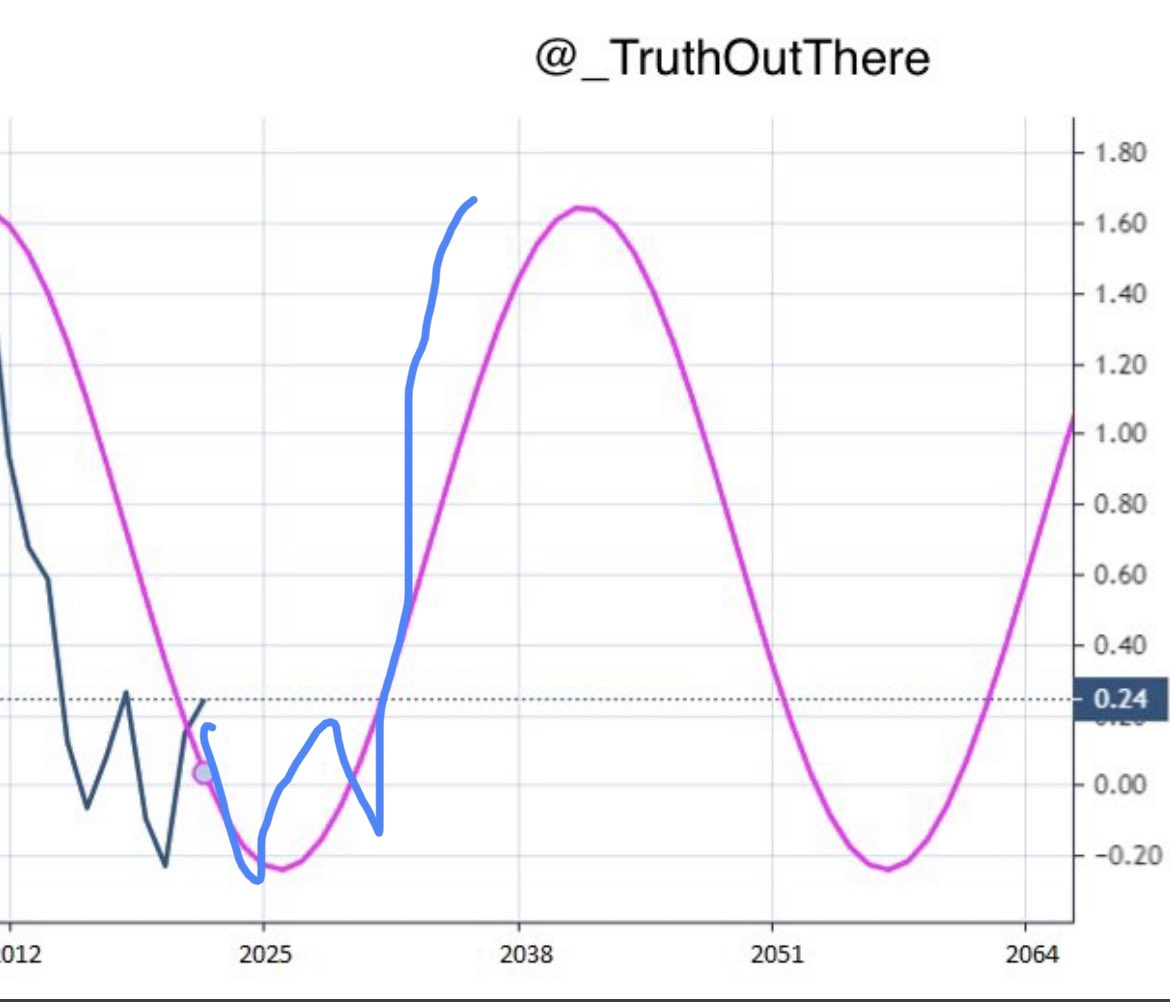

Chief Strategist Simplify Asset Management | PM of top ranked high yield ETF, $CDX. Not investment advice

2/n What the chart is highlighting is that credit and equity are both parts of the capital structure with unique behavior that is contingent on the value of the assets. Credit is a "short put" asset claim. If assets rise to absurd heights, credit "benefits" because risk of default declines. But it doesn't benefit "much"

2/n What the chart is highlighting is that credit and equity are both parts of the capital structure with unique behavior that is contingent on the value of the assets. Credit is a "short put" asset claim. If assets rise to absurd heights, credit "benefits" because risk of default declines. But it doesn't benefit "much"

2/n It's one thing to have your fundamental errors pointed out (repeatedly) and adjust. It's another to double down. You have to ask, "What's the agenda?" at some point

2/n It's one thing to have your fundamental errors pointed out (repeatedly) and adjust. It's another to double down. You have to ask, "What's the agenda?" at some point

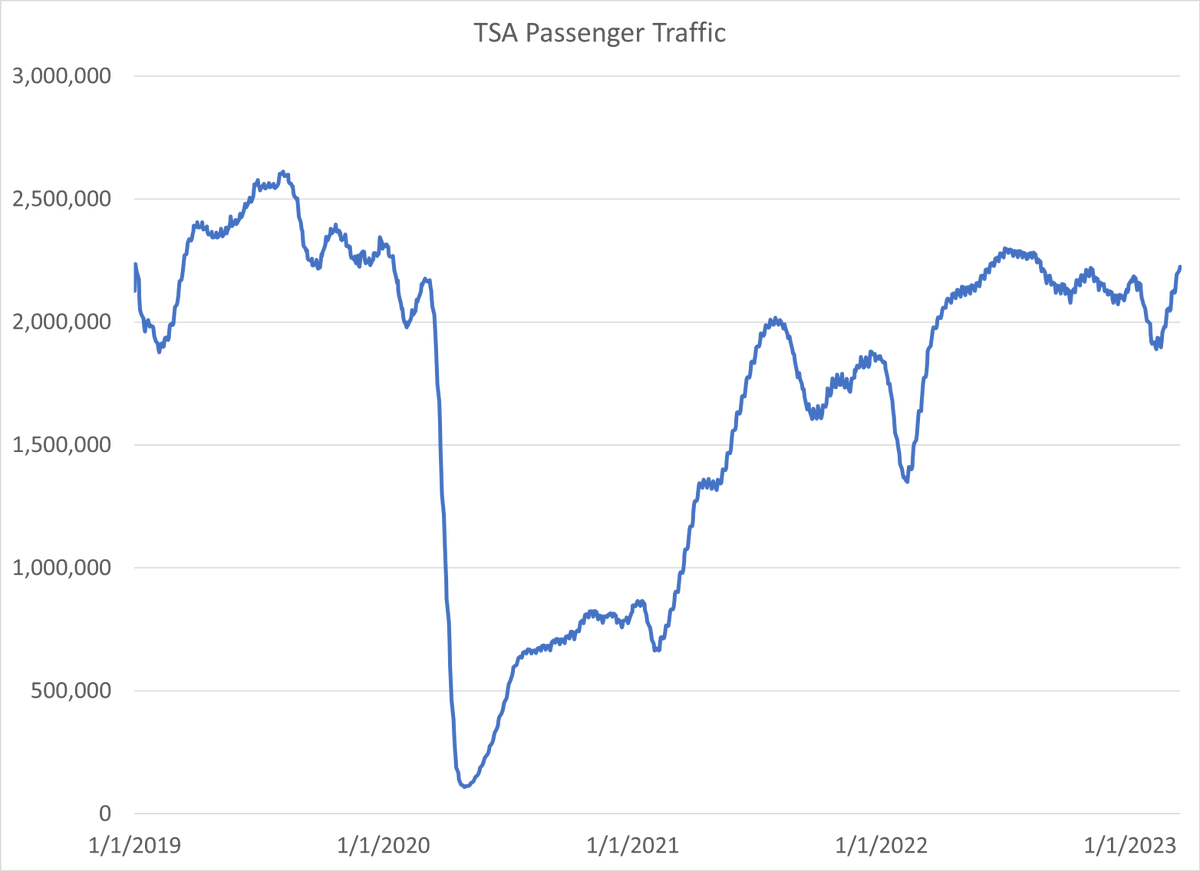

2/n even as they rise (and will continue to rise on a seasonal basis as Q1 tends to see bonus checks/tax refunds used to catch up). I would highlight that the low levels of delinquency are a function of unique factors that are now REVERSING rather than normalizing

2/n even as they rise (and will continue to rise on a seasonal basis as Q1 tends to see bonus checks/tax refunds used to catch up). I would highlight that the low levels of delinquency are a function of unique factors that are now REVERSING rather than normalizing

"The national surge in business formation since 2020 has been led by a handful of industries, including transport and warehousing; accommodation and food services; health care and social assistance; and retail trade."

"The national surge in business formation since 2020 has been led by a handful of industries, including transport and warehousing; accommodation and food services; health care and social assistance; and retail trade."