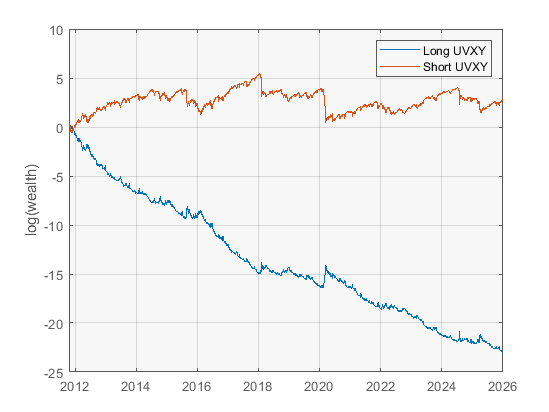

You can make the trade look much better than it is by plotting the collapse in your log(wealth) from being long, but that doesn't mean shorting it is a good idea, as you can see from the red line in my chart. That's volatility drag baby!

You can make the trade look much better than it is by plotting the collapse in your log(wealth) from being long, but that doesn't mean shorting it is a good idea, as you can see from the red line in my chart. That's volatility drag baby!

I think 4-5 people got this exactly right, and a few more had answers along the right lines but didn't mention some key detail. This is the first definitely correct answer that I saw -

I think 4-5 people got this exactly right, and a few more had answers along the right lines but didn't mention some key detail. This is the first definitely correct answer that I saw -

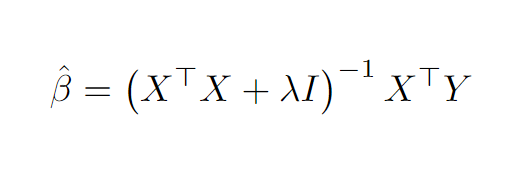

If you've normalized the columns of X so that the diagonal of X'*X are all 1s, then there's a nice interpretation of this - ridge regression both shrinks X'*X toward the identity matrix (ignoring correlations between features) and shrinks coefficients by a factor of 1+lambda

If you've normalized the columns of X so that the diagonal of X'*X are all 1s, then there's a nice interpretation of this - ridge regression both shrinks X'*X toward the identity matrix (ignoring correlations between features) and shrinks coefficients by a factor of 1+lambda

We were long this name for a while (a little unusual - the holding period for this strategy is around a day) and here I've normalized our dollar position by dividing by our max pos. We won't buy any more when this ratio is above 1, and we start selling when it's above 1.15ish

We were long this name for a while (a little unusual - the holding period for this strategy is around a day) and here I've normalized our dollar position by dividing by our max pos. We won't buy any more when this ratio is above 1, and we start selling when it's above 1.15ish

The quantities are all rescaled/renormalized btw, they don't tell you anything about the answer.

The quantities are all rescaled/renormalized btw, they don't tell you anything about the answer.