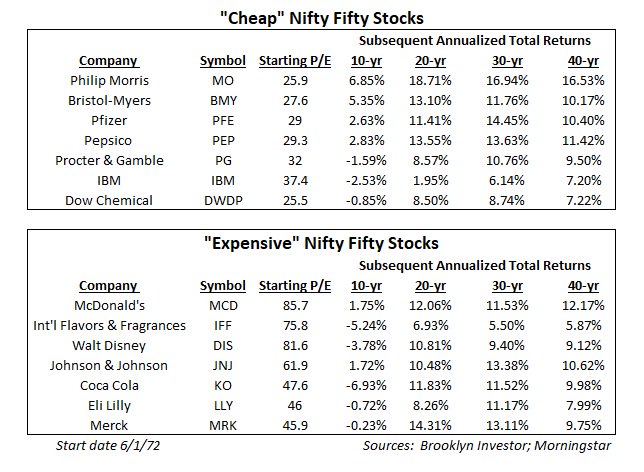

Related, here's a great article from the archives of @jasonzweigwsj on the 1973-1974 market crash that crushed the Nifty Fifty.

Related, here's a great article from the archives of @jasonzweigwsj on the 1973-1974 market crash that crushed the Nifty Fifty.