Physicist, Ergodicity Economics @LdnMathLab, @sfiscience.

Book: https://t.co/Ud4s4YSGD0

2/

2/ 2/

2/ This work soon attracted the attention of some extraordinary thinkers. I had met them because we were all members of the community around the Santa Fe Institute @sfiscience. Among them were Murray Gell-Mann, Ken Arrow, Reuben Hersh, and Cormac McCarthy.

This work soon attracted the attention of some extraordinary thinkers. I had met them because we were all members of the community around the Santa Fe Institute @sfiscience. Among them were Murray Gell-Mann, Ken Arrow, Reuben Hersh, and Cormac McCarthy.

2/

2/

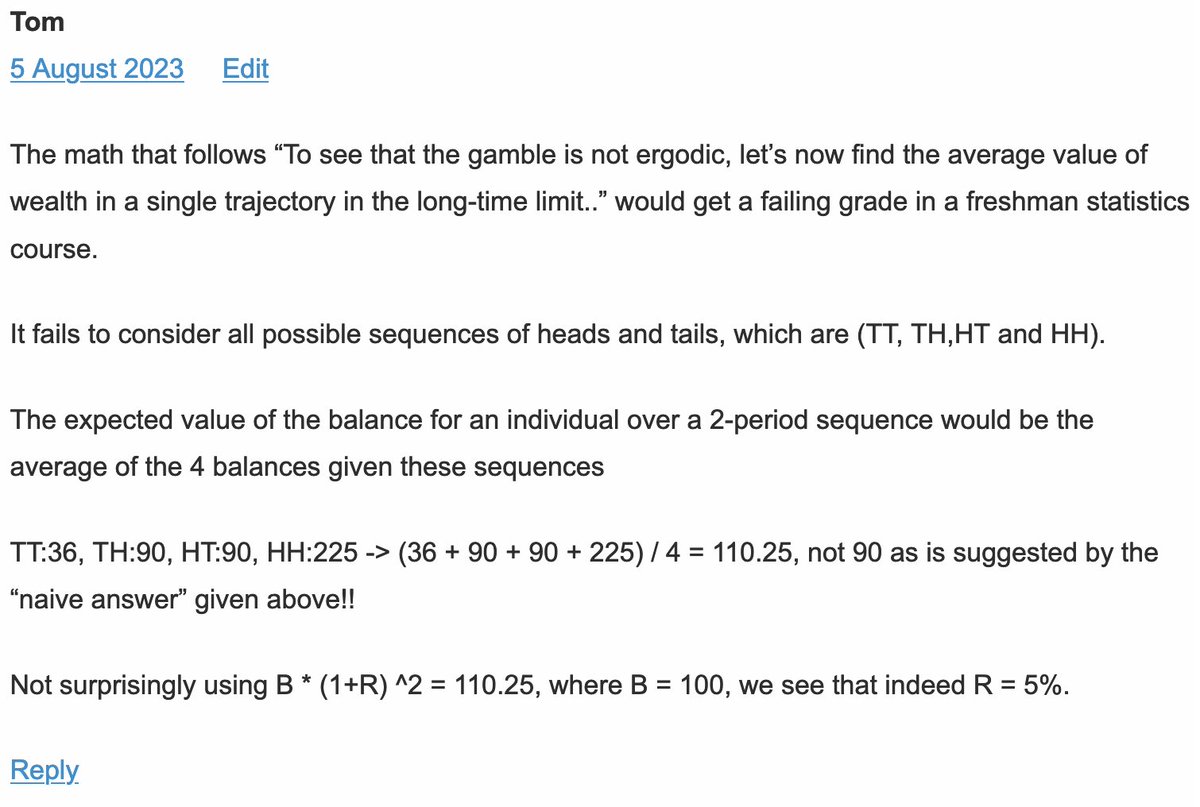

Update: Tom is still rather angry. He has now worked out how to compute expected value.

Update: Tom is still rather angry. He has now worked out how to compute expected value.

2

2 ...by Annalen der Physik - yes, the journal which publishes the Physics Nobel Lectures - to write a review article on Ergodicity Economics. So I'm using all my channels to find out what people have done.

...by Annalen der Physik - yes, the journal which publishes the Physics Nobel Lectures - to write a review article on Ergodicity Economics. So I'm using all my channels to find out what people have done.

2/5

2/5

2/

2/ 2/9

2/9