Deputy Director @DelorsBerlin | Think-tanking on European fiscal, industrial and economic policy | PhD alumnus @IPZuser

Oct 7, 2024 • 12 tweets • 3 min read

We’ve got some early leaks on the European Commission’s thinking for the new "Competitiveness Fund" in the next EU budget. This fund is set to play a big role in shaping the EU’s long-term industrial policy ambitions, and so far, I’ve got mixed feelings. Two quick thoughts:

For context, crafting a proposal for this fund will be a major task for the next COM. In practice, it will only become relevant for the next MFF (from 2028 onward). However, von der Leyen has flagged it as one of the deliverables for the first 100 days of the working program.

Sep 9, 2024 • 19 tweets • 3 min read

The Draghi report contains one of the most spot-on critiques for the current state of EU industrial policy I have read so far.

And it comes with some solid ideas on how to move forward. Here are the three main takeaways.

First, the report offers a clear-eyed assessment of what’s currently going wrong. European efforts to craft a unified industrial strategy have been hampered by two major issues. On the one hand, industrial policies remain fragmented along national lines.

Jul 17, 2024 • 17 tweets • 4 min read

There's a lot of buzz about an impending clash between France and Brussels over fiscal policy. Indeed, complying with the new EU fiscal rules will be a tough nut to crack, no matter who forms the next French government. Here's a quick rundown of the procedure ahead:

To start, the Commission has placed France in an "excessive deficit procedure" (EDP) for breaching the 3% deficit limit. The new rules require deficits to be below this benchmark within 4 years. With commitments to investments and reforms, member states can get another 3 years.

Jun 26, 2024 • 19 tweets • 5 min read

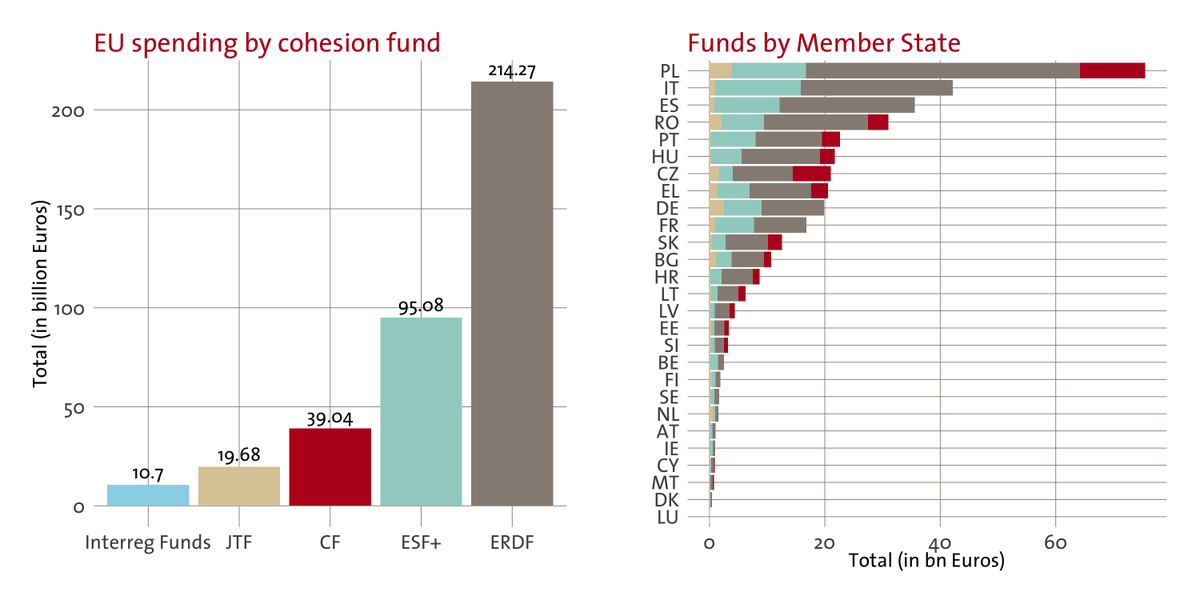

The EU's regional funds are one of the biggest spending items of the EU and a key sticking point in the next budget negotiations.

In a new paper, @valentin_lang, @DanBischof and I use new data to see who benefits from them. And we show they need fundamental reforms. Here's why:

First things first, getting EU cohesion policy right is important. For one, the EU spends a lot of money on its regional policy. Currently, it amounts to €392 billion over seven years - this is almost a third of its entire European budget.

Feb 7, 2024 • 12 tweets • 2 min read

The Net Zero Industry Act was touted as the EU's big response to the US Inflation Reduction Act. It has been in the making for a year. Now it will finally hit the books. Here is the lowdown on what you need to know about it.

First, binding production targets are gone. To signal its ambition in the green tech race, the COM initially laid out precise EU production goals for a list of net-zero sectors. In the legislative process, that list got longer, but the binding production targets were taken out.

Oct 24, 2023 • 15 tweets • 3 min read

The DE Ministry of the Economy just published its long-awaited industrial strategy. It does not add many new measures but provides a pretty honest description of what DE is doing and why it is doing it. And for the EU it has some actual news. Here are the 3 most important points

For context, this is the first official industrial strategy since 2019. The last one was a bit of a disaster. From spelling out industry target shares to implicitly giving state guarantees to a list of major companies, it largely showcased how not to do industrial policy.

Feb 1, 2023 • 15 tweets • 3 min read

The Commission just published its proposal for an EU response to the IRA.

Here is what you need to know about it, why it is still quite vague, and why that might not be such a bad thing.

ec.europa.eu/commission/pre…

Two things are essential in the debate on the COM's new "Green Deal Industry Plan". First, how much additional legroom will the EU provide MS to respond to the US' green subsidy push with national measures?

Dec 20, 2022 • 14 tweets • 3 min read

FR and DE push ahead on EU industrial policy. They just published a paper on what they think the EU response to the US Inflation Reduction Act should look like.

What they call for could amount to big reforms. So, here are the 3 most interesting points.

First, both countries want laxer EU state aid rules. So far, so obvious. FR and DE have asked for more legroom for national industrial policies for a long time. So this alone is no big surprise. However, the scope of what the paper calls for is quite substantial.

Dec 14, 2022 • 19 tweets • 6 min read

.@vonderleyen just outlined here ideas for an EU response for the US Inflation Reducation Act (IRA).

Quick thread on the three main points and what they mean:

First, some context: the IRA has rekindled EU industrial policy FOMO. The combination of immense fiscal firepower (USD 370bn including technically limitless tax breaks) and clear protectionist elements (buy American) sparked real concerns about 🇪🇺 competitiveness.

Nov 9, 2022 • 16 tweets • 5 min read

The @EU_Commission just published its proposal for the reform of EU fiscal rules. @LindnerJS and my first thoughts: Some parts are good, some parts are vague and some parts are going to be rightly challenged. Here's the gist of it and 4 crucial things for the coming negotiations.

The central idea of the Communication is to allow MS to negotiate more country-specific and thus realistic debt-reduction paths, while also allowing for extra space for public investment and creating new reform incentives for national governments.

Aug 29, 2022 • 8 tweets • 2 min read

Olaf Scholz just gave his first big keynote address on the Future of the EU at the Charles University in Prague. Three quick points on the economic policy dimensions of the speech that were actually quite interesting.

First, the chancellor seems serious about the reforms of EU fiscal rules. On substance, the speech did not add much to the principles of the German position published in mid-August bmwk.de/Redaktion/EN/D…

Mar 19, 2022 • 12 tweets • 4 min read

Great thread! But not convinced that it's only frugal resistance that keeps the debate on new EU borrowing from moving forward. There are also some real questions on goals, price tags and funding needs that need to be addressed to get into a more constructive mode. Quick thread/

First, what are the goals of more EU spending? So far, there are two. In the short-term, the EU needs to safeguard a joint position toward Putin. Since the costs of sanctions etc. are going to be split unevenly, pandemic-like burden-sharing may be needed. shorturl.at/mMVX7

Mar 7, 2022 • 21 tweets • 6 min read

On Thursday, EU leaders meet to discuss next steps regarding Putin's invasion of UA.

One point of discussion: the economic consequences for🇪🇺. In a new brief, I work through some data on differences across MS.

Tl;dr: they are big! A thread in 10 charts/ shorturl.at/hkqwV

First things first: The economic knock-on effects of the Ukraine war are going to be felt throughout Europe. Costs from sanctions and trade disruptions, rising inflation due to higher energy prices and mounting uncertainty all will become a drag on Europe’s economy.

May 25, 2021 • 16 tweets • 4 min read

Combat climate change, spur the recovery, strengthen autonomy - like many others, the EU has developed big industrial policy ambitions. I wrote a paper on whether its new strategy will work.

Spoiler: It won't.

But it could - with some real 🇪🇺changes. 1/ bit.ly/3yBVdu0

Starting with context: on May 5 the @EU_Commission published an update to its new industrial strategy. It was long-awaited. The Commission had declared industrial policy as a core initiative of its tenure and many expected a big post-Covid push. This did not happen.

Nov 1, 2019 • 12 tweets • 5 min read

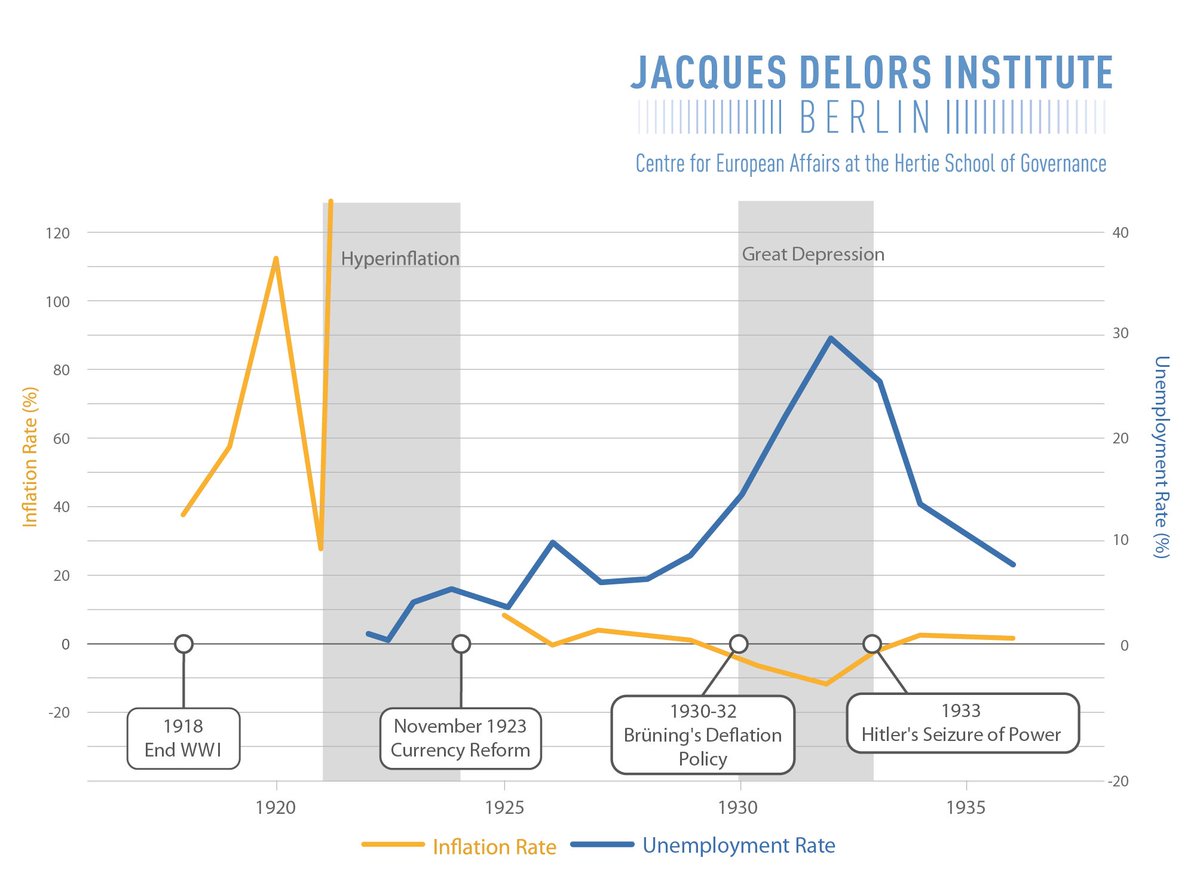

Today @Lagarde takes over at the ECB. Amongst her challenges: dealing with a German public deeply sceptical of ECB policies. In a new paper @LHaffert, @tobirommel and I study the historic roots of this scepticism. Spoiler: it's a misunderstanding. tinyurl.com/y5zex367 (1/n)

To explain German skepticism, commentators often point to the collective memory of the #Hyperinflation in the early 1920s. But why is this still such a strong reference point? We find that many Germans merge it with the Great Depression – a totally different crisis (2/n)