“The world is a hellish place and bad writing is destroying the quality of our suffering.”

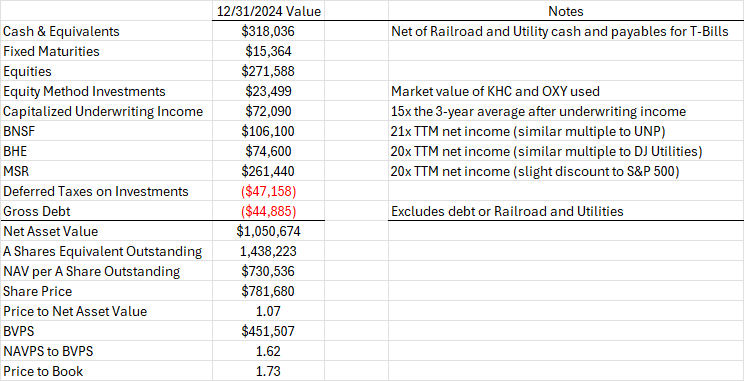

That's a little rich, though not crazy expensive, of a valuation. But, by my estimates it's the first time since 2001 that $BRK has traded at a premium to its NAV. In 2011 and again in the aftermath of the pandemic discounts got as high as more than 30%.

That's a little rich, though not crazy expensive, of a valuation. But, by my estimates it's the first time since 2001 that $BRK has traded at a premium to its NAV. In 2011 and again in the aftermath of the pandemic discounts got as high as more than 30%.

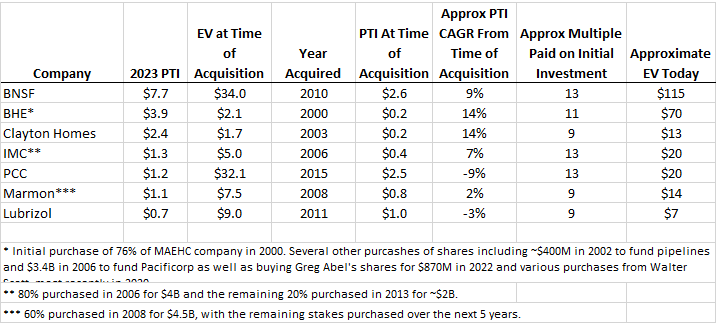

Knowing s/h equity would fill in gap on how much incremental cap was invested to achieve results over time. In case of BNSF (which reports separately), s/h equity was $46.4B at the end of last year. Pretty impressive - $5B PT incremental profit vs. $12B incremental investment.

Knowing s/h equity would fill in gap on how much incremental cap was invested to achieve results over time. In case of BNSF (which reports separately), s/h equity was $46.4B at the end of last year. Pretty impressive - $5B PT incremental profit vs. $12B incremental investment.