Suppose decline in interest rates is due to demand-side factors (population aging, rising inequality, global saving glut). How will firms respond to lower interest rates when deciding how much to invest in productivity enhancement? (2/N)

Suppose decline in interest rates is due to demand-side factors (population aging, rising inequality, global saving glut). How will firms respond to lower interest rates when deciding how much to invest in productivity enhancement? (2/N)

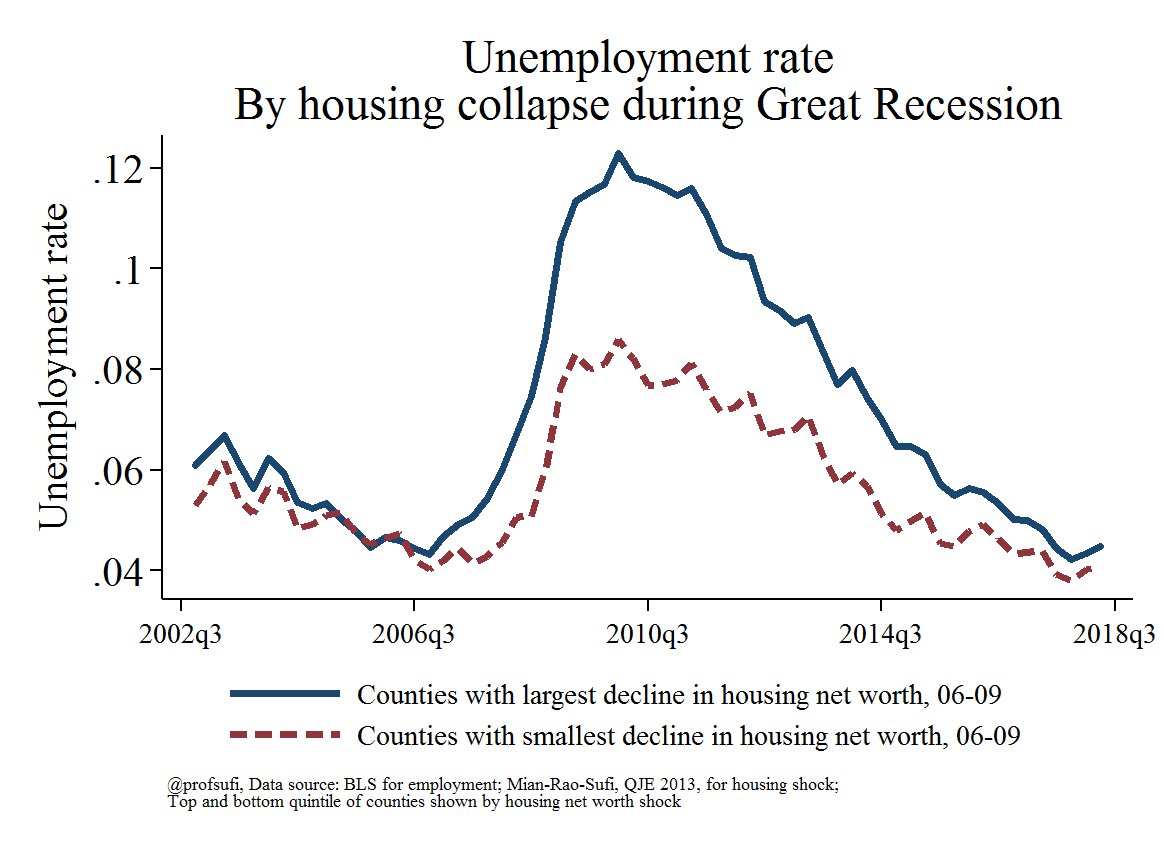

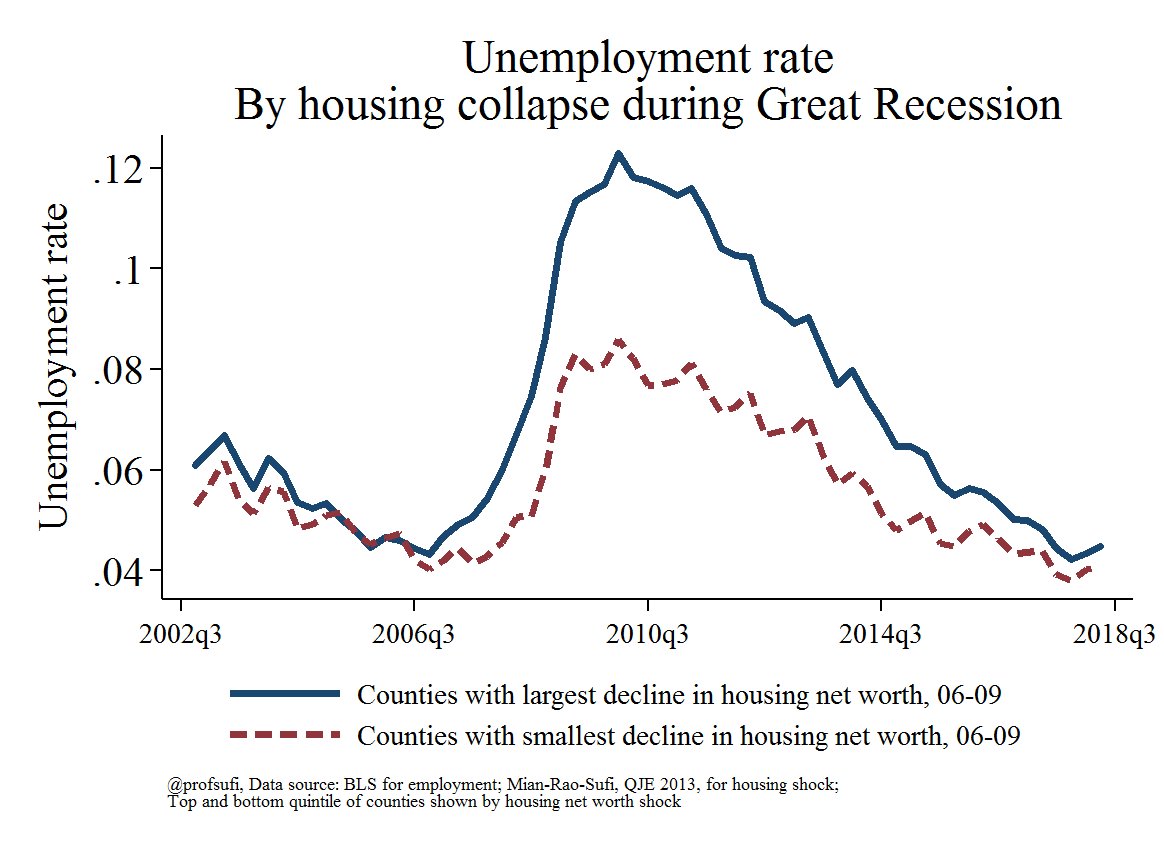

2/ Notice that pre 2006, counties with largest subsequent housing collapse saw similar unemployment rates, and even weak evidence of a larger decline in unemployment rate.

2/ Notice that pre 2006, counties with largest subsequent housing collapse saw similar unemployment rates, and even weak evidence of a larger decline in unemployment rate.