Economist, forecaster, associate professor, CEO, PhD. Expert of financial crises and geopolitics. MACA. Newsletter: https://t.co/brrLzzBJqM

This is due to the fact that if NATO were to retaliate for the leveling of Ukraine with a nuclear strike, Moscow would launch retaliation, destroying London, Berlin, Paris, Stockholm, and Washington DC (and possibly drowning the U.K.) before the first nuclear bombs would have hit Russian soil.

This is due to the fact that if NATO were to retaliate for the leveling of Ukraine with a nuclear strike, Moscow would launch retaliation, destroying London, Berlin, Paris, Stockholm, and Washington DC (and possibly drowning the U.K.) before the first nuclear bombs would have hit Russian soil.  President Trump started with a correct note by re-establishing connections with Moscow. He also put President Zelensky in the "presser" with @VP .

President Trump started with a correct note by re-establishing connections with Moscow. He also put President Zelensky in the "presser" with @VP .

Just six months ago, our government-funded (propaganda) channel @yleuutiset notified that Russian military bases near Finland are nearly empty.

Just six months ago, our government-funded (propaganda) channel @yleuutiset notified that Russian military bases near Finland are nearly empty.

For an untrained eye, it may appear that the motivation behind both wars, in Ukraine and the Middle East (Gaza/Lebanon/Syria), would be the same: threat.

For an untrained eye, it may appear that the motivation behind both wars, in Ukraine and the Middle East (Gaza/Lebanon/Syria), would be the same: threat.  Even in the deepest depths of my depression in my teenage years, I did not settle. I knew what I wanted. Never settle. ☝️

Even in the deepest depths of my depression in my teenage years, I did not settle. I knew what I wanted. Never settle. ☝️

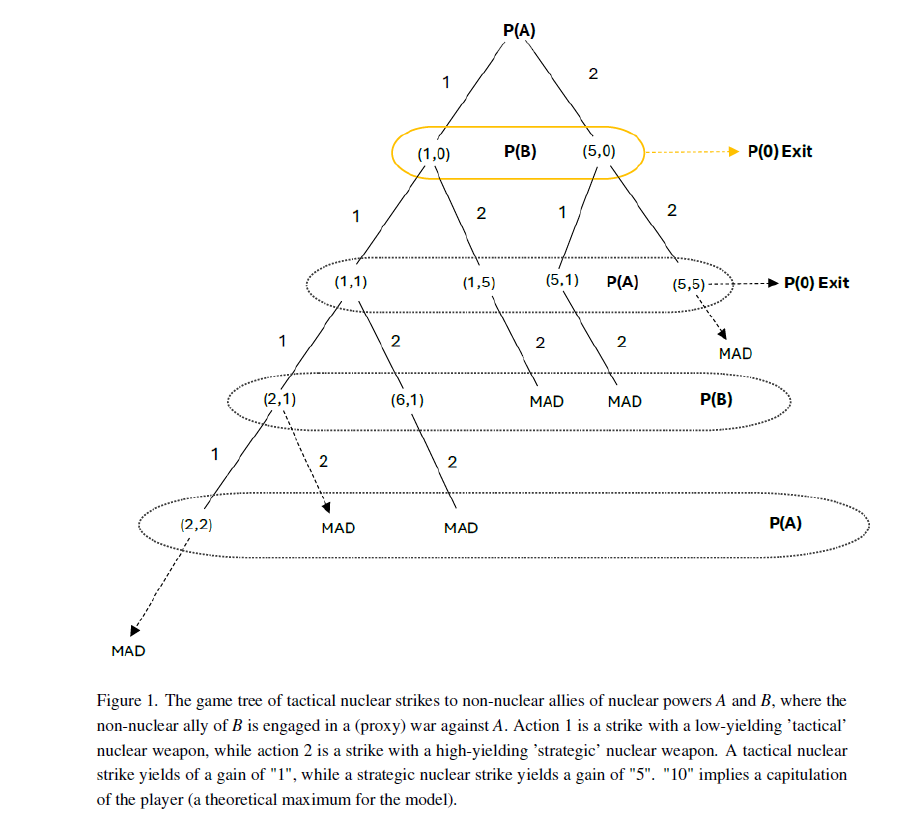

Most importantly, if the analysis of @cirnosad is correct, as I start to believe it is (no personal expertise, though), we would have entered an era of nuclear warfare, with horrendous implications. Another excerpt from my article.

Most importantly, if the analysis of @cirnosad is correct, as I start to believe it is (no personal expertise, though), we would have entered an era of nuclear warfare, with horrendous implications. Another excerpt from my article.

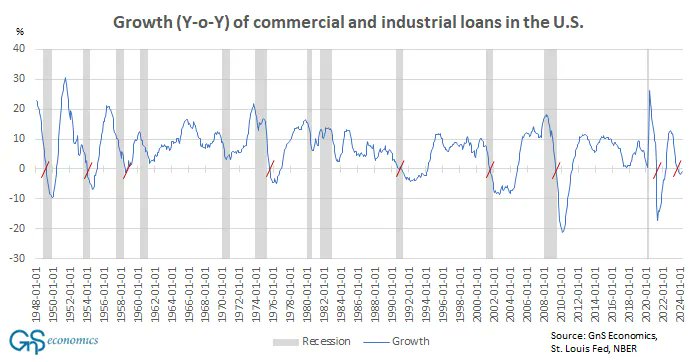

The Fed is currently arguing that these gargantuan deficits (losses) do not to matter, because it can accrue seigniorage revenue (from its money 'printing'; see my post to subscribers here) ad infinitum. So, it claims to be solvent despite of these losses.

The Fed is currently arguing that these gargantuan deficits (losses) do not to matter, because it can accrue seigniorage revenue (from its money 'printing'; see my post to subscribers here) ad infinitum. So, it claims to be solvent despite of these losses.